TDI Fibonacci Volatility Bands Candle Coloring [cryptalent]"This is an advanced Traders Dynamic Index (TDI) candle coloring system, designed for traders seeking precise dynamic analysis. Unlike traditional TDI, which typically relies on a 50 midline with a single standard deviation band (±1 SD), this indicator innovatively incorporates Fibonacci golden ratio multiples (1.618, 2.618, 3.618 times standard deviation) to create multi-layered dynamic bands. It precisely divides the RSI fast line (green line) position into five distinct strength zones, instantly reflecting them on the candle colors, allowing you to grasp market sentiment in real-time without switching to a sub-chart.

Core Calculation Logic:

RSI Period (default 20), Band Length (default 50), and Fast MA Smoothing Period (default 1) are all adjustable.

The midline is the Simple Moving Average (SMA) of RSI, with upper and lower bands calculated by multiplying Fibonacci multiples with Standard Deviation (STDEV), generating three dynamic band sets: 1.618, 2.618, and 3.618.

Traders can quickly identify the following scenarios:

Extreme Overbought Zone (Strong Bullish, Red): Fast line exceeds custom threshold (default 82) and breaks above the specified band (default 2.618). This often signals overheating, potentially a profit-taking point or reversal short entry, especially at trend tops.

Extreme Oversold Zone (Strong Bearish, Green): Fast line drops below custom threshold (default 28) and breaks below the specified band (default 2.618). This is a potential strong rebound starting point, ideal for bottom-fishing or long entries.

Medium Bullish Zone (Yellow): Fast line surpasses medium threshold (default 66) and stands above the specified band (default 1.618), indicating bullish dominance in trend continuation.

Medium Bearish Zone (Orange): Fast line falls below medium threshold (default 33) and breaks below the specified band (default 1.618), signaling bearish control in segment transitions.

Neutral Zone (No Color Change): Fast line within custom upper and lower limits (default 34~65), retaining original candle colors to avoid noise interference during consolidation.

Color priority logic flows from strong to weak (Extreme > Medium > Neutral), ensuring no conflicts. All parameters are highly customizable, including thresholds, band selections (1.618/2.618/3.618/Midline/None), color schemes, and even optional semi-transparent background coloring (default off, transparency 90%) for enhanced visual layering.

Applicable Scenarios:

Intraday Trading: Capture extreme color shifts as entry/exit signals.

Swing Trading: Use medium colors to confirm trend extensions.

Long-Term Trend Following: Filter noise in neutral zones to focus on major trends.

Supports various markets like forex, stocks, and cryptocurrencies. After installation, adjust parameters in settings to match your strategy, and combine with other indicators like moving averages or support/resistance for improved accuracy.

If you're a TDI enthusiast, this will make your trading more intuitive and efficient!

Sisihan Piawai

Cat Cushion Position SizingThis strategy is for people who don’t want to guess position size every time.

It looks at how volatile the market is and then tells you how many units to hold so your risk per trade stays roughly the same – whether the chart is calm or crazy.

What it does

Measures how “shaky” the price is day by day (volatility)

Blends recent volatility with a long-term average so it doesn’t overreact to one weird day

Uses your Risk per Trade (%) setting to calculate how big your position should be

Adds a buffer zone so it doesn’t trade every tiny wiggle and burn commissions

Shows a small performance table on the chart:

• Average annual return (from backtest)

• Sharpe ratio

• Average drawdown per trade

• Current position size as % of equity

How it thinks about risk

When the market is calmer → volatility is lower → position size can be bigger

When the market is wild → volatility is higher → position size becomes smaller

You control the “spiciness” with:

• Risk per Trade (%) – how much of your equity you’re willing to risk on each position

• Change Sensitivity (%) – wider buffer = fewer trades, lower costs; tighter buffer = more frequent rebalancing

Good use cases

Index ETFs (e.g. AMEX:SPY , NASDAQ:ACWI ) or other liquid instruments

People who:

• Already have a direction/idea (bullish on the index long term)

• Want the position sizing to adapt automatically with volatility

• Prefer “set the rules, let it run” rather than staring at the screen

Inputs to pay attention to

Risk per Trade (%)

• Conservative: ~1–2%

• Balanced: ~3–4%

• Aggressive: 5%+ (handle with care)

Important notes

This is a position sizing / risk strategy, not a magical “always win” tool

Works best when combined with:

• A clear idea of what you want to trade (e.g. broad index ETFs)

• A realistic risk profile (don’t just max the risk because the backtest looks better)

Backtest results are not a promise of future returns

Educational use only – this is not financial advice. Please test on your own, tweak to your comfort level, and don’t bet the rent money 😉

If you like systematic, “low-drama” investing (and want to spend more time chilling like a cat 🐱), this script helps the math side stay under control in the background.

SigmaFrame-FESXSigmaFrame is a volatility-weighted standard deviation engine designed to generate dynamic intraday pivot levels which expand during volatility spikes and tighten during compression, giving traders a consistent structural map across trending and rotational environments.

SigmaFrame-NQSigmaFrame is a volatility-weighted standard deviation engine designed to generate dynamic intraday pivot levels which expand during volatility spikes and tighten during compression, giving traders a consistent structural map across trending and rotational environments.

SigmaFrame-ESSigmaFrame is a volatility-weighted standard deviation engine designed to generate dynamic intraday pivot levels which expand during volatility spikes and tighten during compression, giving traders a consistent structural map across trending and rotational environments.

VWAP Bands ProDisclaimer: This script is for educational purposes only and is not financial advice. Trading involves risk, and users are responsible for their own decisions.

VWAP Bands Pro is a professional volatility tool that anchors the Volume Weighted Average Price to a chosen timeframe and projects standard deviation bands to reveal stretched price zones.

Key Features

Anchored Precision : Calculates VWAP from a fixed anchor period (default: Daily) for a clean institutional reference point.

Standard Deviation Bands : Plots 1s, 2s, and 3s bands to show volatility. Moves into the outer bands often point to exhaustion or possible reversal areas.

Glowing Gradient Design : Uses a premium multi step gradient that fades outward, making extreme zones easy to spot.

Clean Visuals : Prioritizes smooth gradient fills instead of crowding the chart with heavy lines.

How to Use

Anchor Period : Select the timeframe you want the tool to follow. Daily works well for intraday setups, while Weekly or Monthly suits swing trades.

Strategy : Watch for mean reversion setups when price moves into the 2s to 3s outer zones and starts to reject, aiming for a return toward the central VWAP.

Today Range Calculator1. Indicator Name

Today (Today’s Volatility)

2. One-line Introduction

Displays real-time 30-day historical volatility (HV30) as a compact table on the chart, helping traders instantly assess market risk levels.

3. General Overview

Today ↑↓ is a lightweight informational widget that calculates and displays the 30-day Historical Volatility (HV30) of the asset in real time.

Using logarithmic returns over the past 30 periods, the script computes variance and then annualizes it to express volatility as a percentage (%) per year.

The result is shown in a clean 1x1 table cell, which can be positioned anywhere on the chart—top/bottom, left/right—depending on your preference.

This makes it easy to quickly evaluate whether the current market is high-risk (volatile) or stable, without cluttering the chart.

It’s especially useful for position sizing, risk management, volatility-based entry/exit decisions, and as a filter for breakout strategies.

Built with performance in mind, the script uses minimal system resources and can be used alongside any indicator or strategy without interference.

4. Key Advantages

📈 Real-time HV30 Display

Calculates and displays 30-day historical volatility using annualized log return variance.

📍 Custom Table Positioning

Place the volatility display in any corner of the chart for optimal visibility.

🧮 Accurate Log Return Calculation

Uses logarithmic returns to ensure precise volatility representation over time.

🎯 Quick Market Sentiment Read

Helps you determine at a glance whether the asset is in a calm or volatile environment.

🧼 Minimalist Design

Clean 1-cell table format keeps your chart readable and organized.

🚀 Ultra-Lightweight Script

Runs efficiently with negligible impact on chart performance.

📘 Indicator User Guide

📌 Basic Concept

Today ↑↓ calculates 30-day Historical Volatility (HV30) by analyzing the asset’s log returns over the past 30 bars.

The result is annualized and shown as a percentage to reflect volatility in standardized terms.

Useful for gauging risk levels and strategy suitability in current market conditions.

⚙️ Settings Explained

Table Position: Choose where the volatility table appears:

Top Left / Top Right / Bottom Left / Bottom Right

📈 High Volatility Example

HV30 > 50% indicates a volatile environment

Suggests wider stop-losses, cautious position sizing, or favoring breakout strategies

📉 Low Volatility Example

HV30 < 15% suggests a calm market or range-bound behavior

Useful as a signal for upcoming volatility expansions or breakout preparations

🧪 Recommended Use Cases

Position Sizing: Scale position size based on HV30 readings

Strategy Filter: Activate certain systems only when volatility meets predefined conditions

Breakout Timing: Identify low-volatility zones as potential breakout opportunities

🔒 Precautions

This indicator does not generate buy/sell signals; it is a volatility reference tool

HV thresholds vary across asset classes—adjust interpretation accordingly

Since HV30 is historical, it may lag during rapid market changes

Z-Score Regime DetectorThe Z-Score Regime Detector is a statistical market regime indicator that helps identify bullish and bearish market conditions based on normalized momentum of three core metrics:

- Price (Close)

- Volume

- Market Capitalization (via CRYPTOCAP:TOTAL)

Each metric is standardized using the Z-score over a user-defined period, allowing comparison of relative extremes across time. This removes raw value biases and reveals underlying momentum structure.

📊 How it Works

- Z-Score: Measures how far a current value deviates from its average in terms of standard deviations.

- A Bullish Regime is identified when both price and market cap Z-scores are above the volume Z-score.

- A Bearish Regime occurs when price and market cap Z-scores fall below volume Z-score.

Bias Signal:

- Bullish Bias = Price Z-score > Market Cap Z-score

- Bearish Bias = Market Cap Z-score > Price Z-score

This provides a statistically consistent framework to assess whether the market is flowing with strength or stress.

✅ Why This Might Be Effective

- Normalizing the data via Z-scores allows comparison of diverse metrics on a common scale.

- Using market cap offers broader insight than price alone, especially for crypto.

- Volume as a reference threshold helps identify accumulation/distribution regimes.

- Simple regime logic makes it suitable for trend confirmation, filtering, or position biasing in systems.

⚠️ Disclaimer

This script is for educational purposes only and should not be considered financial advice. Always perform your own research and risk management. Past performance is not indicative of future results. Use at your own discretion.

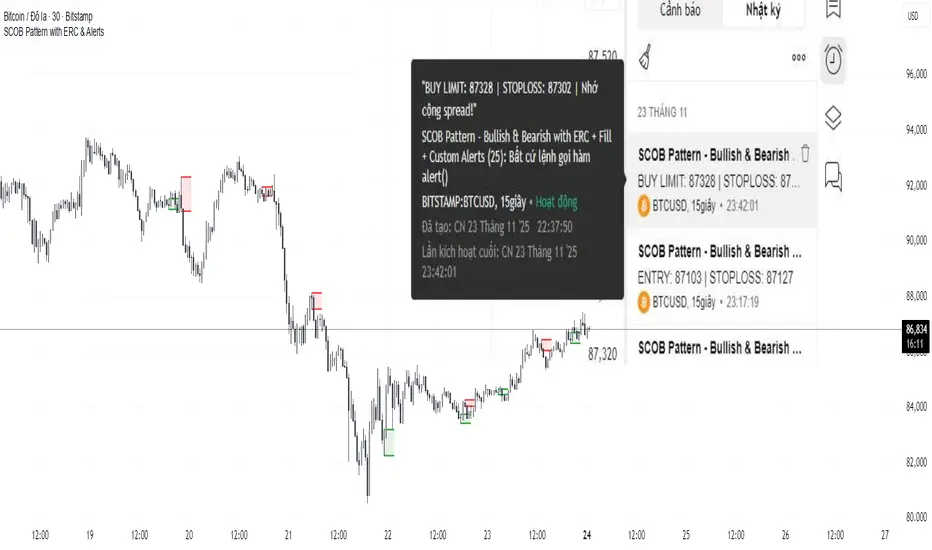

SCOB Pattern with ERC & AlertsSingle Candle Block (SC0B) consists of a single candle appearing at a significant price level, indicating a confirmed reversal in price direction from that particular area of interest.

SCOB is primarily used to confirm and execute trades.

Using a single candle block to enter a trade minimizes risk and maximizes reward.

Single bullish candle block?

1st candle closes at bullish point of interest with a short or long wick.

2nd candle sweeps the low of previous(1st) candle and closes above the low of previous candle.

3rd candle closes above the high of 2nd candle.

How to trade with Scob bullish.

To Trade using Bullish SCOB you have to wait for price to come down and test the single candle order block.

When price tests the SCOB you can directly execute a buy trade or for a precise entry you can wait for a market structure shift in lower time frame.

Scob discount is the opposite of price increase.

This strategy should only be used when price "sweeps through key lever, liquidity, imbalance, poi htf areas.

This indicator will add a filter to help you reduce signal noise.

Use the "Use engulfing candle to test" function to filter the 3rd candle.

Only search for Scob if the 3rd candle is an Engulfing candle.

The logic for finding Engulfing candles can be changed based on the "% maximum wick length" option. The default is that the candle wick is 25% of the total candle wick length.

You can also use the alert function when Scob appears

With Smart money concept, no strategy is perfect in trading, so you should not risk too much of your capital on this strategy.

To be safer, always remember to use stop loss for every trade.

Hourly Volatility Bands (StdDev)real mathematical stdv based on research conducted by me. if you find that anything is wrong feel free to reach out to me and correct me.

Session Ranges Pro+Session Range Zones – Professional Edition

OVERVIEW

Professional visualization of the classic opening-range / Initial Balance concept across Asian, London, and Regular (US) sessions.

Displays the high/low of the user-defined opening window as thick, hierarchical filled zones with optional Fibonacci and standard-deviation extensions plus full alerting.

CONCEPT BACKGROUND

Using the high and low of the first 30–60 minutes of a session as key support/resistance is public-domain knowledge that has been standard in institutional trading for decades (Initial Balance, Opening Range, Session Range, etc.).

On TradingView the same principle was popularized under the name “Defining / DealingRange / DR/IDR” by TheMas7er and others.

IMPLEMENTATION & VALUE ADDED

This indicator follows the established, public-domain range-calculation methodology but has been completely rewritten with the following original enhancements:

• Clean, filled High / Mid / Low zones for instant visual hierarchy

• Intuitive Asian / London / Regular session labelling and fully custom timing

• Comprehensive dynamic & static Fibonacci and 50%/100% standard-deviation extensions

• Alert conditions on every zone, midline, opening level, and extension line

• Modern, modular code architecture using arrays and custom drawing functions

• No repainting, lightweight performance on any intraday timeframe

HOW TO USE

Apply to 1–15 min charts. Select desired sessions and formation period (30 or 60 min typical).

Shaded zones serve as primary support/resistance; extensions provide measured-move targets.

CREDIT & TRANSPARENCY

Core methodology: public domain (Initial Balance / Opening Range / Session Range).

Early TradingView popularization of the DR/IDR naming and feature set: TheMas7er **(with thanks to community contributors like bmsitiaan and trading-guide for refinements)**.

**Utilizes PineCoders' VisibleChart library for optimized chart rendering.**

This script uses the same foundational principle and logical input options but is an independent implementation. All visual presentation, zone system, multi-session handling, extension systems, alerting framework, and underlying code structure are original.

DISCLAIMER

For educational and informational purposes only. Not financial advice. Past performance is no guarantee of future results. Test thoroughly on your instruments and timeframes.

PonoTrading WDRWeekly Dealing Range Indicator

Overview

The Weekly Dealing Range indicator identifies range + volatility based pivot levels that form at the close of the first trading session and extend for the entire week. This tool provides key reference points for both trending and range-bound market conditions.

What It Provides

Range High & Low: Weekly session extremes

Median Level: Mid-point of the weekly range

Weekly Open: First session opening price

Standard Deviation Extensions: Calculated levels above the high and below the low

Practical Application

These levels serve as:

Reversal zones for mean reversion setups

Support/resistance reference points

Target levels for existing positions

Framework for building trade ideas around high-probability pivot areas

Key Features

Traditional price crosses level alerts

Automatically updates each week

Clean, uncluttered chart display

Works across all timeframes

Suitable for all markets and instruments

LGZ – Liquidity Gravity Zones v1 📌 LGZ – Liquidity Gravity Zones (SVI + Net CVD + Volume)

Original Liquidity-Driven Price Magnet Model by Thomas Aaroon

📘 Concept Overview

LGZ (Liquidity Gravity Zones) is a new, original liquidity-based price-attraction model built using three core components:

SVI (Shock Volume Index) – measures abnormal volume spikes at each strike

Net CVD (NCP = CE_CVD − PE_CVD) – the real directional order-flow imbalance

Total Volume (CE + PE) – true liquidity density at each strike

Using these three elements, the indicator calculates Liquidity Gravity Weight (LGW) for every strike and identifies the strongest zones that attract price during the session.

🧠 Why This Indicator?

Traditional OI-based methods (long build-up, short build-up, OI change etc.) often lag.

LGZ focuses only on:

Real traded volume

Actual buy/sell aggression (CVD)

Shock events

Dealer hedging pressure

Strike-level liquidity clusters

This makes it far more responsive for intraday traders.

⭐ Core Formula

Liquidity Gravity Weight (LGW)

LGW = |SVI| × |Net CVD| × Total Volume

Where:

SVI = Shock Volume Index (Z-score based)

Net CVD (NCP) = CE_CVD − PE_CVD

Total Volume = CE_volume + PE_volume

LGW indicates how strongly a strike is pulling price toward it.

🎯 What the Indicator Shows

✔ Top Liquidity Gravity Zones (LGZ-1, LGZ-2, LGZ-3)

These are the strongest price magnets for the day.

✔ Gravity Lines on Chart

Each LGZ is plotted as a horizontal magnet line extending to the right.

✔ Strike-Level Liquidity Table

Shows:

Strike

SVI (Shock intensity)

LGW (Gravity strength)

This table gives a complete picture of the intraday liquidity landscape.

📈 How to Use (Intraday Trading Strategy)

🔵 1. Price gravitates toward LGZ-1

If price is below LGZ-1 → upward pull

If price is above LGZ-1 → downward pull

🔵 2. LGZ Flips = Trend Change

If LGZ-1 suddenly jumps to a different strike:

→ strong trend acceleration

🔵 3. LGZ Cluster = Reversal / Consolidation Zone

Multiple LGZ levels around the same strike indicate

→ liquidity saturation → reversal or slowdown.

🔵 4. Combine with Price Action

Best clarity on 5-minute timeframe

Use 1-minute only for entry.

🔬 Why LGZ Works

The indicator models the same reality driving option markets:

Where option volume + orderflow (CVD) + shock liquidity concentrate,

market makers hedge, and price moves toward that strike.

This is the foundation of dealer hedging mechanics and liquidity-based price movement.

🔧 Inputs

Symbol prefix (e.g., NIFTY)

Expiry (YYMMDD)

Center strike & range

Number of gravity zones

Color customization

TVB - Thomas Volatility Bands v2.0TVB – Thomas Volatility Bands v2.0

Author: Thomas Aaroon

Concept: CIV-Driven Volatility Bands with Adaptive Vomma Scaling

Overview

TVB – Thomas Volatility Bands v2.0 is an advanced volatility-adaptive band system built on two core elements:

CIV (Composite Implied Volatility) – manually provided or proxied using an external IV index

Dynamic Vomma Scaling – a higher-order volatility response factor that adjusts band width based on the convexity of implied volatility changes

Together, these components create a continuously adapting volatility envelope that reacts smoothly to market regime shifts.

Key Features

1. Flexible CIV Input

Manual CIV mode: Enter your own CIV value (decimal or %)

Proxy CIV mode: Pulls IV data from INDIA_VIX or any custom IV symbol

Weighted blending: Adjustable α-weight for proxy influence

Automatic normalization ensures stable and bounded CIV values.

2. Adaptive Volatility Engine

CIV is smoothed using EMA for intraday and SMA for higher-timeframes

Vomma coefficient dynamically adjusts based on CIV percentile and short-term CIV volatility

Produces a volatility surface that expands during stress and contracts during calm periods.

3. Time-Scaled Band Construction

Bands automatically scale their width according to:

Timeframe multiplier

Estimated bars-per-day

Annualized volatility normalization (√252 rule)

This ensures consistent volatility geometry across all chart timeframes.

4. Dual-Layer Volatility Bands

Inner Bands (±3σ): Tactical mean-reversion boundaries

Outer Bands (±4σ): Structural deviation zones for extreme price dislocations

Smooth color-coded volatility regimes (low/moderate/high CIV).

5. Re-Entry Logic (34% Rule)

A clean, rule-based mechanism inspired by distributional penetration depth:

Tracks bars that break the ±4σ outer band

Looks for 34% penetration back toward the ±3σ region

Generates optional visual markers (buy/sell re-entry)

Designed to highlight volatility compression opportunities after extreme expansions.

6. Optional CIV Diagnostic Label

Shows:

CIV and smooth CIV

Vomma coefficient

Effective band width

Useful for strategy development and volatility research.

Intended Use

TVB v2.0 is designed for:

Volatility-based trading models

Mean-reversion and re-entry systems

Volatility regime identification

Institutional-grade market structure research

This indicator does not repaint and does not generate trade signals by default (signals can be enabled via optional shapes).

Disclaimer

This tool is for educational and analytical purposes only.

It is not financial advice, and the author is not responsible for any trading outcomes.

Order-Flow Proxy (VWAP Deviation Zones)Order-Flow Proxy (VWAP Deviation Zones) helps traders visualize when market price moves unusually far away from its Volume-Weighted Average Price (VWAP) — a key fair-value level used by institutional participants.

When price stretches too far above or below VWAP, it often signals temporary imbalance between buying and selling pressure.

This tool highlights those moments using simple color zones and an optional statistical Z-Score filter for deeper precision.

In short: it’s a clean, minimal mean-reversion indicator showing when price is statistically “too far” from fair value.

Red zone → Price extended above VWAP → possible buyer exhaustion or short setup.

Green zone → Price extended below VWAP → possible seller exhaustion or long setup.

VWAP line → Acts as a dynamic fair-value anchor.

Concept:

VWAP combines both price and traded volume to define where most transactions occurred.

Deviations from it — measured either by a fixed distance (1%) or by Z-Score — can reveal overvaluation or undervaluation zones used by professional traders for contrarian setups.

How to use:

Apply the indicator to any intraday chart (1m–1h recommended).

Watch for background color shifts — red or green.

Optionally enable the Z-Score filter to focus only on statistically extreme deviations.

Combine with volume spikes, liquidity sweeps, or your own order-flow tools for confirmation.

Tip:

Best used as a visual overlay for detecting stretched markets and potential reversals.

VWAP Reversion (Sequential Stats + Profit/Loss Points)First time posting. This is my attempt to evaluate the effectiveness of VWAP reversion. I decided to make this an indicator with its own integrated stats.

If you set the session length to lets say 100, but choose a 1 minute timeframe, it will only load as many sessions as the chart will allow for that timeframe. increasing the timeframe will allow you to go back further with more sessions.

I plan to implement more and more as I refine it. I just wanted to get my working copy out into the universe. I'd like to add some method of "scaling in". Perhaps if the price goes further and further away from the original entry, say for each additional std. deviation band further, it could add another entry signal.

My trading journey is just beginning, I've never coded before, and this was made entirely through the fusion of my attempt to communicate the ideas in my head for ChatGPT to turn into code!

Volume Weighted Volatility RegimeThe Volume-Weighted Volatility Regime (VWVR) is a market analysis tool that dissects total volatility to classify the current market 'character' or 'regime'. Using a Linear Regression model, it decomposes volatility into Trend, Residual (mean-reversion), and Within-Bar (noise) components.

Key Features:

Seven-Stage Regime Classification: The indicator's primary output is a regime value from -3 to +3, identifying the market state:

+3 (Strong Bull Trend): High directional, upward volatility.

+2 (Choppy Bull): Moderate upward trend with noise.

+1 (Quiet Bull): Low volatility, slight upward drift.

0 (Neutral): No clear directional bias.

-1 (Quiet Bear): Low volatility, slight downward drift.

-2 (Choppy Bear): Moderate downward trend with noise.

-3 (Strong Bear Trend): High directional, downward volatility.

Advanced Volatility Decomposition: The regime is derived from a three-component volatility model that separates price action into Trend (momentum), Residual (mean-reversion), and Within-Bar (noise) variance. The classification is determined by comparing the 'Trend' ratio against the user-defined 'Trend Threshold' and 'Quiet Threshold'.

Dual-Level Analysis: The indicator analyzes market character on two levels simultaneously:

Inter-Bar Regime (Background Color): Based on the main StdDev Length, showing the overall market character.

Intra-Bar Regime (Column Color): Based on a high-resolution analysis within each single bar ('Intra-Bar Timeframe'), showing the micro-structural character.

Calculation Options:

Statistical Model: The 'Estimate Bar Statistics' option (enabled by default) uses a statistical model ('Estimator') to perform the decomposition. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead).

Normalization: An optional 'Normalize Volatility' setting calculates an Exponential Regression Curve (log-space).

Volume Weighting: An option (Volume weighted) applies volume weighting to all volatility calculations.

Multi-Timeframe (MTF) Capability: The entire dual-level analysis can be run on a higher timeframe (using the Timeframe input), with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Integrated Alerts: Includes 22 comprehensive alerts that trigger whenever the 'Inter-Bar Regime' or the 'Intra-Bar Regime' crosses one of the key thresholds (e.g., 'Regime crosses above Neutral Line'), or when the 'Intra-Bar Dominance' crosses the 50% mark.

Caution: Real-Time Data Behavior (Intra-Bar Repainting) This indicator uses high-resolution intra-bar data. As a result, the values on the current, unclosed bar (the real-time bar) will update dynamically as new intra-bar data arrives. This behavior is normal and necessary for this type of analysis. Signals should only be considered final after the main chart bar has closed.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volume Weighted Intra Bar LR Standard DeviationThis indicator analyzes market character by providing a detailed view of volatility. It applies a Linear Regression model to intra-bar price action, dissecting the total volatility of each bar into three distinct components.

Key Features:

Three-Component Volatility Decomposition: By analyzing a lower timeframe ('Intra-Bar Timeframe'), the indicator separates each bar's volatility into:

Trend Volatility (Green/Red): Volatility explained by the intra-bar linear regression slope (Momentum).

Residual Volatility (Yellow): Volatility from price oscillating around the intra-bar trendline (Mean-Reversion).

Within-Bar Volatility (Blue): Volatility derived from the range of each intra-bar candle (Noise/Choppiness).

Layered Column Visualization: The indicator plots these components as a layered column chart. The size of each colored layer visually represents the dominance of each volatility character.

Dual Display Modes: The indicator offers two modes to visualize this decomposition:

Absolute Mode: Displays the total standard deviation as the column height, showing the absolute magnitude of volatility and the contribution of each component.

Normalized Mode: Displays the components as a 100% stacked column chart (scaled from 0 to 1), focusing purely on the percentage ratio of Trend, Residual, and Noise.

Calculation Options:

Statistical Model: The 'Estimate Bar Statistics' option (enabled by default) uses a statistical model ('Estimator') to perform the decomposition. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead).

Normalization: An optional 'Normalize Volatility' setting calculates an Exponential Regression Curve (log-space).

Volume Weighting: An option (Volume weighted) applies volume weighting to all intra-bar calculations.

Multi-Component Pivot Detection: Includes a pivot detector that identifies significant turning points (highs and lows) in both the Total Volatility and the Trend Volatility Ratio. (Note: These pivots are only plotted when 'Plot Mode' is set to 'Absolute').

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed, which introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF Analysis: The entire intra-bar analysis can be run on a higher timeframe (using the Timeframe input), with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes 9 comprehensive alerts for:

Volatility character changes (e.g., 'Character Change from Noise to Trend').

Dominant character emerging (e.g., 'Bullish Trend Character Emerging').

Total Volatility pivot (High/Low) detection.

Trend Volatility pivot (High/Low) detection.

Caution! Real-Time Data Behavior (Intra-Bar Repainting) This indicator uses high-resolution intra-bar data. As a result, the values on the current, unclosed bar (the real-time bar) will update dynamically as new intra-bar data arrives. This behavior is normal and necessary for this type of analysis. Signals should only be considered final after the main chart bar has closed.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volume Weighted Intra Bar Standard DeviationThis indicator provides a high-resolution analysis of market volatility by dissecting each bar on the chart into its fundamental components. It uses data from a lower, intra-bar timeframe to separate the total volatility of a single bar into its 'directional' and 'non-directional' parts.

Key Features:

Intra-Bar Volatility Decomposition: For each bar on the chart, the indicator analyzes the underlying price action on a smaller timeframe ('Intra-Bar Timeframe') and quantifies two types of volatility:

Between-Bar Volatility (Directional): Calculated from price movements between the intra-bar candles. This component represents the directional, trending price action within the main bar.

Within-Bar Volatility (Non-Directional): Calculated from price fluctuations inside each intra-bar candle. This component represents the choppy, noisy, or ranging price action.

Dual Display Modes: The indicator offers two modes to visualize this information:

Absolute Mode: Plots the total standard deviation as a stacked column chart, showing the absolute magnitude of volatility and the contribution of each component.

Normalized Mode: Plots the components as a 100% stacked column chart (scaled from 0 to 1), focusing purely on the percentage ratio of 'between-bar' (trending) and 'within-bar' (choppy) volatility.

Calculation Options:

Statistical Model: The 'Estimate Bar Statistics' option (enabled by default) uses a statistical model ('Estimator') to perform the decomposition. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead).

Normalization: An optional 'Normalize Volatility' setting calculates volatility in percentage terms (log-space).

Volume Weighting: An option (Volume weighted) applies volume weighting to all intra-bar volatility calculations.

Volatility Pivot Detection: Includes a built-in pivot detector that identifies significant turning points (highs and lows) in the total volatility line. (Note: This is only visible in 'Absolute Mode').

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed, which introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF Analysis Lines: The entire intra-bar analysis can be run on a higher timeframe (using the Timeframe input), with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes 6 alerts for:

Volatility character changes (e.g., 'Character Change from Choppy to Trend').

Dominant character emerging (e.g., 'Trend Character Emerging').

Total Volatility pivot (High/Low) detection.

Caution: Real-Time Data Behavior (Intra-Bar Repainting) This indicator uses high-resolution intra-bar data. As a result, the values on the current, unclosed bar (the real-time bar) will update dynamically as new intra-bar data arrives. This behavior is normal and necessary for this type of analysis. Signals should only be considered final after the main chart bar has closed.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volume Weighted LR Standard DeviationThis indicator analyzes market character by decomposing total volatility into three distinct, interpretable components based on a Linear Regression model.

Key Features:

Three-Component Volatility Decomposition: The indicator separates volatility based on the 'Estimate Bar Statistics' option.

Standard Mode (Estimate Bar Statistics = OFF): Calculates volatility based on the selected Source (dies führt hauptsächlich zu 'Trend'- und 'Residual'-Volatilität).

Decomposition Mode (Estimate Bar Statistics = ON): The indicator uses a statistical model ('Estimator') to calculate within-bar volatility. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead). This separates volatility into:

Trend Volatility (Green/Red): Volatility explained by the regression's slope (Momentum).

Residual Volatility (Yellow): Volatility from price oscillating around the regression line (Mean-Reversion).

Within-Bar Volatility (Blue): Volatility from the high-low range of each bar (Noise/Choppiness).

Dual Display Modes: The indicator offers two modes to visualize this decomposition:

Absolute Mode: Displays the total standard deviation as a stacked area chart, partitioned by the variance ratio of the three components.

Normalized Mode: Displays the direct variance ratio (proportion) of each component relative to the total (0-1), ideal for identifying the dominant market character.

Calculation Options:

Normalization: An optional 'Normalize Volatility' setting calculates an Exponential Regression Curve (log-space), making the analysis suitable for growth assets.

Volume Weighting: An option (Volume weighted) applies volume weighting to all regression and volatility calculations.

Multi-Component Pivot Detection: Includes a pivot detector that identifies significant turning points (highs and lows) in both the Total Volatility and the Trend Volatility Ratio. (Note: These pivots are only plotted when 'Plot Mode' is set to 'Absolute').

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed, which introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF Volatility Lines: The volatility lines can be calculated on a higher timeframe, with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes 9 comprehensive alerts for:

Volatility character changes (e.g., 'Character Change from Noise to Trend').

Dominant character emerging (e.g., 'Bullish Trend Character Emerging').

Total Volatility pivot (High/Low) detection.

Trend Volatility pivot (High/Low) detection.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volume Weighted Standard DeviationThis indicator calculates the Standard Deviation and decomposes total volatility into its core components, allowing to analyze the underlying character of the market.

Key Features:

Volatility Decomposition: The indicator separates volatility based on the 'Estimate Bar Statistics' option.

Standard Mode (Estimate Bar Statistics = OFF): Calculates a simple (Volume-Weighted) Standard Deviation of the selected Source.

Decomposition Mode (Estimate Bar Statistics = ON): The indicator uses a statistical model ('Estimator') to calculate within-bar volatility (choppiness, noise) and between-bar volatility (trending moves). (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used instead).

Dual Display Modes: The indicator offers two modes to visualize this information:

Absolute Mode: Plots the total standard deviation as a stacked area chart, showing the proportional contribution of the 'Between' and 'Within' components.

Normalized Mode: Plots the direct ratio of each component's variance (from 0 to 1), making it easy to identify which character is dominant.

Calculation Options: The volatility calculation can be optionally Volume weighted. An optional Normalize Volatility setting performs the calculation in logarithmic space, making volatility comparable across different price scales.

Volatility Pivot Detection: Includes a built-in pivot detector that identifies significant turning points (highs and lows) in the total volatility line. (Note: This is only visible in 'Absolute Mode').

Note on Confirmation (Lag): Pivot signals are confirmed using a lookback method. A pivot is only plotted after the Pivot Right Bars input has passed, which introduces an inherent lag.

Multi-Timeframe (MTF) Capability:

MTF Volatility Lines: The volatility lines can be calculated on a higher timeframe, with standard options to handle gaps (Fill Gaps) and prevent repainting (Wait for...).

Limitation: The Pivot detection (Calculate Pivots) is disabled if a Higher Timeframe (HTF) is selected.

Integrated Alerts: Includes 6 alerts for:

Volatility character changes (e.g., 'Trend Character Emerging', 'Character Change from Trend to Choppy').

Volatility pivot (high or low) detection.

DISCLAIMER

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Volatility Cones **Volatility Cones - Interactive**

This indicator visualizes volatility cones based on historical or manual volatility and projects them up to 252 trading days into the future.

**Features:**

- Automatic start at the first trading day of the year (customizable)

- Volatility calculation from historical data or manual input

- Display of ±1σ, ±2σ, and ±3σ bands

- Projection of expected price movements based on volatility

**Use Case:**

Ideal for options traders and risk management to assess expected price movements over different time horizons.