Put Option Profits inspired by Travis Wilkerson; SPX BacktesterPut Option Profits — Travis Wilkerson inspired. This tester evaluates a simple monthly SPX at-the-money credit-spread timing idea: enter on a fixed calendar rule (e.g., 1st Friday or 8th day with business-day shifting) at Open or Close, then exit exactly N calendar days later (first tradable day >= target, at Close). A trade is marked WIN if price at exit is above the entry price (1:1 risk proxy).

The book suggests forward testing 60-day and 180-day expirations to prove the concept. This tool lets you backtest both (and more) to see what actually works best. In the book, profits are taken when the spread reaches ~80% of max credit; losers are left to expire and cash-settle. This backtester does not model early profit-taking—every trade is held to the configured hold period and evaluated on price vs entry at the exit close. Think of it as a pure “set it and forget it” stress test. In live trading, you can still follow Travis’s 80% take-profit rule; TradingView just doesn’t simulate that here. Happy trading!

Features:

Schedule: Day-of-Month (with Prev/Next business-day shift, optional “stay in month”) or Nth Weekday (e.g., 1st Friday).

Entry timing: Open or Close.

Exit: N calendar days later at Close (holiday/weekend aware).

Filters: Optional EMA-200 “risk-on” filter.

Scope: Date range limiter.

Visuals: Entry/exit bubbles (paired colors) or simple win/loss dots.

Table: Overall Win% and N (within range).

Alerts: Entry alert (static condition + dynamic alert() message).

How to use:

[* ]Choose Start Mode (NthWeekday or DayOfMonth) and parameters (e.g., 1st Friday or DOM=8, PrevBizDay).

Pick Entry Timing (Open or Close).

Set Days In Trade (e.g., 150).

(Optional) Enable EMA filter and set Date Range.

Turn Bubbles on/off and/or Dots on/off.

Create alert:

Simple ping: Condition = this indicator -> Monthly Entry Signal -> “Once per bar” (Open) or “Once per bar close” (Close).

Rich message: Condition = this indicator -> Any alert() function call.

Notes:

Keep DOM shift in same month: when a DOM falls on a weekend/holiday, PrevBizDay/NextBizDay shift will stay inside the month if enabled; otherwise it can spill into the prior/next month. (Ignored for NthWeekday.)

Credits: Concept sparked by “Put Option Profits – How to turn ten minutes of free time into consistent cash flow each month” by Travis Wilkerson; this script is a neutral research tool (not financial advice).

Statistics

Slick Strategy Weekly PCS TesterInspired by the book “The Slick Strategy: A Unique Profitable Options Trading Method.” This indicator tests weekly SPX put-credit spreads set below Monday’s open and judged at Friday’s close.

WHAT IT DOES

• Sets weekly PCS level = Monday (or first trading day) OPEN − your offset; win/loss checked at Friday close.

• Optional core filter at entry: Price ≥ 200-SMA AND 10-SMA ≥ 20-SMA; pause if Price < both 10 & 20 while > 200.

• Reference modes: Strict = Mon OPEN vs Fri SMAs (no repaint); Mid = Mon OPEN vs Mon SMAs

KEY INPUTS

• Date range (Start/End) to limit backtest window.

• Offset mode/value (Points or Percent).

• Entry day (Monday only or first trading day).

• Core filters (On/Off) and Strict/Mid reference.

• SMA settings (source; 10/20/200 lengths).

• Table settings (position, size, padding, border).

VISUALS

• Active week line: Orange = trade taken; Gray = skipped.

• History: Green = win; Red = loss; Purple = skipped.

• Optional week bands highlight active/win/loss/skipped weeks (adjustable opacity).

TABLE

• Shows Date range, Trades, Wins, Losses, Win rate, and Active level (this week’s PCS price).

NOTES

• PCS level freezes at week open and persists through the week.

MarketCap + BVPSMarketCap + BVPS

Fundamental Summary Table Version 1 is currently being tested on the Israeli market and some stocks from the American market

Releasing a version after the data has been tested

And there is also interesting information that emerges from this indicator

עברית

טבלת סיכום פונדמנטלי גרסה 1 כרגע בדוקה על השוק הישראלי ועל כמה מניות מהשוק האמריקאי

משחרר גרסה לאחר שהנתונים נבדקו

וגם יש מידע מעניין שעולה מן האינדיקטור הזה! (מוזמנים לבדוק)

High/Low from Set Period with LabelsMark high and low from a set period.

I use it to mark Overnight Low and High of FDAX instrument, to achieve that :

- you need to use candle chart

- you need to use regular trading hours ( to include overnight trades )

- you need to set that on M2 timeframe

- you need to set time begin : 17:30

- you need to set time end : 08:58

- when it will be drawn in 09:02, then let extend it via a hand and then you can disable

Issues :

- it will be visible after finished miminum period time :

-- after 2 minutes on M2 ( 9:02 )

-- after 5 minutes on M5 ( 9:05 )

etc ...

DAX Sectors OverviewIt's a table with a realtime read of DAX sectors, their changes in the day, weight for the whole DAX index.

Weights are fixed values defined in the script - recommended to refresh them periodically.

Dublin Time Hourly Levels for Natural Gas Prints lines from 2:30am too 8:30am UTC 00:00 and shows the odds of those levels being hit between 10:30am - 13:30am based on previous sessions. going too larger time frames gathers data from more and more sessions. This can be very helpful paired with a basic entry strat eg support and resistance, volume profile etc NYMEX:NG1! is what I found has great levels but you could test on other futures, forex, crypto etc.

NQ 55 LEVELSlevels to top and bottom tick

These levels top and bottom tick a lot of the times, use your own confluences to make them work

PE Fair ValueIn short, it’s an automated fair value estimator based on the price-to-earnings model, with full manual control if TradingView’s fundamental data is missing.

Summary:

1. Lets the user choose the EPS source – either automatically from TradingView fundamentals (EPS TTM) or a manual value.

2. Attempts to fetch the stock’s P/E ratio (TTM) automatically; if unavailable, it uses a manual fallback P/E.

3. Calculates:

Actual P/E = current price ÷ EPS

Fair Value = EPS × chosen (auto/manual) P/E

Percentage difference between market price and fair value

4. Plots the fair-value line on the chart for visual comparison.

5. Displays a table in the top-right corner showing:

EPS used

Target P/E

Actual P/E

Fair value

Current price

Difference vs fair value (colored green or red)

6. Creates alerts when the stock is trading above or below the calculated fair value.

7. Also plots the current closing price for reference.

Adaptive ATR Guardian PRO+ (Locked Lines)🎯 核心交易功能 / Core Trading Features

1. 智能参数配置系统 / Intelligent Parameter Configuration

多风格选择:稳健/激进/保守三种交易风格

Multi-style Selection: Conservative/Aggressive/Moderate trading styles

多时间周期:M5/M15/H1三种时间框架

Multi-timeframe: M5/M15/H1 timeframes

自适应参数:根据风格自动调整所有技术参数

Adaptive Parameters: Automatically adjusts all technical parameters based on style

2. 高级信号生成系统 / Advanced Signal Generation

双均线策略:快慢EMA交叉信号

Dual MA Strategy: Fast/Slow EMA crossover signals

趋势过滤:100周期EMA作为趋势方向过滤

Trend Filter: 100-period EMA for trend direction filtering

ADX强度确认:ADX > 最小值才确认趋势有效

ADX Strength Confirmation: ADX > minimum value for valid trend

交易时段控制:可设置交易开始和结束时间

Trading Session Control: Configurable start and end times

3. 智能风险管理 / Intelligent Risk Management

动态止损:基于ATR的智能止损计算

Dynamic Stop Loss: ATR-based intelligent stop loss calculation

分批止盈:TP1平仓50%,TP2平仓剩余50%

Partial Take Profit: TP1 closes 50%, TP2 closes remaining 50%

追踪止损:TP2部分启用追踪止损功能

Trailing Stop: TP2 portion uses trailing stop functionality

品种自适应:BTC和黄金品种特殊参数调整

Symbol Adaptation: Special parameter adjustments for BTC and Gold

4. 专业订单管理 / Professional Order Management

自动平仓:新信号自动平掉反向仓位

Auto Close: New signals automatically close opposite positions

仓位管理:基于账户权益的百分比仓位

Position Management: Percentage-based position sizing

佣金计算:包含交易佣金成本

Commission Calculation: Includes trading commission costs

📊 高级可视化功能 / Advanced Visualization Features

1. 实时交易线系统 / Real-time Trading Lines System

入场线:蓝色虚线,显示入场价格

Entry Line: Blue dashed line showing entry price

止损线:红色实线,显示止损价格

Stop Loss Line: Red solid line showing stop loss price

TP1线:青色实线,显示第一目标位

TP1 Line: Teal solid line showing first target

TP2线:青色实线,显示第二目标位

TP2 Line: Teal solid line showing second target

2. 智能标签管理 / Intelligent Label Management

动态字号:根据时间周期自动调整标签大小

Dynamic Font Size: Auto-adjusts label size based on timeframe

位置优化:标签固定在入场K线右侧3根位置

Position Optimization: Labels fixed 3 bars right of entry candle

实时更新:线条和标签随图表滚动延伸

Real-time Updates: Lines and labels extend with chart scrolling

3. 专业信息面板 / Professional Information Panel

策略状态:交易风格、时间周期、持仓方向

Strategy Status: Trading style, timeframe, position direction

指标数据:ADX强度、ATR波动率数值

Indicator Data: ADX strength, ATR volatility values

交易信息:入场价格、止损价格、止盈价格

Trade Information: Entry price, stop loss, take profit prices

实时更新:每根K线更新最新数据

Real-time Updates: Updates data on every candle

4. 模式状态标签 / Mode Status Label

顶部状态栏:显示周期、风格、ADX、ATR、持仓状态

Top Status Bar: Shows timeframe, style, ADX, ATR, position status

颜色编码:蓝色主题,专业视觉效果

Color Coding: Blue theme, professional visual appearance

⚙️ 技术特色功能 / Technical Special Features

1. 自适应波动率调整 / Adaptive Volatility Adjustment

ATR基准:基于14周期ATR计算

ATR Baseline: Based on 14-period ATR calculation

波动率调整:ATR相对于50周期均线的调整系数

Volatility Adjustment: ATR adjustment coefficient relative to 50-period MA

动态止盈:止盈距离根据波动率动态调整

Dynamic Take Profit: TP distances dynamically adjusted based on volatility

2. 多品种优化 / Multi-Symbol Optimization

BTC特殊处理:更大的止损倍数和TP2倍数

BTC Special Handling: Larger stop loss and TP2 multipliers

黄金特殊处理:适中的参数调整

Gold Special Handling: Moderate parameter adjustments

通用品种:标准参数适用于其他品种

General Symbols: Standard parameters for other symbols

3. 时间智能控制 / Intelligent Time Control

交易时段:可配置的交易时间窗口

Trading Sessions: Configurable trading time windows

时段逻辑:支持跨午夜的时间段设置

Session Logic: Supports cross-midnight time periods

时间过滤:只在交易时段内产生信号

Time Filtering: Only generates signals during trading hours

4. 内存管理优化 / Memory Management Optimization

自动清理:平仓时自动删除所有线条和标签

Auto Cleanup: Automatically deletes all lines and labels on position close

资源回收:避免图表元素堆积

Resource Recycling: Prevents chart element accumulation

性能优化:高效的实时更新机制

Performance Optimization: Efficient real-time update mechanism

🛡️ 风险控制功能 / Risk Control Features

1. 多层过滤系统 / Multi-layer Filtering System

趋势方向过滤 / Trend direction filtering

ADX强度过滤 / ADX strength filtering

交易时间过滤 / Trading time filtering

品种特性过滤 / Symbol characteristic filtering

2. 动态参数系统 / Dynamic Parameter System

快慢均线周期自适应 / Fast/slow MA period adaptation

止损倍数动态调整 / Stop loss multiplier dynamic adjustment

止盈倍数风格化配置 / Take profit multiplier style-based configuration

追踪止损灵敏度设置 / Trailing stop sensitivity settings

3. 资金管理 / Money Management

固定百分比仓位 / Fixed percentage position sizing

佣金成本计入 / Commission costs included

无金字塔加仓 / No pyramiding (no adding to positions)

自动反向平仓 / Automatic opposite position closing

📈 用户体验功能 / User Experience Features

1. 可视化定制 / Visualization Customization

交易线显示/隐藏开关 / Trading lines show/hide toggle

信息面板显示控制 / Information panel display control

线条延伸长度可调 / Line extension length adjustable

颜色方案统一管理 / Color scheme unified management

2. 实时监控 / Real-time Monitoring

持仓状态实时显示 / Real-time position status display

关键价格水平标记 / Key price level markings

指标数值动态更新 / Indicator values dynamic updates

交易统计信息 / Trading statistics information

3. 专业布局 / Professional Layout

右上角信息面板 / Top-right information panel

顶部状态标签 / Top status label

图表交易线条 / Chart trading lines

整洁的视觉层次 / Clean visual hierarchy

Top Finder & Dip Hunter [BackQuant]Top Finder & Dip Hunter

A practical tool to map where price is statistically most likely to exhaust or mean-revert. It builds objective support for dips and resistance for tops from multiple methodologies, then filters raw touches with volume, momentum, trend, and price-action context to surface higher-quality reversal opportunities.

What this does

Draws a Dip Support line and a Top Resistance line using the method you select, or a blended hybrid.

Evaluates each touch/penetration against Quality Filters and assigns a 0–100 composite score.

Prints clean DIP and TOP signals only when depth/extension and quality pass your thresholds.

Optionally annotates the chart with the computed quality score at signal time.

Why it’s useful

Objectivity: Converts vague “looks extended” into rules, reduces discretion creep.

Signal hygiene: Filters raw touches using trend, volume, momentum, and candle structure to avoid obvious traps.

Adaptable regimes: Switch methods, sensitivity, and lookbacks to match choppy vs trending conditions.

How support and resistance are built

Pick one per side, or use “Hybrid.”

Dynamic: Anchors to the extreme of a lookback window, padded by recent ATR, so buffers expand in volatile periods and contract when calm.

Fibonacci: Uses the 0.618/0.786 retracement pair inside the current swing window to target common reaction zones.

Volatility: Uses a moving-average basis with standard-deviation bands to capture statistically stretched moves.

Volume-Weighted: Centers off VWAP and penalizes deviations using dispersion of price around VWAP, helpful on intraday instruments.

Hybrid: A weighted average of the above to smooth out single-method biases.

When a touch becomes a signal

Depth/extension test:

Dips must penetrate their support by at least Min Dip Depth % .

Tops must extend above resistance by at least Min Top Rise % .

Quality Score gate: The composite must clear Min Quality Score . Components:

Trend alignment: Favor dips in bullish regimes and tops in bearish regimes using EMAs and RSI.

Volume confirmation: Reward expansion or spikes versus a 20-period baseline.

RSI context: Prefer oversold for dips, overbought for tops.

Momentum shift: Look for short-term momentum turning in the expected direction.

Candle structure: Reward hammer/shooting-star style responses at the level.

How to use it

Pick your regime:

Range/chop, small caps, mean-revert intraday → Volatility or Volume Weighted .

Cleaner swings/trends → Dynamic or Fibonacci .

Unsure or mixed conditions → Hybrid .

Set windows: Start with Lookback = 50 for both sides. Increase in higher timeframes or slow assets, decrease for fast scalps.

Tune sensitivity: Raise Dip/Top Sensitivity to widen buffers and reduce noise. Lower to be more aggressive.

Gate with quality: Begin with Min Quality Score = 60 . Push to 70–80 for cleaner swing entries, relax to 50–60 for scalps.

Act on first prints: The script only fires on new qualified events. Use the score label to prioritize A-setups.

Typical workflows

Intraday futures/crypto: Volume-Weighted or Volatility methods for both sides, higher Sensitivity , require Volume Filter and Momentum Filter on. Look for DIP during opening drive exhaustion and TOP near late-session fatigue.

Swing equities/FX: Dynamic or Fibonacci with moderate sensitivity. Keep Trend Filter on to only take dips above the 200-EMA and tops below it.

Countertrend scouts: Lower Min Dip Depth % / Min Top Rise % slightly, but raise Min Quality Score to compensate.

Reading the chart

Lines: “Dip Support” and “Top Resistance” are the current actionable rails, lightly smoothed to reduce flicker.

Signals: “DIP” prints below bars when a qualified dip appears, “TOP” prints above for qualified tops.

Scores: Optional labels show the composite at signal time. Favor higher numbers, especially when aligned with higher-timeframe trend.

Background hints: Light highlights mark raw touches meeting depth/extension, even if they fail quality. Treat these as early warnings.

Tuning tips

If you get too many false DIP signals in downtrends, raise Min Dip Depth % and keep Trend Filter on.

If tops appear late in squeezes, lower Top Sensitivity slightly or switch top side to Fibonacci .

On assets with erratic volume, prefer Volatility or Dynamic methods and down-weight the Volume Filter .

For strict systems, increase Min Quality Score and require both Volume and Momentum filters.

What this is not

It is not a blind reversal signal. It’s a structured context tool. Combine with your risk plan and higher-timeframe map.

It is not a guarantee of mean reversion. In strong trends, expect fewer, higher-score opportunities and respect invalidation quickly.

Suggested presets

Scalp preset: Lookback 30–40, Sensitivity 1.2–1.5, Quality ≥ 55, Volume & Momentum filters ON.

Swing preset: Lookback 75–100, Sensitivity 1.0–1.2, Quality ≥ 70, Trend & Volume filters ON.

Chop preset: Volatility/Volume-Weighted methods, Quality ≥ 60, Momentum filter ON, RSI emphasis.

Input quick reference

Dip/Top Method: Choose the model for each side or “Hybrid” to blend.

Lookback: Swing window the levels are built from.

Sensitivity: Scales volatility padding around levels.

Min Dip Depth % / Min Top Rise %: Minimum breach/extension to qualify.

Quality Filters: Trend, Volume, Momentum toggles, plus Min Quality Score gate.

Visuals: Colors and whether to print score labels.

Best practices

Map higher-timeframe trend first, then act on lower-timeframe DIP/TOP in the trend’s favor.

Use the score as triage. Skip mediocre prints into news or at session open unless score is exceptional.

Pre-define stop placement relative to the level you used. If a DIP fails, exit on loss of structure rather than waiting for the next print.

Bottom line: Top Finder & Dip Hunter codifies where reversals are most defensible and only flags the ones with supportive context. Tune the method and filters to your market, then let the score keep your playbook disciplined.

Dance With Wolves VN PublicDance With Wolves VN

Indicator kết hợp EMA 9/21 để vào lệnh nhanh, thêm EMA 20/50/200 để xem trend lớn.

Tự tạo Entry, SL, TP1, TP2, TP3 theo ATR.

Vẽ luôn 3 mức kháng cự (R1–R3) và 3 mức hỗ trợ (S1–S3) từ pivot gần nhất.

Dùng tốt cho khung 1m–15m với crypto, stock, futures.

Dance With Wolves VN — Smart EMA Strategy

This indicator combines EMA 20/50/200 trend tracking, automatic Buy/Sell signals, Take Profit & Stop Loss levels, and Support/Resistance zones.

It helps traders identify clean entries, manage risk with visual TP/SL targets, and follow market trends with clarity.

Created by Dance With Wolves VN — a community project for traders who value discipline, teamwork, and precision.

Anchored ATH Drawdown LevelsThe Anchored ATH Drawdown Levels plots horizontal lines from a chosen anchor price (ATH), showing potential pullback zones at set percentage drops below it.

This indicator's use lies in its anchored ATH framework, which rapidly visualizes precise drawdown levels as dynamic levels of interest or price targets enabling traders to anticipate pullback depths and potential reversal levels without manual calculations.

Pick "True ATH" for the all-time high or "Period ATH" for anchored highs reset weekly, monthly, or quarterly. Lines stretch right for a cleaner visual.

Key Features

Anchoring: True ATH (lifetime max) or Period ATH (resets on 1W/1M/3M intervals).

Drawdown Levels: 8 adjustable levels (defaults: -5%, -10%, -15%, -20% on; -25% to -50% off). Toggle each, set drop % (0.1-99.9), pick color, style (solid/dashed/dotted), width (1-3).

ATH Line: Optional ATH line with custom color, style, width.

Unified Look: Global overrides for all levels' color, style, width.

Labels: Show % drops (with/without prices) via text boxes or full tags; sizes from tiny to large.

Projection: Lines extend 5-100 bars right (default 20).

Settings

Anchor: Mode and timeframe.

Display: Toggle levels/ATH, set extension.

Labels: Style (text/full/none), size, price display.

Global/ATH/Levels: Colors, styles, widths (per-level or shared).

How to Use

Load on chart (overlays prices; handles up to 500 lines).

Choose anchor for your high.

Tune levels for key pullbacks (e.g., -5% minor, -20% major).

Customize visuals where the lines update on new peaks.

AudenFX Futures Risk Management & CalculatorAudenFX Futures Risk Management (FRM) is a specialized utility indicator designed to help Futures traders calculate position size, risk exposure, and reward potential in a structured and consistent manner.

Unlike signal or entry indicators, this tool focuses entirely on capital protection and risk allocation, supporting traders in making more deliberate and well-planned decisions.

This indicator is particularly made for Micro and Mini Futures markets, where tick values vary across instruments, and miscalculation of position size can significantly affect overall account performance. FRM removes guesswork by using accurate, contract-specific tick values built directly into the calculation.

What Makes This Indicator Different

Most position sizing or risk calculators available publicly:

Are designed mainly for Forex / Pips, not Tick-valued Futures

Require manual tick value input, which can lead to calculation errors

Do not account for the difference between theoretical vs. executable contract sizing

Or only display formulas, instead of practical contract size output

AudenFX FRM addresses these limitations by:

Automatically applying correct tick value for each supported Futures contract

Using Stop Loss in ticks, matching actual Futures market structure

Providing rounded contract size that can be realistically executed (no decimals)

Showing both expected and actual risk after rounding, for transparency

Presenting data in a clear, on-chart table without cluttering price action

This helps minimize position size error and ensures risk is intentional, not accidental.

Key Features

Contract Support Works with Micro and Mini Futures contracts such as: MES, MNQ, MGC, SIL, MYM, ES, NQ, GC, SI, YM, RTY, M2K

Risk-Based Position Sizing Calculates trade size based on % of account equity or user-defined risk tolerance

Tick-Based SL Input Accepts Stop Loss in ticks, consistent with Futures charting and DOM placement

Accurate Tick Value Mapping Built-in tick value per contract — no manual lookup or conversion required

Contract Size Output Returns rounded number of contracts suitable for actual order execution

Actual Risk Transparency Displays the real dollar risk after rounding, preventing under/over exposure

Reward Estimation Calculates potential reward based on chosen Reward:Risk ratio (RR)

Customizable Table Display Adjustable position & size to match any chart layout preference

Intended Use

This indicator is suitable for:

Traders who prioritize risk management and capital preservation

Traders refining sizing consistency across volatile market environments

Manual, discretionary, price action, or system-based Futures traders

This tool does not generate buy/sell signals, define market direction, or promise trade outcomes.

It is meant to support a planned, methodical approach to risk, which can be applied in any strategy.

Important Disclaimer

This indicator is provided for educational and informational purposes only.

It does not guarantee profitability, prevent loss, or provide trading instructions or recommendations.

Users are fully responsible for their own trading decisions and financial outcomes.

Jackpot_By_Rao_Gs_Swng_Pbls🎯 Description

Jackpot_By_Rao_Gs_Swng_Pbls is a precision-based intraday and swing trading automation tool designed for NIFTY options, built to identify high-probability BUY CE and BUY PE opportunities.

The script automatically tracks ITM (In-the-Money) option pairs derived from the live NIFTY spot price and calculates breakout/breakdown setups based on recent swing highs and lows, EMA alignment, and RSI confirmation.

Once a valid breakout condition is met, the script generates:

Visual chart signals with complete trade details (Entry, Stop Loss, Targets)

Dynamic JSON alerts for webhook-based auto order placement

Automated trade management (Target, SL, and Exit logic)

It’s optimized for traders using Dhan API or compatible webhook integrations, enabling one-click or automated trade execution directly from TradingView alerts.

⚙️ Core Features

✅ Auto-calculates current ATM and ITM strike codes based on today’s open price

✅ Identifies breakout/breakdown trades from the previous swing levels

✅ Dynamic EMA-based trend filter (EMA 20 vs EMA 50)

✅ RSI check for directional strength (internally calculated)

✅ Full trade details shown on the chart with 5 target levels

✅ Auto JSON alert generation with webhook-ready payload

✅ Built-in Stop Loss and Exit handling logic

✅ Visual markers for CE (Green arrows) and PE (Red arrows)

✅ Adjustable parameters for expiry date, open price, and swing length

📈 Trade Logic Overview

🔹 BUY CE Condition (Bullish Setup):

EMA20 > EMA50 → Bullish trend confirmation

Spot closes below recent swing low

CE Option price below its recent high

Confirmation candle closes above previous open (if green) or above midpoint (if red)

🔹 BUY PE Condition (Bearish Setup):

EMA50 > EMA20 → Bearish trend confirmation

Spot closes above recent swing high

PE Option price below its recent high

Confirmation candle closes below previous close/midpoint depending on color

Each signal automatically plots a BUY label on the chart showing:

Entry Price

Stop Loss

Targets 1–5

Strike Code

Trigger Time |

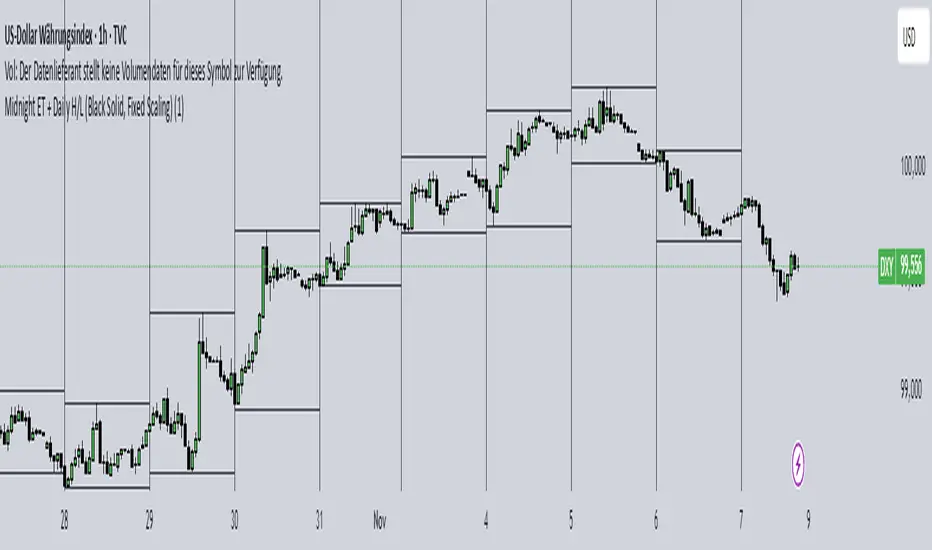

Midnight ET + Daily H/L True dayThis script divides each day from midnight EST to the next midnight opening price (True day). Full credits go to my mentor ICT for the idea behind the script

Midnight ET + Daily H/L (vertical midnight + HL lines)This script provides midnight EST dividers for each day and marks each daily high and low during each True day. Credits go to my mentor ICT for the idea behind this script.

1BullBear™ StatisticsOverview

1BullBear™ Statistics is a comprehensive volume delta analysis tool that transforms raw order flow data into actionable visual insights. This indicator displays seven key metrics in a clean, gradient-based heatmap format below your price chart, helping you identify significant buying and selling pressure in real-time.

Key Features: Seven Essential Metrics

Volume - Total volume per bar with threshold highlighting

Delta - Net buying/selling pressure (Buy Volume - Sell Volume)

Cumulative Delta - Session-based running total of delta

Delta Ratio - Delta expressed as a percentage of total volume

Minimum - Lowest delta value within the bar's timeframe

Maximum - Highest delta value within the bar's timeframe

Standard Deviation - Statistical measure of delta volatility within the session

Intelligent Gradient Visualization

Dynamic color intensity based on historical significance

Adaptive scaling using configurable lookback periods (10-200 bars)

Threshold-based highlighting to immediately spot extreme values

Separate bull/bear coloring for directional clarity

Customizable transparency for optimal chart integration

Flexible Configuration

Toggle any metric on/off to focus on what matters

Custom labels - rename metrics to your preference

Independent color schemes for each row

Adjustable thresholds for highlighting significant values

Multiple text sizes from tiny to huge

Session-aware calculations that reset at market open

Real-Time Updates

Confirmed bars display permanent historical data

Current bar updates in real-time as price action develops

Efficient rendering with automatic cleanup of previous bars

Handles up to 500 boxes for extensive historical analysis

How It Works

The indicator uses TradingView's native volume delta data (sourced from lower timeframe aggregation) to calculate order flow statistics. Each metric is displayed as a colored box below the chart, with gradient intensity representing the value's significance relative to recent history.

Gradient Logic:

Stronger colors = more significant values relative to the lookback period

Transparent backgrounds = values below threshold (filtered out)

Color saturation scales from 0% to your set maximum opacity

Session Management:

Cumulative Delta and Standard Deviation reset at each new trading session

Session detection uses exchange timezone for accurate daily calculations

Historical lookback maintains a rolling window for gradient intensity

I deal Use Cases

Scalping & Day Trading - Identify aggressive buying/selling in real-time

Order Flow Analysis - Understand market participant behavior

Divergence Detection - Spot when price and delta disagree

Volume Profile Context - Complement VP analysis with granular delta data

Breakout Confirmation - Verify price moves with volume delta agreement

Default Thresholds

The indicator comes pre-configured with sensible defaults for futures trading:

Volume: Highlights bars above 1,500 contracts

Delta: Flags extremes beyond ±500

Delta Ratio: Alerts on imbalances beyond ±70%

Min/Max: Range filter of ±10 for precision

Std Dev: Highlights outliers beyond ±0.7 standard deviations

Adjust these values based on your instrument and timeframe.

Technical Notes

Requires real-time volume delta data from your broker

Works best on instruments with strong volume (futures, major stocks, crypto)

Lower timeframe aggregation defaults to 1-second or 1-minute depending on chart timeframe

Optimized performance with efficient array management and conditional rendering

Compatibility

Pine Script™ v6

All timeframes supported

Best results on liquid instruments with reliable volume data

Integrates seamlessly with other TradingView indicators

Created by KweeBoss_ | Licensed under Mozilla Public License 2.0

Note: This indicator analyzes historical and real-time volume data. Past performance does not guarantee future results. Always combine with other forms of analysis and proper risk management.

Emerson v8.4 – Kulture Metrics🜂 Emerson v8.4 – Kulture Metrics

“When volatility breathes, probability answers.”

The Emerson Engine isn’t another indicator—it’s a precision instrument built to exploit the hidden mathematics of motion.

Born from Kulture Metrics’ Nosreme lineage, this model fuses trend architecture, volatility anatomy, and Linetsky’s path-integral weighting into one living signal core. It doesn’t predict — it quantifies belief.

Each trigger passes through three unforgiving filters:

Classical Trend & Momentum Logic — directional strength, pure and unadulterated.

Squeeze Regime Anticipation — volatility compression before the break.

Path-Integral Confirmation — stochastic payoffs weighted by risk-free discounting and volatility density.

The result?

Only signals where the math, the market, and the moment all align — Absolute Confirmations.

No noise. No guessing. No emotion.

In practice, Emerson waits. It calculates. Then it strikes with surgical precision — entries that respect volatility, discount rates, and expected path contributions like a derivatives desk built into your chart.

Each decision point carries the full weight of stochastic probability theory — the same principles driving modern option pricing — yet distilled into something you can read at a glance.

Benefits that separate you from the herd:

✅ Trades filtered by volatility percentile and expected payoff distribution — not gut feel.

✅ Dotted bias line reveals the “probabilistic current” beneath price itself.

✅ Alerts trigger only when logic, momentum, and probability form a unanimous verdict.

✅ Dynamic macro-window shading adapts to volatility pressure in real time.

✅ Every entry inherently respects your risk, target, and discounting horizon.

Emerson v8.4 doesn’t ask the market what’s happening — it tells it what must happen next, given the probabilities.

It’s not designed to comfort. It’s designed to confirm.

Kulture Metrics. Built for traders who understand that randomness is just order not yet resolved.

Michie Breakout 1.0A precision breakout indicator built with adaptive machine learning logic and price action principles.

Designed specifically for TSLA, it detects key volatility shifts and directional momentum zones to capture high-probability breakout setups while filtering noise.

Focuses on clarity, adaptability, and accuracy — optimized for real-time intraday trading.

TraderMathLibrary "TraderMath"

A collection of essential trading utilities and mathematical functions used for technical analysis,

including DEMA, Fisher Transform, directional movement, and ADX calculations.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

roundVal(val)

Constrains a value to the range .

Parameters:

val (float) : (float) Value to constrain.

Returns: (float) Value limited to the range .

fisherTransform(length)

Computes the Fisher Transform oscillator, enhancing turning point sensitivity.

Parameters:

length (int) : (int) Lookback length used to normalize price within the high-low range.

Returns: (float) Fisher Transform value.

dirmov(len)

Calculates the Plus and Minus Directional Movement components (DI+ and DI−).

Parameters:

len (simple int) : (int) Lookback length for directional movement.

Returns: (float ) Array containing .

adx(dilen, adxlen)

Computes the Average Directional Index (ADX) based on DI+ and DI−.

Parameters:

dilen (simple int) : (int) Lookback length for directional movement calculation.

adxlen (simple int) : (int) Smoothing length for ADX computation.

Returns: (float) Average Directional Index value (0–100).

VWAP Kalman FilterOverview

This indicator applies Kalman filtering techniques to Volume Weighted Average Price (VWAP) calculations, providing a statistically optimized approach to VWAP analysis. The Kalman filter reduces noise while maintaining responsiveness to genuine price movements, addressing common VWAP limitations in volatile or low-volume conditions.

Technical Implementation

Kalman Filter Mathematics

The indicator implements a state-space model for VWAP estimation:

- Prediction Step: x̂(k|k-1) = x̂(k-1|k-1) + v(k-1)

- Update Step: x̂(k|k) = x̂(k|k-1) + K(k)

- Kalman Gain: K(k) = P(k|k-1) / (P(k|k-1) + R)

Where:

- x̂ = estimated VWAP state

- K = Kalman gain (adaptive weighting factor)

- P = error covariance

- R = measurement noise

- Q = process noise

- v = optional velocity component

Core Components

Dual VWAP System

- Standard VWAP: Traditional volume-weighted calculation

- Kalman-filtered VWAP: Noise-reduced estimation with optional velocity tracking

- Real-time divergence measurement between filtered and unfiltered values

Adaptive Filtering

- Process Noise (Q): Controls adaptation to price changes (0.001-1.0)

- Measurement Noise (R): Determines smoothing intensity (0.01-5.0)

- Optional velocity tracking for momentum-based filtering

Multi-Timeframe Anchoring

- Session, Weekly, Monthly, Quarterly, and Yearly anchor periods

- Automatic Kalman state reset on anchor changes

- Maintains VWAP integrity across timeframes

Features

Visual Components

- Dual VWAP Lines: Compare filtered vs. unfiltered in real-time

- Dynamic Bands: Three-level deviation bands (1σ, 2σ, 3σ)

- Trend Coloring: Automatic color adaptation based on price position

- Cloud Visualization: Highlights divergence between standard and Kalman VWAP

- Signal Markers: Crossover and band-touch indicators

Trading Signals

- VWAP crossover detection with Kalman filtering

- Band touch alerts at multiple standard deviation levels

- Velocity-based momentum confirmation (optional)

- Divergence warnings when filtered/unfiltered values separate

Information Display

- Real-time VWAP values (both standard and filtered)

- Trend direction indicator

- Velocity/momentum reading (when enabled)

- Divergence percentage calculation

- Anchor period display

Input Parameters

VWAP Settings

- Anchor Period: Choose calculation reset period

- Band Multipliers: Customize deviation band distances

- Display Options: Toggle standard VWAP and bands

Kalman Parameters

- Length: Base period for calculations (5-200)

- Process Noise (Q: Higher values increase responsiveness

- Measurement Noise (R): Higher values increase smoothing

- Velocity Tracking: Enable momentum-based filtering

Visual Controls

- Toggle filtered/unfiltered VWAP display

- Band visibility options

- Signal markers on/off

- Cloud fill between VWAPs

- Bar coloring by trend

Use Cases

Noise Reduction

Particularly effective during:

- Low volume periods (pre-market, lunch hours)

- Volatile market conditions

- Fast-moving markets where standard VWAP whipsaws

Trend Identification

- Cleaner trend signals with reduced false crosses

- Earlier trend detection through velocity component

- Confirmation through divergence analysis

Support/Resistance

- Filtered VWAP provides more stable S/R levels

- Bands adapt to filtered values for better zone identification

- Reduced false breakout signals

Technical Advantages

1. Optimal Estimation: Mathematically optimal under Gaussian noise assumptions

2. Adaptive Response: Self-adjusting to market conditions

3. Predictive Element: Velocity component provides forward-looking insight

4. Noise Immunity: Superior noise rejection vs. simple moving average smoothing

Limitations

- Assumes linear price dynamics

- Requires parameter optimization for different instruments

- May lag during sudden volatility regime changes

- Not suitable as standalone trading system

Mathematical Background

Based on control systems theory, the Kalman filter provides recursive Bayesian estimation originally developed for aerospace applications. This implementation adapts the algorithm specifically for financial time series, maintaining VWAP's volume-weighted properties while adding statistical filtering.

Comparison with Standard VWAP

Standard VWAP Issues Addressed:

- Choppy behavior in low volume

- Whipsaws around VWAP line

- Lag in trend identification

- Noise in deviation bands

Kalman VWAP Benefits:

- Smooth yet responsive line

- Fewer false signals

- Optional momentum tracking

- Statistically optimized filtering

Alert Conditions

The indicator includes several pre-configured alert conditions:

- Bullish/Bearish VWAP crosses

- Upper/Lower band touches

- High divergence warnings

- Velocity shifts (if enabled)

---

This open-source indicator is provided as-is for educational and trading purposes. No guarantees are made regarding trading performance. Users should conduct their own testing and validation before using in live trading.

Dynamic S/R Levels - MTF (1-Week, Strong/Spaced)dynamic support and resistance levels based on timeframe

Info de Vela 1m1-Minute Candle Info Dashboard (Real-Time)

Overview

This is a lightweight, real-time dashboard designed specifically for 1-minute (1m) scalping. It provides critical, non-lagging data about the current 1-minute candle, helping you make split-second decisions on stop-loss placement and risk assessment.The table updates on every tick without flickering or repainting.

Key Features (Real-Time Table)

The dashboard displays three key metrics about the current 1m candle:Time Remaining: A simple countdown timer showing the exact seconds remaining until the current candle closes (e.g., "00:34").Dist. to Extreme (Ticks): This is the core function for scalping. It calculates the distance (in ticks) from the current price to the furthest extreme of the candle (i.e., max(high - close, close - low)). This is ideal for traders who base their stop-loss on the current candle's range.Total Candle Range (Ticks): Displays the full high-to-low range of the current candle in ticks, giving you an instant read on volatility.

How to Use

This tool is designed to solve one problem: speed.Instead of manually measuring the distance for your stop-loss on every candle, you can instantly read the exact tick value from the table. This allows you to calculate your position size (lotage) much faster, which is essential in a fast-moving 1m environment.

REQUIREMENT:This indicator is designed to work ONLY on the 1-minute (1m) timeframe. It will display an error and show no data on any other chart.