Fourier Adjusted Average True Range [BackQuant]Fourier Adjusted Average True Range

1. Conceptual Foundation and Innovation

The FA-ATR leverages the principles of Fourier analysis to dissect market prices into their constituent cyclical components. By applying Fourier Transform to the price data, the FA-ATR captures the dominant cycles and trends which are often obscured in noisy market data. This integration allows the FA-ATR to adapt its readings based on underlying market dynamics, offering a refined view of volatility that is sensitive to both market direction and momentum.

2. Technical Composition and Calculation

The core of the FA-ATR involves calculating the traditional ATR, which measures market volatility by decomposing the entire range of price movements. The FA-ATR extends this by incorporating a Fourier Transform of price data to assess cyclical patterns over a user-defined period 'N'. This process synthesizes both the magnitude of price changes and their rhythmic occurrences, resulting in a more comprehensive volatility indicator.

Fourier Transform Application: The Fourier series is calculated using price data to identify the fundamental frequency of market movements. This frequency helps in adjusting the ATR to reflect more accurately the current market conditions.

Dynamic Adjustment: The ATR is then adjusted by the magnitude of the dominant cycle from the Fourier analysis, enhancing or reducing the ATR value based on the intensity and phase of market cycles.

3. Features and User Inputs

Customizability: Traders can modify the Fourier period, ATR period, and the multiplication factor to suit different trading styles and market environments.

Visualization : The FA-ATR can be plotted directly on the chart, providing a visual representation of volatility. Additionally, the option to paint candles according to the trend direction enhances the usability and interpretative ease of the indicator.

Confluence with Moving Averages: Optionally, a moving average of the FA-ATR can be displayed, serving as a confluence factor for confirming trends or potential reversals.

4. Practical Applications

The FA-ATR is particularly useful in markets characterized by periodic fluctuations or those that exhibit strong cyclical trends. Traders can utilize this indicator to:

Adjust Stop-Loss Orders: More accurately set stop-loss orders based on a volatility measure that accounts for cyclical market changes.

Trend Confirmation: Use the FA-ATR to confirm trend strength and sustainability, helping to avoid false signals often encountered in volatile markets.

Strategic Entry and Exit: The indicator's responsiveness to changing market dynamics makes it an excellent tool for planning entries and exits in a trend-following or a breakout trading strategy.

5. Advantages and Strategic Value

By integrating Fourier analysis, the FA-ATR provides a volatility measure that is both adaptive and anticipatory, giving traders a forward-looking tool that adjusts to changes before they become apparent through traditional indicators. This anticipatory feature makes it an invaluable asset for traders looking to gain an edge in fast-paced and rapidly changing market conditions.

6. Summary and Usage Tips

The Fourier Adjusted Average True Range is a cutting-edge development in technical analysis, offering traders an enhanced tool for assessing market volatility with increased accuracy and responsiveness. Its ability to adapt to the market's cyclical nature makes it particularly useful for those trading in highly volatile or cyclically influenced markets.

Traders are encouraged to integrate the FA-ATR into their trading systems as a supplementary tool to improve risk management and decision-making accuracy, thereby potentially increasing the effectiveness of their trading strategies.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Average

FVG Positioning Average [LuxAlgo]The FVG Positioning Average indicator aims to uncover potential price levels of interest by averaging together recent Fair Value Gap (FVG) initiation levels.

This indicator is grounded in the theory that significant buying or selling activity is the primary catalyst for creating FVGs.

By averaging together the prices where each FVG initiated, we may potentially reveal where major participants are positioned.

🔶 USAGE

By analyzing the average price of bullish or bearish FVGs, users can identify potential support or resistance areas where the larger participants may re-enter or defend their positions.

These areas could be used to adjust entries and exits or assist with risk management such as take-profit or stop-loss levels.

The indicator displays 2 lines, the Bull Average and the Bear Average.

The Bull Average is only displayed when the price holds above the bull Average.

The Bear Average is only displayed when the price holds below the bear average.

When only one average is displayed alone, this level is seen as support or resistance, it is anticipated that this level would be defended for the current trend to stay valid.

When both averages are displayed simultaneously, it can be interpreted as one side attempting to take over the trend.

The movements and reactions during these attempts can be analyzed to provide helpful information about where the price might be headed.

Possible outcomes:

Trend Confirmation/Re-Entry (From Weak Attempts)

Trend Reversal (Creating Support or Resistance)

Consolidation (Oscillating between/around Bull & Bear Averages)

🔶 DETAILS

🔹 Lookback Types

This indicator includes 2 lookback types:

Bar Count: Uses Bars to determine what data to include. This type can be utilized for averages that are more locally relevant to the current chart data.

FVG Count: Uses a specific # of FVGs for calculations. This type can be utilized for a continuous & consistent view, typically relevant with longer term analysis.

Note: When using bar lookback, if no data is in range, no lines will be displayed.

Below is an example of the 'FVG Count' Display.

🔹 Initiation Levels

Initiation Levels are the specific price points where each FVG starts, these are the last points the price was traded at before creating the gap.

Bull Initiation Level: Lowest Point (Bottom) of FVG

Bear Initiation Level: Highest Point (Top) of FVG

🔹 FVG Display

Each FVG being used for the current calculation of averages is displayed on the chart for reference.

Note: If you prefer to not display the FVGs, they can be toggled off in the settings, uncheck "Show FVGs on Chart".

🔶 Settings

FVG Lookback: As mentioned above in the 'Lookback Types', this sets the number of FVGs or Bars to use for consideration.

Lookback Type: As also mentioned above in 'Lookback Types', this determines the method of lookback to be used.

ATR Multiplier: The FVGs are required to have a Greater Width than (ATR * Multiplier) in order to be used for calculations. This allows you to focus on the data being considered if needed.

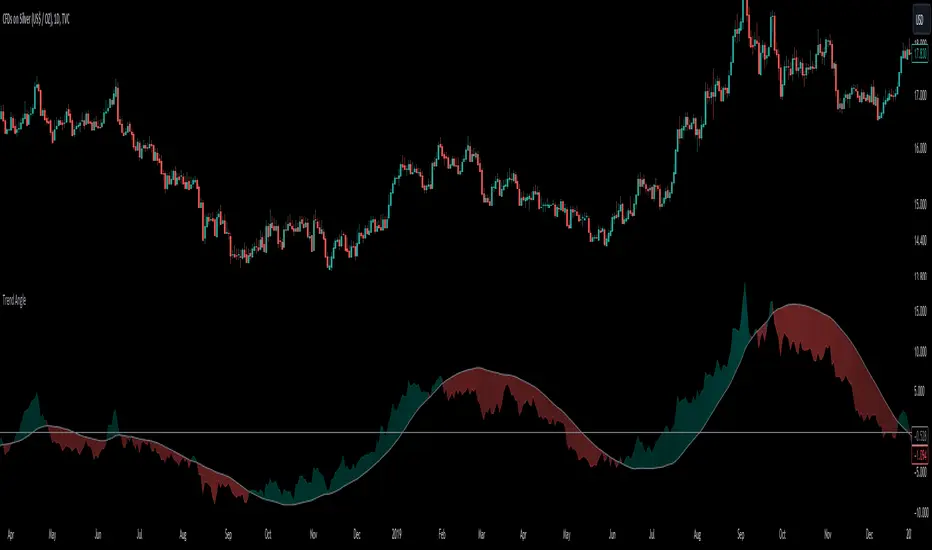

Trend AngleThe "Trend Angle" indicator serves as a tool for traders to decipher market trends through a methodical lens. It quantifies the inclination of price movements within a specified timeframe, making it easy to understand current trend dynamics.

Conceptual Foundation:

Angle Measurement: The essence of the "Trend Angle" indicator is its ability to compute the angle between the price trajectory over a defined period and the horizontal axis. This is achieved through the calculation of the arctangent of the percentage price change, offering a straightforward measure of market directionality.

Smoothing Mechanisms: The indicator incorporates options for "Moving Average" and "Linear Regression" as smoothing mechanisms. This adaptability allows for refined trend analysis, catering to diverse market conditions and individual preferences.

Functional Versatility:

Source Adaptability: The indicator affords the flexibility to select the desired price source, enabling users to tailor the angle calculation to their analytical framework and other indicators.

Detrending Capability: With the detrending feature, the indicator allows for the subtraction of the smoothing line from the calculated angle, highlighting deviations from the main trend. This is particularly useful for identifying potential trend reversals or significant market shifts.

Customizable Period: The 'Length' parameter empowers traders to define the observation window for both the trend angle calculation and its smoothing, accommodating various trading horizons.

Visual Intuition: The optional colorization enhances interpretability, with the indicator's color shifting based on its relation to the smoothing line, thereby providing an immediate visual cue regarding the trend's direction.

Interpretative Results:

Market Flatness: An angle proximate to 0 suggests a flat market condition, indicating a lack of significant directional movement. This insight can be pivotal for traders in assessing market stagnation.

Trending Market: Conversely, a relatively high angle denotes a trending market, signifying strong directional momentum. This distinction is crucial for traders aiming to capitalize on trend-driven opportunities.

Analytical Nuance vs. Simplicity:

While the "Trend Angle" indicator is underpinned by mathematical principles, its utility lies in its simplicity and interpretative clarity. However, it is imperative to acknowledge that this tool should be employed as part of a comprehensive trading strategy , complemented by other analytical instruments for a holistic market analysis.

In essence, the "Trend Angle" indicator exemplifies the harmonization of simplicity and analytical rigor. Its design respects the complexity of market behaviors while offering straightforward, actionable insights, making it a valuable component in the arsenal of both seasoned and novice traders alike.

RWEDT Weighted Moving Average Overview:

The RWEDT MA, which is short for rolling, weighted, exponential, double exponential, and triple exponential, is a group of moving averages that were subjected to a log transformation to deal with the skewness of price, and the weight of each of these moving averages was also used for calculating the standard deviations from the mean.

Clearing a misunderstanding on Standard Deviation Bands and Moving Averages

Bands, such as standard deviation bands, are frequently misinterpreted as indicators of support and resistance levels or as "mean-reverting" indicators." However, this is not their intended purpose. Bands are statistical tools that provide ranges within which price (in this case) movements are expected to occur based on historical data. Deviations beyond these bands suggest a decrease in confidence in the model rather than a reversal back to a moving average or a "support/resistance level."

Example : Assuming you correctly applied a log transformation to your standard deviation bands to remove the right skew, and assuming your data closely resembles a normal distribution or some other type of symmetrical distribution, then the probability of a value being in the 2 standard deviation range is around 95%. This does not mean it will reject or go up, or mean revert. The price won't bounce from -2 STDEV 95% of the time; that is incorrect. It just tells you that around 95% of the values will be within the 2 SD range.

Moving averages, including the ones in this indicator, are often misinterpreted as signals of trend reversals or levels of "bouncing." What moving averages actually tell you is what the expected value is. It does not show where you expect the price to be in the future; it tells you that based on the lookback, the expected value is in the center, and the confidence you have in the estimate is the confidence interval or the standard deviation range.

Example: Let's say you enter a trade with a positive expected value (expecting the price to drift up), and we have the limits set at 95%. What it tells you is that as long as the price stays within the limits, you can be 95% certain the model isn't completely random. As the price moves further away from the average, or expected value, it tells you that the model is less likely to be correct.

RWEDT MA

This indicator comes with 5 moving averages, each log transformed to reduce the skewness and asymmetry of price as much as possible

Rolling

Weighted

Exponential

Double Exponential

Triple Exponential

The band standard deviation can be adjusted, and the standard deviations have the weight of all of the moving averages that are present in the indicator. The weight is not customizable.

Why this indicator is useful:

This indicator can tell you what the expected value is. Above the moving average signifies a positive expected value, and below the moving average signifies a negative expected value. As previously stated above, the price moving further from the expected value lets you know that you should have less confidence that the model is "correct," and you could see this as taking profits as the price deviates further from the expected value.

The importance of log-transforming prices for standard deviations and moving averages.

Symmetry: Logarithmic transformations can help achieve symmetry in the distribution of price data. Stock prices, for example, exhibit some type of right-skewed distribution, where large positive price movements are more common than large negative movements. Price also can't go below 0 but can go towards positive infinity, so having a right-skew makes sense; all the outliers will be towards infinity, while all the average occurrences are "near" 0.

Stabilizing Variance: Price data typically exhibit heteroscedasticity, meaning that the variance of price movements changes over time. Log transformations can stabilize the variance and make it more consistent across different price levels. This is important for ensuring that the variability in price moves is not disproportionately influenced by extreme values.

Statistical Assumptions: Many retail indicators like Bollinger Bands use the standard deviation and moving average models of a normal distribution to attempt to model price, whose distribution more closely resembles some type of right-skew distribution. Even with the log-transformation, it still won't always resemble a perfect symmetrical distribution, and you still should not use it for mean reversion. You can still use it to understand the expected value and whether or not you should have confidence in your model.

PhiSmoother Moving Average Ribbon [ChartPrime]DSP FILTRATION PRIMER:

DSP (Digital Signal Processing) filtration plays a critical role with financial indication analysis, involving the application of digital filters to extract actionable insights from data. Its primary trading purpose is to distinguish and isolate relevant signals separate from market noise, allowing traders to enhance focus on underlying trends and patterns. By smoothing out price data, DSP filters aid with trend detection, facilitating the formulation of more effective trading techniques.

Additionally, DSP filtration can play an impactful role with detecting support and resistance levels within financial movements. By filtering out noise and emphasizing significant price movements, identifying key levels for entry and exit points become more apparent. Furthermore, DSP methods are instrumental in measuring market volatility, enabling traders to assess volatility levels with improved accuracy.

In summary, DSP filtration techniques are versatile tools for traders and analysts, enhancing decision-making processes in financial markets. By mitigating noise and highlighting relevant signals, DSP filtration improves the overall quality of trading analysis, ultimately leading to better conclusions for market participants.

APPLYING FIR FILTERS:

FIR (Finite Impulse Response) filters are indispensable tools in the realm of financial analysis, particularly for trend identification and characterization within market data. These filters effectively smooth out price fluctuations and noise, enabling traders to discern underlying trends with greater fidelity. By applying FIR filters to price data, robust trading strategies can be developed with grounded trend-following principles, enhancing their ability to capitalize on market movements.

Moreover, FIR filter applications extend into wide-ranging utility within various fields, one being vital for informed decision-making in analysis. These filters help identify critical price levels where assets may tend to stall or reverse direction, providing traders with valuable insights to aid with identification of optimal entry and exit points within their indicator arsenal. FIRs are undoubtedly a cornerstone to modern trading innovation.

Additionally, FIR filters aid in volatility measurement and analysis, allowing traders to gauge market volatility accurately and adjust their risk management approaches accordingly. By incorporating FIR filters into their analytical arsenal, traders can improve the quality of their decision-making processes and achieve better trading outcomes when contending with highly dynamic market conditions.

INTRODUCTORY DEBUT:

ChartPrime's " PhiSmoother Moving Average Ribbon " indicator aims to mark a significant advancement in technical analysis methodology by removing unwanted fluctuations and disturbances while minimizing phase disturbance and lag. This indicator introduces PhiSmoother, a powerful FIR filter in it's own right comparable to Ehlers' SuperSmoother.

PhiSmoother leverages a custom tailored FIR filter to smooth out price fluctuations by mitigating aliasing noise problematic to identification of underlying trends with accuracy. With adjustable parameters such as phase control, traders can fine-tune the indicator to suit their specific analytical needs, providing a flexible and customizable solution.

Mathemagically, PhiSmoother incorporates various color coding preferences, enabling traders to visualize trends more effectively on a volatile landscape. Whether utilizing progression, chameleon, or binary color schemes, you can more fluidly interpret market dynamics and make informed visual decisions regarding entry and exit points based on color-coded plotting.

The indicator's alert system further enhances its utility by providing notifications of specifically chosen filter crossings. Traders can customize alert modes and messages while ensuring they stay informed about potential opportunities aligned with their trading style.

Overall, the "PhiSmoother Moving Average Ribbon" visually stands out as a revolutionary mechanism for technical analysis, offering traders a comprehensive solution for trend identification, visualization, and alerting within financial markets to achieve advantageous outcomes.

NOTEWORTHY SETTINGS FEATURES:

Price Source Selection - The indicator offers flexibility in choosing the price source for analysis. Traders can select from multiple options.

Phase Control Parameter - One of the notable standout features of this indicator is the phase control parameter. Traders can fine-tune the phase or lag of the indicator to adapt it to different market conditions or timeframes. This feature enables optimization of the indicator's responsiveness to price movements and align it with their specific trading tactics.

Coloring Preferences - Another magical setting is the coloring features, one being "Chameleon Color Magic". Traders can customize the color scheme of the indicator based on their visual preferences or to improve interpretation. The indicator offers options such as progression, chameleon, or binary color schemes, all having versatility to dynamically visualize market trends and patterns. Two colors may be specifically chosen to reduce overlay indicator interference while also contrasting for your visual acuity.

Alert Controls - The indicator provides diverse alert controls to manage alerts for specific market events, depending on their trading preferences.

Alertable Crossings: Receive an alert based on selectable predefined crossovers between moving average neighbors

Customizable Alert Messages: Traders can personalize alert messages with preferred information details

Alert Frequency Control: The frequency of alerts is adjustable for maximum control of timely notifications

EMA + Lower Timeframe EMA (correct display in Replay Mode)This indicator shows

one EMA for the current timeframe

one EMA for a lower timeframe

Unlike the built-in Tradingview EMA indicator, this indicator shows the correct values for the lower timeframe EMA during Replay Mode.

ADR % RangesThis indicator is designed to visually represent percentage lines from the open of the day. The % amount is determined by X amount of the last days to create an average...or Average Daily Range (ADR).

1. ADR Percentage Lines: The core function of the script is to apply lines to the chart that represent specific percentage changes from the daily open. It first calculates the average over X amount of days and then displays two lines that are 1/3rd of that average. One line goes above the other line goes below. The other two lines are the full "range" of the average. These lines can act as boundaries or targets to know how an asset has moved recently. *Past performance is not indicative of current or future results.

The calculation for ADR is:

Step 1. Calculate Today's Range = DailyHigh - DailyLow

Step 2. Store this average after the day has completed

Step 3. Sum all day's ranges

Step 4. Divide by total number of days

Step 5. Draw on chart

2. Customizable Inputs: Users have the flexibility to customize the script through various inputs. This includes the option to display lines only for the current trading day (`todayonly`), and to select which lines are displayed. The user can also opt to show a table the displays the total range of previous days and the average range of those previous days.

3. No Secondary Timeframe: The ADR is computed based on whatever timeframe the chart is and does not reference secondary periods. Therefore the script cannot be used on charts greater than daily.

This script is can be used by all traders for any market. The trader might have to adjust the "X" number of days back to compute a historical average. Maybe they only want to know the average over the past week (5 days) or maybe the past month (20 days).

[AIO] Multi Collection Moving Averages 140 MA TypesAll In One Multi Collection Moving Averages.

Since signing up 2 years ago, I have been collecting various Сollections.

I decided to get it into a decent shape and make it one of the biggest collections on TV, and maybe the entire internet.

And now I'm sharing my collection with you.

140 Different Types of Moving Averages are waiting for you.

Specifically :

"

AARMA | Adaptive Autonomous Recursive Moving Average

ADMA | Adjusted Moving Average

ADXMA | Average Directional Moving Average

ADXVMA | Average Directional Volatility Moving Average

AHMA | Ahrens Moving Average

ALF | Ehler Adaptive Laguerre Filter

ALMA | Arnaud Legoux Moving Average

ALSMA | Adaptive Least Squares

ALXMA | Alexander Moving Average

AMA | Adaptive Moving Average

ARI | Unknown

ARSI | Adaptive RSI Moving Average

AUF | Auto Filter

AUTL | Auto-Line

BAMA | Bryant Adaptive Moving Average

BFMA | Blackman Filter Moving Average

CMA | Corrected Moving Average

CORMA | Correlation Moving Average

COVEMA | Coefficient of Variation Weighted Exponential Moving Average

COVNA | Coefficient of Variation Weighted Moving Average

CTI | Coral Trend Indicator

DEC | Ehlers Simple Decycler

DEMA | Double EMA Moving Average

DEVS | Ehlers - Deviation Scaled Moving Average

DONEMA | Donchian Extremum Moving Average

DONMA | Donchian Moving Average

DSEMA | Double Smoothed Exponential Moving Average

DSWF | Damped Sine Wave Weighted Filter

DWMA | Double Weighted Moving Average

E2PBF | Ehlers 2-Pole Butterworth Filter

E2SSF | Ehlers 2-Pole Super Smoother Filter

E3PBF | Ehlers 3-Pole Butterworth Filter

E3SSF | Ehlers 3-Pole Super Smoother Filter

EDMA | Exponentially Deviating Moving Average (MZ EDMA)

EDSMA | Ehlers Dynamic Smoothed Moving Average

EEO | Ehlers Modified Elliptic Filter Optimum

EFRAMA | Ehlers Modified Fractal Adaptive Moving Average

EHMA | Exponential Hull Moving Average

EIT | Ehlers Instantaneous Trendline

ELF | Ehler Laguerre filter

EMA | Exponential Moving Average

EMARSI | EMARSI

EPF | Edge Preserving Filter

EPMA | End Point Moving Average

EREA | Ehlers Reverse Exponential Moving Average

ESSF | Ehlers Super Smoother Filter 2-pole

ETMA | Exponential Triangular Moving Average

EVMA | Elastic Volume Weighted Moving Average

FAMA | Following Adaptive Moving Average

FEMA | Fast Exponential Moving Average

FIBWMA | Fibonacci Weighted Moving Average

FLSMA | Fisher Least Squares Moving Average

FRAMA | Ehlers - Fractal Adaptive Moving Average

FX | Fibonacci X Level

GAUS | Ehlers - Gaussian Filter

GHL | Gann High Low

GMA | Gaussian Moving Average

GMMA | Geometric Mean Moving Average

HCF | Hybrid Convolution Filter

HEMA | Holt Exponential Moving Average

HKAMA | Hilbert based Kaufman Adaptive Moving Average

HMA | Harmonic Moving Average

HSMA | Hirashima Sugita Moving Average

HULL | Hull Moving Average

HULLT | Hull Triple Moving Average

HWMA | Henderson Weighted Moving Average

IE2 | Early T3 by Tim Tilson

IIRF | Infinite Impulse Response Filter

ILRS | Integral of Linear Regression Slope

JMA | Jurik Moving Average

KA | Unknown

KAMA | Kaufman Adaptive Moving Average & Apirine Adaptive MA

KIJUN | KIJUN

KIJUN2 | Kijun v2

LAG | Ehlers - Laguerre Filter

LCLSMA | 1LC-LSMA (1 line code lsma with 3 functions)

LEMA | Leader Exponential Moving Average

LLMA | Low-Lag Moving Average

LMA | Leo Moving Average

LP | Unknown

LRL | Linear Regression Line

LSMA | Least Squares Moving Average / Linear Regression Curve

LTB | Unknown

LWMA | Linear Weighted Moving Average

MAMA | MAMA - MESA Adaptive Moving Average

MAVW | Mavilim Weighted Moving Average

MCGD | McGinley Dynamic Moving Average

MF | Modular Filter

MID | Median Moving Average / Percentile Nearest Rank

MNMA | McNicholl Moving Average

MTMA | Unknown

MVSMA | Minimum Variance SMA

NLMA | Non-lag Moving Average

NWMA | Dürschner 3rd Generation Moving Average (New WMA)

PKF | Parametric Kalman Filter

PWMA | Parabolic Weighted Moving Average

QEMA | Quadruple Exponential Moving Average

QMA | Quick Moving Average

REMA | Regularized Exponential Moving Average

REPMA | Repulsion Moving Average

RGEMA | Range Exponential Moving Average

RMA | Welles Wilders Smoothing Moving Average

RMF | Recursive Median Filter

RMTA | Recursive Moving Trend Average

RSMA | Relative Strength Moving Average - based on RSI

RSRMA | Right Sided Ricker MA

RWMA | Regressively Weighted Moving Average

SAMA | Slope Adaptive Moving Average

SFMA | Smoother Filter Moving Average

SMA | Simple Moving Average

SSB | Senkou Span B

SSF | Ehlers - Super Smoother Filter P2

SSMA | Super Smooth Moving Average

STMA | Unknown

SWMA | Self-Weighted Moving Average

SW_MA | Sine-Weighted Moving Average

TEMA | Triple Exponential Moving Average

THMA | Triple Exponential Hull Moving Average

TL | Unknown

TMA | Triangular Moving Average

TPBF | Three-pole Ehlers Butterworth

TRAMA | Trend Regularity Adaptive Moving Average

TSF | True Strength Force

TT3 | Tilson (3rd Degree) Moving Average

VAMA | Volatility Adjusted Moving Average

VAMAF | Volume Adjusted Moving Average Function

VAR | Vector Autoregression Moving Average

VBMA | Variable Moving Average

VHMA | Vertical Horizontal Moving Average

VIDYA | Variable Index Dynamic Average

VMA | Volume Moving Average

VSO | Unknown

VWMA | Volume Weighted Moving Average

WCD | Unknown

WMA | Weighted Moving Average

XEMA | Optimized Exponential Moving Average

ZEMA | Zero Lag Moving Average

ZLDEMA | Zero-Lag Double Exponential Moving Average

ZLEMA | Ehlers - Zero Lag Exponential Moving Average

ZLTEMA | Zero-Lag Triple Exponential Moving Average

ZSMA | Zero-Lag Simple Moving Average

"

Don't forget that you can use any Moving Average not only for the chart but also for any of your indicators without affecting the code as in my example.

But remember that some MAs are not designed to work with anything other than a chart.

All MA and Code lists are sorted strictly alphabetically by short name (A-Z).

Each MA has its own number (ID) by which you can display the Moving Average you need.

Next to the ID selection there are tooltips with short names and their numbers. Use them.

The panel below will help you to read the Name of the selected MA.

Because of the size of the collection I think this is the optimal and most convenient use. Correct me if this is not the case.

Unknown - Some MAs I collected so long ago that I lost the full real name and couldn't find the authors. If you recognize them, please let me know.

I have deliberately simplified all MAs to input just Source and Length.

Because the collection is so large, it would be quite inconvenient and difficult to customize all MA functions (multipliers, offset, etc.).

If you need or like any MA you will still have to take it from my collection for your code.

I tried to leave the basic MA settings inside function in first strings.

I have tried to list most of the authors, but since the bulk of the collection was created a long time ago and was not intended for public publication I could not find all of them.

Some of the features were created from scratch or may have been slightly modified, so please be careful.

If you would like to improve this collection, please write to me in PM.

Also Credits, Likes, Awards, Loves and Thanks to :

@alexgrover

@allanster

@andre_007

@auroagwei

@blackcat1402

@bsharpe

@cheatcountry

@CrackingCryptocurrency

@Duyck

@ErwinBeckers

@everget

@glaz

@gotbeatz26107

@HPotter

@io72signals

@JacobAmos

@JoshuaMcGowan

@KivancOzbilgic

@LazyBear

@loxx

@LuxAlgo

@MightyZinger

@nemozny

@NGBaltic

@peacefulLizard50262

@RicardoSantos

@StalexBot

@ThiagoSchmitz

@TradingView

— 𝐀𝐧𝐝 𝐎𝐭𝐡𝐞𝐫𝐬 !

So just a Big Thank You to everyone who has ever and anywhere shared their codes.

Geometrical Mean Moving AverageThe geometric moving average is a type of moving average that calculates the geometric mean of the previous n-periods of the price time series. Unlike the simple moving average that uses the arithmetic mean to continuously calculate the moving average as new price data comes in, the geometric moving average uses the geometric mean formula to get the moving average of the price data as new ones come in.

Why use a geometric moving average?

The geometric moving average differs from the simple moving average in how it is calculated. Most importantly, the geometric mean takes into account the compounding that occurs from period to period.

How can you use a geometric mean moving average?

You can use the GMMA just as you would use any other moving average indicator. You can use it to identify the direction of the trend, and in this case, it can also serve as a support level during an uptrend or a resistance level during a downtrend.

Drawbacks with a geometric moving average

Just like other moving average indicators, the GMA has limitations. Some of them are as follows:

It lags because it uses past price data.

It is pretty useless when the price action is choppy or moving predominantly sideways. During such periods, it can give multiple false signals.

YinYang RSIYinYang RSI is a Momentum Oscillator. It is loosely based on the standard RSI but uses our Custom True Value Zone Algorithm. Essentially it is a stronger, more accurate RSI that isn't manipulated by consolidation. YinYang RSI moves slightly slower than the standard RSI but when it does move it is much more accurate.

Why do we deem YinYang RSI to be a more accurate RSI? Well, let's discuss some of the underlying logic behind it. YinYang RSI is derived from the High and Low data from multiple Security Requests, we send that data into a modified Donchian Channel to calculate its Basis. That basis is then taken and averaged between multiple different VWMA calculations to ‘Smooth’ it out before we send it into an RSI calculation and display the final results.

This may sound a little confusing and you may be wondering, why bother doing this? The main reason we created the YinYang RSI is to remove the fact that consolidation causes Regular RSI to go down in index value. In our opinion RSI shouldn’t go down due to consolidation. By removing consolidation from RSI it innately made the RSI more smooth and since it became more smooth there were less times it crossed the RSI Moving Average (MA). In turn, since it crosses the RSI MA less, it means when it does cross the RSI MA, it is a much stronger more accurate signal; but don’t just take our word for it! Let’s get into some examples to show you exactly how it works:

Our RSI is very smooth, because of the way we apply VWMA to it, it keeps it from being a jagged line like the regular RSI is:

Our Indicator features 3 RSI’s in it: YinYangRSI, Regular RSI and YinYang Stoch RSI. The reason there are 3 is not only for the Information Tables (we will talk about this later), but also for the fact that you can overlay them on top of each other.

Here is the same dates but with Regular RSI:

Hopefully you can see how different they are and how smooth ours is, but if not, lets overlay them so you get a better idea:

When the YinYang RSI and Regular RSI are overlaid on top of each other, the Regular RSI’s colors change for easier readability. The Regular RSI turns Pink and the Regular RSI MA turns Orange. As you can see here, they function much differently and it is quite clear that the YinYang RSI holds itself during consolidation and is more smooth.

You may be asking yourself, this is great and all, but how does it help me trade?

Well, now that you understand the difference between YinYang and Regular RSI let's discuss exactly that!

So as you can see in the image above, when the RSI crosses the RSI MA it represents a strong movement in price is likely about to occur. When the RSI is very low (20 or less) and it crosses ABOVE the RSI MA, this represents a BUY/LONG signal. When the RSI is very high (80 or above) and it crosses BELOW the RSI MA, this represents a SELL/SHORT signal.

There are times where it is a good time to buy or sell, but the RSI may not be in the right place. This is rare but it does happen. We marked a location that did exactly that with an Orange circle in the picture above. These things happen, however we don’t recommend you act on them. The main reason is that they are much more risky. Nothing will ever be 100% accurate, but the key is making decisions that are more in your favor than not. When the RSI and RSI MA cross and the RSI is near 50, it's much less accurate, however, not impossible for it to be a good signal.

Now you may be wondering, how come I see 2 SELL or 2 BUY signals before the RSI moves a lot? This is quite normal. Based on the picture above, all of the BUY and SELL signals are accurate, but not all of them have insane price movements. However, they all did feature SOME price movements. Just because a BUY or SELL (RSI and RSI MA crossing) happens, doesn’t mean the RSI is going to move all the way from 80 to 20, sometimes the price only moves a bit and then corrects back. This is completely normal.

The part that is up to you is knowing when to exit these trades. You can use the YinYang RSI to see entry locations for Long/Short, but it can be risky to assume that you can go from a BUY right to a SELL and vice versa.

Don’t fret, there is a reason we have our YinYang Stoch RSI within this indicator and its not just because we felt like it! When you overlay the YinYang RSI and YinYang Stoch RSI on top of each other, you can get a very good idea of when a signal may be over and likely it’s a good time to get out. However, first, just so you understand what our YinYang Stoch RSI does, let's take a quick look at it.

At first glance, the YinYang Stoch RSI can look pretty strange and even overwhelming, this is completely normal. It features drastic movements, but only when there is good reason to! When the blue line (K) crosses the orange line (D) it represents momentum in price. So when the blue line crosses above the orange line it means BUY and when the blue line crosses below the orange line it means SELL.

How it works with the YinYang RSI is simple, lets toggle the two of them on together in the settings:

It may look a little confusing at first, and we don’t necessarily recommend you do it for your entry as it can be a little too much and sometimes confusing, but it can be very helpful for understanding your exit and if the momentum has changed/died down. Here's an example based on our initial BUY/SELL image above:

So since we’re talking about the double SELL signal and how to know if its momentum is ending we’ve zoomed in on this example. Here we can see where the pink circle is, that the YinYang Stoch RSI has gained buy momentum and the sell momentum has likely ended here. This is canceled out however, by the fact that shortly after we see another SELL signal combined with the Stoch RSI crossing under and also showing SELL momentum. The blue Vertical lines are to show visually where the stoch crossed over/under as they can be a little hard to see visually. Also, based on this example, you can see where the orange circle is that was clearly a very good buy location and also has the stoch crossover in that location too. So even though the RSI isn’t very low, there is still a decent amount of bullish momentum in that location. Is this enough for you to make a purchase on? In our opinion, it’s still a little too risky, but maybe it fits your trading style, or maybe you decide its a good time to Dollar Cost Average / purchase just a small amount.

Now, you may be wondering, as we mentioned it early, what are those Information Tables that have been sitting on the right of every example?

These Information Tables are there to display very important Time Frame data for you. Not only can you see 6 Different Time Frames, which you can customize within your Settings. You also get to see the level of RSI and RSI MA for YinYang, Regular and YinYang Stoch RSI. Being able to see this data on multiple different Time Frames without having to change the Time Frame you are on can be very helpful, especially if you’re trading on a lower Time Frame like 15 minutes. The color of the box is based on if the RSI has crossed the MA or not. When the box is Green, the RSI is greater than the MA (Bullish). When the box is Red, the RSI is less than the MA (Bearish).

This concludes our Tutorial on how to use YinYang RSI, below you will see all of our current Settings, what they all mean and how you can customize them.

Settings:

1. Show Signals:

Signals are when the RSI crosses the RSI MA (for any RSI TYPE active). When these crosses happen, it will make a plot on the chart that represents Buy and Sell Signals. These signals have alerts that correspond with them, but you will manually need to set up these alerts yourself through the indicator. Please refer to TradingView for how to set up alerts.

2. RSI Type:

We have 3 types of RSI’s within this Indicator:

YinYang RSI

Regular RSI

YinYang Stoch RSI

These RSI’s can be used individually or overlaid on top of each other for easier comparison. It can be useful to go back and forth between indicators or have them overlaid to get a better understanding of what's going on.

2.1. YinYang RSI:

Our YinYang RSI is our custom RSI that is based on our True Value Zone Algorithm. It is the main purpose of this Indicator but can be used in conjunction with Regular RSI and YinYang Stoch RSI. YinYang RSI is a much more smooth, slow moving form of RSI that doesn’t go down from consolidation and therefore makes the RSI and RSI MA crosses much more accurate.

2.2. Regular RSI:

This is a regular RSI that is within our indicator so you can make comparisons and also overlay on top of our YinYang RSI and/or YinYang Stoch.

2.3. YinYang Stoch RSI:

This is a Stoch RSI that is calculated with our YinYang RSI’s values to create a very unique Stoch RSI. Our YinYang Stoch RSI moves very drastically and quickly when there is true momentum swings but it never really hovers in the middle. It makes its way from 0-100 and 100-0 within 2-3 candles usually and if it makes it all the way, you know there is momentum backing this price movement.

3. Information Tables:

3.1. Show Information Tables:

Our Information tables display 6 different Time Frame resolutions to give you the data of YinYang RSI/MA, Regular RSI/MA and Stoch RSI/MA over multiple different Time Frames so you don’t constantly have to keep changing yours and can focus on the trade at hand.

You can choose to display:

‘All’,

‘None’,

‘YinYang RSI’,

‘Regular RSI’,

‘YinYang Stoch RSI’

and/or any combination of the three so you can see all the data you want to your liking.

3.2. Display Tables Direction:

Since there are 6 different Time Frames shown, and you have the ability to display all 3 RSI and MA values, this table can get pretty big. If you have a large monitor and not too many indicators active it's no big deal and a vertical display is likely what you’ll want. However, if you have a smaller monitor or many Indicators active, it will scrunch this Indicator and make it difficult to see all of your Time Frames in the tables. For this reason, we have the option to display them ‘Horizontally’.

3.3. Res1 / Res2/ Res3 / Res4 / Res5 / Res6:

These represent the different resolutions (Time Frames) being used in your information tables and can be modified to display whatever resolution works best for your trading style. By default they are:

Res1: Current Timeframe

Res2: 15 Minute

Res3: 1 Hour

Res4: 4 Hour

Res5: 1 Day

Res6: 1 Week

Backup Res (not changeable): 5 Minute (this is only used if your Current Timeframe in Res1 is a duplicate of one of the other resolutions)

Alerts are available and customizable within the Indicator. You can set up an alert for any of the RSI crossing Signals.

If you have any Questions or Concerns, don’t hesitate to contact us.

HAPPY TRADING!

Strategy Gaussian Anomaly DerivativeConcept behind this Strategy :

Considering a normal "buy/sell" situation, an asset would be bought in average at the median price following a Gaussian like concept. A higher or lower average trend would significate that the current perceived value is respectively higher or lower than the current median price, which mean that the buyers are evaluating the price underpriced or overpriced.

This behaviour would be even more relevent depending on its derivative evolution.

Therefore, this Strategy setup is based on this Gaussian like concept anomaly of average close positionning compare to high-low average derivative, such as the derivative of the following ploted basic signal : 1-(high+low)/(2*close).

This Strategy can actually be used like a trend change and continuation strength indicator aswell.

In the Setup Signal part :

You can define the filtering of the basis signal "1-(high+low)/(2*close)" on EMA or SMA as you wish.

You can define the corresponding period and the threathold as a mutiply of the average 1/3 of all time value of the basis signal.

You can define the SMA filtering period of the Derivative signal and the corresponding threathold on the same mutiply of the average 1/3 of all time value of the derivative.

In the Setup Strategy part :

You can set up your strategy assesment based on Long and/or Short. You can also define the considered period.

The most successful tuned strategies I did were based on the derivative indicator with periods on the basis signal and the derivative under 30, can be 1 to 3 of te derivative and 7 to 21 for the basis signal. The threathold depends on the asset volatility aswell, 1 is usually the most efficient but 0 to 10 can be relevent depending on the situation I met. You can find an example of tuning for this strategy based on Kering's case hereafter.

I hoping that you will enjoy using this Strategy, don't hesitate to comment, to question, to correct or complete it ! I would be very curious about similar famous approaches that would have already been made.

Thank to you !

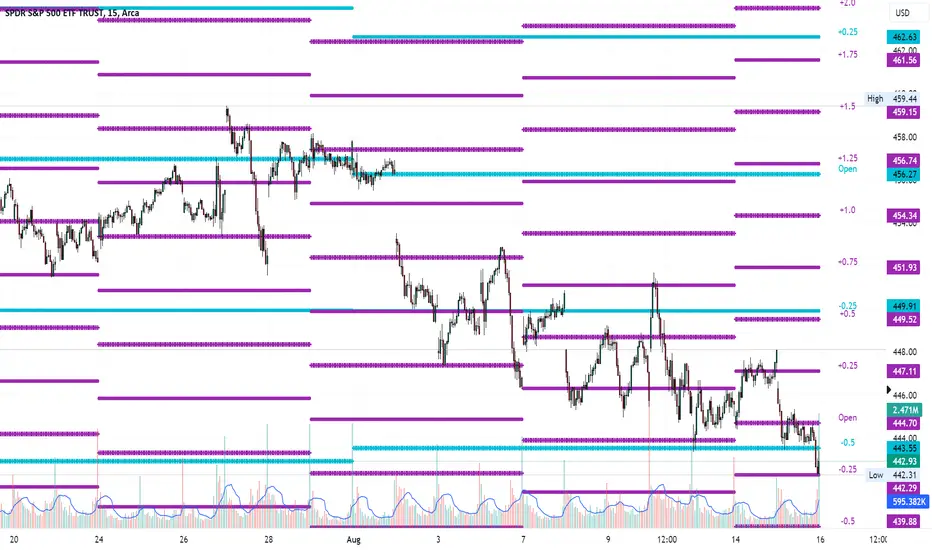

Average Range LinesThis Average Range Lines indicator identifies high and low price levels based on a chosen time period (day, week, month, etc.) and then uses a simple moving average over the length of the lookback period chosen to project support and resistance levels, otherwise referred to as average range. The calculation of these levels are slightly different than Average True Range and I have found this to be more accurate for intraday price bounces.

Lines are plotted and labeled on the chart based on the following methodology:

+3.0: 3x the average high over the chosen timeframe and lookback period.

+2.5: 2.5x the average high over the chosen timeframe and lookback period.

+2.0: 2x the average high over the chosen timeframe and lookback period.

+1.5: 1.5x the average high over the chosen timeframe and lookback period.

+1.0: The average high over the chosen timeframe and lookback period.

+0.5: One-half the average high over the chosen timeframe and lookback period.

Open: Opening price for the chosen time period.

-0.5: One-half the average low over the chosen timeframe and lookback period.

-1.0: The average low over the chosen timeframe and lookback period.

-1.5: 1.5x the average low over the chosen timeframe and lookback period.

-2.0: 2x the average low over the chosen timeframe and lookback period.

-2.5: 2.5x the average low over the chosen timeframe and lookback period.

-3.0: 3x the average low over the chosen timeframe and lookback period.

Look for price to find support or resistance at these levels for either entries or to take profit. When price crosses the +/- 2.0 or beyond, the likelihood of a reversal is very high, especially if set to weekly and monthly levels.

This indicator can be used/viewed on any timeframe. For intraday trading and viewing on a 15 minute or less timeframe, I recommend using the 4 hour, 1 day, and/or 1 week levels. For swing trading and viewing on a 30 minute or higher timeframe, I recommend using the 1 week, 1 month, or longer timeframes. I don’t believe this would be useful on a 1 hour or less timeframe, but let me know if the comments if you find otherwise.

Based on my testing, recommended lookback periods by timeframe include:

Timeframe: 4 hour; Lookback period: 60 (recommend viewing on a 5 minute or less timeframe)

Timeframe: 1 day; Lookback period: 10 (also check out 25 if your chart doesn’t show good support/resistance at 10 days lookback – I have found 25 to be useful on charts like SPX)

Timeframe: 1 week; Lookback period: 14

Timeframe: 1 month; Lookback period: 10

The line style and colors are all editable. You can apply a global coloring scheme in the event you want to add this indicator to your chart multiple times with different time frames like I do for the weekly and monthly.

I appreciate your comments/feedback on this indicator to improve. Also let me know if you find this useful, and what settings/ticker you find it works best with!

Also check out my profile for more indicators!

Average purchase price 0.1 [PATREND]

Average purchase price

This tool calculates the average purchase and sell price and the profit/loss ratio for the selected symbol based on the user's inputs for the purchase and sell prices and the entry and exit amounts.

Using Average purchase price with DCA strategy

This tool can be used to track the performance of your dollar cost averaging (DCA) investment strategy.

This tool allows you to enter information about your purchase and sell transactions, such as the purchase and sell price and the entry and exit amount, and it calculates the average purchase and sell price and the profit/loss ratio based on this information.

When using a DCA strategy, you can enter information about your regular purchase and sell transactions and the tool will calculate the average purchase and sell price for you.

You can use this information to determine if your strategy is working well and make the necessary adjustments.

In addition, this tool can help you determine when you should increase or decrease the regular investment amounts that you make as part of your DCA strategy.

It can also show you the profit/loss ratio for each sell transaction that you made.

_________________________________

We hope you find it useful.

Don't hesitate to try this tool and customize its settings to meet your trading needs.

We look forward to seeing your opinions and comments.

______________________________________________________________________________________________________

Average purchase price

هذه الأداة تحسب متوسط سعر الشراء والبيع ونسبة الربح / الخسارة للرمز المحدد بناءً على إدخالات المستخدم لأسعار الشراء والبيع ومبالغ الدخول والخروج.

استخدام Average purchase price مع استراتيجية DCA

يمكن استخدام هذه الأداة لتتبع أداء استراتيجية الاستثمار المتوسط التكلفة الدولارية (DCA) الخاصة بك.

تتيح لك هذه الأداة إدخال معلومات عن عمليات الشراء والبيع الخاصة بك، مثل سعر الشراء والبيع وكمية الدخول والخروج، ويقوم بحساب متوسط سعر الشراء والبيع ونسبة الربح / الخسارة بناءً على هذه المعلومات.

عند استخدام استراتيجية DCA، يمكنك إدخال معلومات عن عمليات الشراء والبيع المنتظمة التي تقوم بها وستقوم الأداة بحساب متوسط سعر الشراء والبيع لك. يمكنك استخدام هذه المعلومات لتحديد ما إذا كانت استراتيجيتك تعمل بشكل جيد وإجراء التعديلات اللازمة.

بالإضافة إلى ذلك

يمكن لهذه الأداة مساعدتك في تحديد متى يجب عليك زيادة أو تقليل مبالغ الاستثمار المنتظمة التي تقوم بها كجزء من استراتيجية DCA. كما يمكنها أن تظهر لك نسبة الربح / الخسارة في كل عملية بيع قمت بها.

تصرف كخبير ترجمه مختص باسواق المال وترجم هذا النص للغه الانكليزيه بشكل دقيق

_________________________________

نأمل أن تجدوه مفيدًا لكم .

لا تترددوا في تجربة هذه الأداة وتخصيص إعداداتها لتلبية احتياجاتكم التداولية.

نتطلع إلى رؤية آرائكم وتعليقاتكم .

Average True Range Trailing Mean [Alifer]Upgrade of the Average True Range default indicator by TradingView. It adds and plots a trailing mean to show periods of increased volatility more clearly.

ATR TRAILING MEAN

A trailing mean, also known as a moving average, is a statistical calculation used to smooth out data over time and identify trends or patterns in a time series.

In our indicator, it clearly shows when the ATR value spikes outside of it's average range, making it easier to identify periods of increased volatility.

Here's how the ATR Trailing Mean (atr_mean) is calculated:

atr_mean = ta.cum(atr) / (bar_index + 1) * atr_mult

The ta.cum() function calculates the cumulative sum of the ATR over all bars up to the current bar.

(bar_index + 1) represents the number of bars processed up to the current bar, including the current one.

By dividing the cumulative ATR ta.cum(atr) by (bar_index + 1) and then multiplying it by atr_mult (Multiplier), we obtain the ATR Trailing Mean value.

If atr_mult is set to 1.0, the ATR Trailing Mean will be equal to the simple average of the ATR values, and it will follow the ATR's general trend.

However, if atr_mult is increased, the ATR Trailing Mean will react more strongly to the ATR's recent changes, making it more sensitive to short-term fluctuations.

On the other hand, reducing atr_mult will make the ATR Trailing Mean less responsive to recent changes in ATR, making it smoother and less prone to reacting to short-term volatility.

In summary, adjusting the atr_mult input allows traders to fine-tune the ATR Trailing Mean's responsiveness based on their preferred level of sensitivity to recent changes in market volatility.

IMPLEMENTATION IN A STRATEGY

You can easily implement this indicator in an existing strategy, to only enter positions when the ATR is above the ATR Trailing Mean (with Multiplier-adjusted sensitivity). To do so, add the following lines of codes.

Under Inputs:

length = input.int(title="Length", defval=20, minval=1)

atr_mult = input.float(defval=1.0, step = 0.1, title = "Multiplier", tooltip = "Adjust the sensitivity of the ATR Trailing Mean line.")

smoothing = input.string(title="Smoothing", defval="RMA", options= )

ma_function(source, length) =>

switch smoothing

"RMA" => ta.rma(source, length)

"SMA" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

=> ta.wma(source, length)

This will allow you to define the Length of the ATR (lookback length over which the ATR is calculated), the Multiplier to adjust the Trailing Mean's sensitivity and the type of Smoothing to be used for the ATR.

Under Calculations:

atr= ma_function(ta.tr(true), length)

atr_mean = ta.cum(atr) / (bar_index+1) * atr_mult

This will calculate the ATR based on Length and Smoothing, and the resulting ATR Trailing Mean.

Under Entry Conditions, add the following to your existing conditions:

and atr > atr_mean

This will make it so that entries are only triggered when the ATR is above the ATR Trailing Mean (adjusted by the Multiplier value you defined earlier).

ATR - DEFINITION AND HISTORY

The Average True Range (ATR) is a technical indicator used to measure market volatility, regardless of the direction of the price. It was developed by J. Welles Wilder and introduced in his book "New Concepts in Technical Trading Systems" in 1978. ATR provides valuable insights into the degree of price movement or volatility experienced by a financial asset, such as a stock, currency pair, commodity, or cryptocurrency, over a specific period.

ATR - CALCULATION AND USAGE

The ATR calculation involves three components:

1 — True Range (TR): The True Range is a measure of the asset's price movement for a given period. It takes into account the following factors:

The difference between the high and low prices of the current period.

The absolute value of the difference between the high price of the current period and the closing price of the previous period.

The absolute value of the difference between the low price of the current period and the closing price of the previous period.

Mathematically, the True Range (TR) for the current period is calculated as follows:

TR = max(high - low, abs(high - previous_close), abs(low - previous_close))

2 — ATR Calculation: The ATR is calculated as a Moving Average (MA) of the True Range over a specified period.

The ATR is calculated as follows:

ATR = MA(TR, length)

3 — ATR Interpretation: The ATR value represents the average volatility of the asset over the chosen period. Higher ATR values indicate higher volatility, while lower ATR values suggest lower volatility.

Traders and investors can use ATR in various ways:

Setting Stop Loss and Take Profit Levels: ATR can help determine appropriate stop-loss and take-profit levels in trading strategies. A larger ATR value might require wider stop-loss levels to allow for the asset's natural price fluctuations, while a smaller ATR value might allow for tighter stop-loss levels.

Identifying Market Volatility: A sharp increase in ATR might indicate heightened market uncertainty or the potential for significant price movements. Conversely, a decreasing ATR might suggest a period of low volatility and possible consolidation.

Comparing Volatility Between Assets: Since ATR uses absolute values, it shouldn't be used to compare volatility between different assets, as assets with higher prices will consistently have higher ATR values, while assets with lower prices will consistently have lower ATR values. However, the addition of a trailing mean makes such a comparison possible. An asset whose ATR is consistently close to its ATR Trailing Mean will have a lower volatility than an asset whose ATR continuously moves far above and below its ATR Trailing Mean. This can help traders and investors decide which markets to trade based on their risk tolerance and trading strategies.

Determining Position Size: ATR can be used to adjust position sizes, taking into account the asset's volatility. Smaller position sizes might be appropriate for more volatile assets to manage risk effectively.

Volume Change Indicator 0.1 [PATREND]

(Volume Change Indicator)

It is an analytical tool that studies the trading volume and its changes.

This indicator uses the Simple Moving Average (SMA) to calculate the average volume for a specific period of time.

Only candles that meet the required conditions are determined when the trading volume is greater than or equal to the calculated average.

This means that the indicator identifies a volume candle only when there is a significant change in trading volume compared to the average.

This indicator is distinguished from other similar indicators in that it allows the user to determine the required percentage of change as an additional condition for determining the volume candle.

If the conditions are correct, the indicator will display a diamond below the candle that meets the requirements specified by the user.

The indicator also displays lines above and below the candle and places "A" and "B" marks next to them to determine the start and end points.

__________________________________

(Volume Change Indicator)

It is a useful analytical tool for traders who rely on volume analysis strategies in their trading decisions.

This indicator helps traders identify important volume candles and search for trading opportunities more accurately.

Traders can use this indicator to determine trends and search for potential entry and exit points.

The indicator helps determine when there is a significant change in trading volume compared to the average, indicating a possible change in direction.

In general

This indicator benefits traders who use volume analysis strategies in their trading decisions and who want additional information about trading volume and its changes.

It can also be used for all markets and on different time frames.

_________________________________

Settings:

1. The user is allowed to determine whether they want to display the indicator through the "Show Indicator" box.

2. The user is allowed to determine the required percentage of change through the "Percent Change" box.

3. The user is allowed to determine the type of candles they want to display (Bearish, Bullish, both) through the "Candle Type" box.

4. The user is allowed to calculate the average candle volume using the "Average Vol" box.

5. The user is allowed to determine the length of lines and number of lines they want to display through "Max Lines" and "Line Length" boxes.

_________________________________

We hope you find (Volume Change Indicator) useful in your analysis.

Feel free to try this indicator and customize its settings to meet your trading needs.

We look forward to seeing your opinions and comments on this indicator.

______________________________________________________________________________________________________

(Volume Change Indicator)

هو أداة تحليلية تعمل على دراسة حجم التداول وتغيراته.

يستخدم هذا المؤشر متوسط الحجم المتحرك (SMA) لحساب متوسط الحجم لفترة زمنية معينة.

يتم تحديد الشموع التي تلبي الشروط المطلوبة فقط عندما يكون حجم التداول أكبر من أو يساوي المتوسط المحسوب.

هذا يعني أن المؤشر يحدد شمعة الكميات فقط عندما يكون هناك تغير كبير في حجم التداول مقارنة بالمتوسط.

يتميز هذا المؤشر عن غيره من موشرات الممثاله بأنه يتيح للمستخدم تحديد النسبة المئوية المطلوبة للتغيير كشرط إضافي لتحديد شمعة الكميات.

إذا كانت الظروف صحيحة، فسيعرض المؤشر ماسًا أسفل الشمعة التي تلبي المتطلبات المحددة من قبل المستخدم.

كما يعرض المؤشر خطوطًا فوق وتحت الشمعة ويضع علامتي "A" و "B" بجانبهما لتحديد نقاط البداية والنهاية.

________________________________________

(Volume Change Indicator)

هو أداة تحليلية مفيدة للمتداولين الذين يعتمدون على استراتيجيات تحليل الحجم في قراراتهم التداولية.

يساعد هذا المؤشر المتداولين على تحديد شموع الكميات المهمة والبحث عن فرص تداولية بشكل أكثر دقة.

يمكن للمتداولين استخدام هذا المؤشر لتحديد الاتجاهات والبحث عن نقاط الإدخال والخروج المحتملة.

يساعد المؤشر على تحديد متى يكون هناك تغير كبير في حجم التداول مقارنة بالمتوسط، مما يشير إلى احتمالية حدوث تغير في الاتجاه.

In general

يستفيد من هذا المؤشر المتداولون الذين يستخدمون استراتيجيات تحليل الحجم في قراراتهم التداولية والذين يرغبون في الحصول على معلومات إضافية حول حجم التداول وتغيراته.

كما يمكن استخدامة لجميع الاسواق وعلى مختلف الفواصل الزمنية .

_________________________________________

Settings:

1. يُتيح للمستخدم تحديد ما إذا كان يرغب في عرض المؤشر من خلال خانة "Show Indicator".

2. يُتيح للمستخدم تحديد النسبة المئوية المطلوبة للتغير من خلال خانة "Percent Change".

3. يُتيح للمستخدم تحديد نوع الشموع التي يرغب في عرضها (Bearish, Bullish, both) من خلال خانة "Candle Type".

4. يُتيح للمستخدم حساب متوسط حجم الشموع باستخدام خانة "Average Vol".

5. يُتيح للمستخدم تحديد طول الخطوط وعدد الخطوط التي يرغب في عرضها من خلال خانات "Max Lines" و "Line Length".

_________________________________________

نأمل أن تجدواه مفيدًا في تحليلاتكم .

لا تترددوا في تجربة هذا المؤشر وتخصيص إعداداته لتلبية احتياجاتكم التداولية.

نتطلع إلى رؤية آرائكم وتعليقاتكم حول هذا المؤشر.

Rough AverageThe Rough Average indicator is a unique technical tool that calculates a modified average to provide insights into market conditions. It incorporates a combination of mathematical operations and existing indicators to offer traders a different perspective on price movements.

The Rough Average indicator aims to capture market dynamics through a specific calculation method. It utilizes two main components: a check for the approximate scale of the price and a profile calculation based on the Relative Strength Index (RSI) of the closing price.

Methodology:

Approximate Scale: The indicator determines the approximate scale of the price by analyzing the magnitude of the closing price. This step involves a mathematical process that identifies the power of 10 that best represents the scale. This function reduces overall lag and gives a better smoothing to the output of the calculation

Profile Calculation: The indicator calculates a profile value by summing the absolute values of the RSI of the closing price over a specified period. The RSI provides insights into the strength or weakness of price movements. The profile calculation considers a range of prices based on the determined scale.

Indicator Calculation:

The Rough Average is derived by applying the Exponential Moving Average (EMA) to the calculated profile. The EMA is a smoothing technique that emphasizes recent price data. The resulting value represents the modified average of the indicator.

Utility:

The Rough Average indicator offers traders an alternative perspective on market conditions. By utilizing a modified average calculation, it can reveal potential trends, reversals, or periods of market strength or weakness. Traders can use the Rough Average to complement their analysis and identify possible trading opportunities.

It is important to note that the effectiveness of the Rough Average indicator may vary depending on the specific market and trading strategy. It is recommended to combine its analysis with other technical indicators and conduct thorough testing before making trading decisions.

Key Features:

Customizable OB\OS Levels

Bar coloring methods: Trend, Reversions, Extremities

Example Charts:

TimeLy Moving Average - TMAHello traders, I'm Only Fibonacci.

With this indicator, you will see the averages according to the hourly, weekly and monthly price movements in many periods on the chart.

This will show you the moving average values of the price over different periods in a progressive manner on the chart that is open to you.

Options and Usage

To see the hourly average, your chart's time range must be less than or equal to 60 minutes, otherwise it will produce a NaN value.

In order to see the daily average, your chart must be open for any minute period or (even if the second is open, it must be greater than 6 seconds). Otherwise, it does not produce any value.

Your chart must be larger than the second chart to see the weekly average. In other words, you can see the weekly average with at least 1 minute chart open.

In order to see the monthly average, your chart time interval must be above 10 minutes, otherwise you will not be able to see data again.

Settings

You choose the moving average type and the time interval value you want to see from the indicator settings.

You can also select a source for moving averages.

Enjoy it, you can make improvements on it.

Please do not forget to comment for various bug reports.

Anchored VWAP+This indicator is an enhanced version of the Anchored VWAP indicator with additional functions:

1. Anchored AP (average price). It removes the volume weighting step in Anchored VWAP, and can display the average price over a period of time. For example, if the price of the stock in the last 3 days is 100, 200, 300, then AP is their average value of 200

2. Anchored AC (average cost). The average cost over time can be displayed. For example, if the price of the stock in the last 2 days is 100,300, then AC is (1+1)/(1/100+1/300)=150

When using the indicator, you need to choose a starting point, then the indicator will start to calculate the subsequent VWAP, AP and AC from this starting point, and draw 3 lines in the graph

These three lines can be regarded as the average cost line of the market, with potential support and resistance effects

We have filled the shadow between VWAP and AP, which can be regarded as a potential support resistance band

===========================中文版本===========================

该指标为增强版本的Anchored VWAP指标。在Anchored VWAP基础上增加了额外功能:

1. Anchored AP。其去掉了Anchored VWAP中成交量加权的步骤,可以显示一段时间的平均价格。举个例子,假如股票最近3天的价格为100,200,300,那么AP为他们的平均值200

2. Anchored AC。可以显示一段时间的平均成本。举个例子,假如股票最近2天的价格为100,300,那么AC为(1+1)/(1/100+1/300)=150

使用指标时你需要先选择一个起点,随后指标将会以该起点开始计算后续的VWAP、AP和AC,并且在图中绘制3根线

这3根线均可以视作是市场的平均成本线,具有潜在的支撑和阻力效果

我们让VWAP和AP之间填充了阴影,该阴影可以视作潜在的支撑阻力带

Ratio To Average - The Quant ScienceRatio To Average - The Quant Science is a quantitative indicator that calculates the percentage ratio of the market price in relation to a reference average. The indicator allows the calculation of the ratio using four different types of averages: SMA, EMA, WMA, and HMA. The ratio is represented by a series of histograms that highlight periods when the ratio is positive (in green) and periods when the ratio is negative (in red).

What is the Ratio to Average?

The Ratio to Average is a measure that tracks the price movements with one of its averages, calculating how much the price is above or below its own average, in percentage terms.

USER INTERFACE

Lenght: it adjusts the number of bars to include in the calculation of the average.

Moving Average: it allows you to choose the type of average to use.

Color Up/Color Down : it allows you to choose the color of the indicator for positive and negative ratios.

MADI(Moving average deviation rate index)This script is "Moving average deviation rate" to Indexing.

index = average deviation rate / (Sigma * (input:SIgma)) * 100

It's for people who like simplicity.

Broadview Dominance SuiteIntroducing the revolutionary Broadview Dominance Suite, a culmination of scientific precision and astute mathematical finance, designed to provide traders with unparalleled insights into market dynamics and the balance of power. This suite leverages a comprehensive set of seven distinct moving averages, including the Simple Moving Average (SMA), Exponential Moving Average (EMA), Hull Moving Average (HMA), Weighted Moving Average (WMA), Volume Weighted Moving Average (VWMA), Triple Exponential Moving Average (TEMA), and Least Squares Moving Average (LSMA). Through the combination of these moving averages, the Broadview Dominance Suite offers traders an authoritative perspective on the control exerted by market participants over a given period.

At the heart of the Broadview Dominance Suite lies the concept of the balance of power, a pivotal determinant of market dynamics. The balance of power refers to the tug-of-war between buyers (bulls) and sellers (bears) within the market. By analyzing the relationship between the market participants, the suite allows traders to identify and comprehend who holds control over a specific timeframe.

The seven different types of moving averages employed in the Broadview Dominance Suite contribute to an in-depth assessment of market dominance. Each moving average possesses unique characteristics that facilitate a comprehensive evaluation of the balance of power. Let's delve into the moving averages included in this suite and their respective properties:

Simple Moving Average (SMA): The SMA, known for its simplicity, calculates the average price over a specified period. When applied to the balance of power, the SMA provides a smoothed line that highlights overall price trends. Its straightforward nature allows for a clear interpretation of the dominant market forces.

Exponential Moving Average (EMA): The EMA assigns more weight to recent prices, making it highly responsive to short-term price movements. By incorporating the EMA into the balance of power analysis, traders can identify potential trend reversals and shifts in market control with increased accuracy.

Hull Moving Average (HMA): The HMA employs weighted moving averages and a square root function to reduce lag and noise. This results in a smoother line that closely aligns with current price action. When assessing the balance of power, the HMA enables traders to discern precise trend indications, minimizing false signals and providing a clearer understanding of market dominance.

Weighted Moving Average (WMA): The WMA assigns varying weights to different price points within the selected period, placing greater emphasis on recent data. This feature allows the WMA to be more sensitive to recent price changes. When utilized in the analysis of the balance of power, the WMA excels at detecting short-term shifts in market control and identifying periods of heightened buying or selling pressure.

Volume Weighted Moving Average (VWMA): The VWMA incorporates trading volume into its calculation, highlighting the importance of volume in determining market dynamics. By integrating volume data, the VWMA offers a more comprehensive understanding of price levels where significant buying or selling activity occurs. In the context of the balance of power, the VWMA provides valuable insights into the intensity of market control exerted by the bulls or bears.

Triple Exponential Moving Average (TEMA): The TEMA employs multiple exponential smoothing techniques to reduce lag and enhance responsiveness. It excels at capturing short-term price movements and potential trend reversals. By incorporating the TEMA into the analysis of the balance of power, traders can gain a deeper understanding of swift shifts in market control, allowing for timely decision-making.

Least Squares Moving Average (LSMA): The LSMA minimizes the sum of squared differences between the moving average and the actual price, resulting in a curve that closely fits the price data. When applied to the balance of power, the LSMA provides a smooth line that effectively captures significant price trends. Its ability to filter out noise ensures a clearer representation of dominant market forces.

By combining these seven moving averages within the Broadview Dominance Suite, traders gain an authoritative assessment of market control. The interplay between these moving averages presents a nuanced and multi-faceted perspective on the balance of power. When a line falls below the center line, it signifies the market is under the control of the bears, indicating a dominance of selling pressure. Conversely, when the lines rise above the center line, it suggests the market is controlled by the bulls, with buying pressure prevailing.

Average Trend with Deviation Bands v2TL;DR: An average based trend incl. micro trend spotting and multiple display options.

This script is basically an update of my "Average Trend with Deviation Bands" script. I made the following changes:

Not an overlay anymore - The amount of drawn lines makes the chart pretty messy. That's why I moved it to a pane. If you preferred the overlay you can use my "Average Trend with Deviation Bands" script. *This is also the reason why I publish this script instead of updating the existing one.

I added an EMA to represent the price movement instead of candles

I added a signal (SMA) to spot micro trends and early entry/exit signals

I added the option to switch between a "line view" which shows the average trend and deviation bands and an "oscillator view" which shows an oscillator and histogram (MACD style)

General usage:

1. The white line is the average trend (which is an average of the last N bars open, close, high, low price).

2. Bands around the average trend are standard deviations which can be adjusted in the options menu and are only visible in "lines view". Basically they are like the clouds in the Ichimoku Cloud indicator - In big deviation bands the price movement needs more "power" to break through the average trend and vice versa.

3. Indicator line (blue line) - This is the EMA which represents the price. Crossing the average trend from below indicates an uptrend and vice versa (crossing from above indicates a down trend).

4. Signal line (red line) - This is a smoothed version of the indicator line which can be used to predict the movement of the price when crossed by the indicator line (like at MACD and many other indicators).

Oscillator usage:

When switched to "oscillator view" the indicator line oscillates around a zero line which can be seen as the average trend. The usage is basically the same as described above. However there is also the histogram which shows the difference between the indicator and signal. Of course the histogram can be deactivated. Additionally a color filling can be added to easily spot entry/exit signals.

As always: Code is free do whatever you like. If you have any questions/comments/etc. just drop it in the comment section.

Manual PnL (Profit and Loss) % Tracker - spot long only

This is a manual profit and loss tracker. It takes the user's manual input of total cost and quantity, and then outputs a table on the bottom right of the chart showing the profit or loss %, average purchase price, gross profit or loss, and market value.

Instructions:

1. Double click the indicator title at the top left of the chart

2. Select the "Inputs" tab and click the empty field next to "Symbol" to enter the traded symbol+exchange. This entry MUST be the same as the chart you are on, for example BTCUSDT/BINANCE (indicator will not display otherwise)

3. Enter the Total Cost and Qty of shares/coins owned

4. Optional - change positive or negative colors

5. Optional - under the "Style" tab, change the color of the average price (AVG) line

Note that for the average price (AVG) line to be shown/hidden you must enable/disable "Indicator and financials labels" in the scales settings.

For crypto or other tickers that have prices in many decimal places I would suggest, for the sake of accuracy, adjusting the decimal places in the code so that for prices under $1 you will display more info.

For example let's say you purchase x number of crypto at a price of 0.031558 you should change the code displaying "0.00" on line 44 to "0.000000"

This will ensure that the output table and plotted line will calculate an average price with the same number of decimals.