FunctionSurvivalEstimationLibrary "FunctionSurvivalEstimation"

The Survival Estimation function, also known as Kaplan-Meier estimation or product-limit method, is a statistical technique used to estimate the survival probability of an individual over time. It's commonly used in medical research and epidemiology to analyze the survival rates of patients with different treatments, diseases, or risk factors.

What does it do?

The Survival Estimation function takes into account censored observations (i.e., individuals who are still alive at a certain point) and calculates the probability that an individual will survive beyond a specific time period. It's particularly useful when dealing with right-censoring, where some subjects are lost to follow-up or have not experienced the event of interest by the end of the study.

Interpretation

The Survival Estimation function provides a plot of the estimated survival probability over time, which can be used to:

1. Compare survival rates between different groups (e.g., treatment arms)

2. Identify patterns in the data that may indicate differences in mortality or disease progression

3. Make predictions about future outcomes based on historical data

4. In a trading context it may be used to ascertain the survival ratios of trading under specific conditions.

Reference:

www.global-developments.org

"Beyond GDP" ~ www.aeaweb.org

en.wikipedia.org

www.kdnuggets.com

survival_probability(alive_at_age, initial_alive)

Kaplan-Meier Survival Estimator.

Parameters:

alive_at_age (int) : The number of subjects still alive at a age.

initial_alive (int) : The Total number of initial subjects.

Returns: The probability that a subject lives longer than a certain age.

utility(c, l)

Captures the utility value from consumption and leisure.

Parameters:

c (float) : Consumption.

l (float) : Leisure.

Returns: Utility value from consumption and leisure.

welfare_utility(age, b, u, s)

Calculate the welfare utility value based age, basic needs and social interaction.

Parameters:

age (int) : Age of the subject.

b (float) : Value representing basic needs (food, shelter..).

u (float) : Value representing overall well-being and happiness.

s (float) : Value representing social interaction and connection with others.

Returns: Welfare utility value.

expected_lifetime_welfare(beta, consumption, leisure, alive_data, expectation)

Calculates the expected lifetime welfare of an individual based on their consumption, leisure, and survival probability over time.

Parameters:

beta (float) : Discount factor.

consumption (array) : List of consumption values at each step of the subjects life.

leisure (array) : List of leisure values at each step of the subjects life.

alive_data (array) : List of subjects alive at each age, the first element is the total or initial number of subjects.

expectation (float) : Optional, `defaut=1.0`. Expectation or weight given to this calculation.

Returns: Expected lifetime welfare value.

MATH

PineVersatilitiesBundleLibrary "PineVersatilitiesBundle"

Versatilities (aka, Versatile Utilities) Pack includes:

- Eighteen Price Variants bundled in a Map,

- Nine Smoothing Variants bundled in a Map,

- Visualisations that indicate on both - pane and chart.

price_variants(lb)

Computes Several different averages using current and previous OHLC values

Parameters:

lb (int) : - lookback distance for combining OHLC values from the past with the present

Returns: Map of Eighteen Uncommon Combinations of single and two-bar OHLC averages (rounded-to-mintick)

dynamic_MA(masrc, malen, lsmaoff, almasgm, almaoff, almaflr)

Dynamically computes Eight different MAs and returns a Map containing Nine MAs

Parameters:

masrc (float) : source series to compute MA

malen (simple int) : lookback distance for MA

lsmaoff (simple int) : optional LSMA offset - default is 0

almasgm (simple float) : optional ALMA sigma - default is 5

almaoff (simple float) : optional ALMA offset - default is 0.5

almaflr (simple bool) : optional ALMA floor flag - default is false

Returns: Map of MAs - 'ALMA', 'EMA', 'HMA', 'LSMA', 'RMA', 'SMA', 'SWMA', 'WMA', 'ALL' (rounded-to-mintick)

NR_VersatilitiesLibrary "NR_Versatilities"

Versatilities (aka, Versatile Utilities) includes:

- Seventeen Price Variants returned as a tuple,

- Eight Smoothing functions rolled into one,

- Pick any Past Value from any series with offset,

- Or just the previous value from any series.

pastVal(src, len)

Fetches past value from src that came len distance ago

Parameters:

src (float) : source series

len (int) : lookback distance - (optional) default is 1

Returns: latest src if len <= 0, else src

previous(src)

Fetches past value from src that came len distance ago

Parameters:

src (float) : source series

Returns: previous value in the series if found, else current value

price_variants()

Computes Several different averages using current and previous OHLC values

Returns: Seventeen Uncommon Average Price Combinations

dynamic_MA(matyp, masrc, malen, lsmaoff, almasgm, almaoff, almaflr)

Dynamically computes Eight different MAs on-demand individually, or an average of all taken together

Parameters:

matyp (string) : pick one of these MAs - ALMA, EMA, HMA, LSMA, RMA, SMA, SWMA, WMA, ALL

masrc (float) : source series to compute MA

malen (simple int) : lookback distance for MA

lsmaoff (simple int) : optional LSMA offset - default is 0

almasgm (simple float) : optional ALMA sigma - default is 5

almaoff (simple float) : optional ALMA offset - default is 0.5

almaflr (simple bool) : optional ALMA floor flag - default is false

Returns: MA series for chosen type or, an average of all of them, if chosen so

TimeframeUtilsCustomLibrary "TimeframeUtilsCustom"

Timeframe utilities library

f_timeframe_to_minutes(tf)

Converts timeframe string to minutes

Parameters:

tf (string) : String representation of timeframe

Returns: Number of minutes in the given timeframe

f_bars_for_hours(timeframe_minutes, hours)

Calculate number of bars for a specified time period

Parameters:

timeframe_minutes (int) : Current timeframe in minutes

hours (int) : Number of hours to calculate bars for

Returns: Number of bars representing the specified hours

f_bars_for_days(timeframe_minutes, days)

Calculate number of bars for a specified number of days

Parameters:

timeframe_minutes (int) : Current timeframe in minutes

days (int) : Number of days to calculate bars for

Returns: Number of bars representing the specified days

rate_of_changeLibrary "rate_of_change"

// @description: Applies ROC algorithm to any pair of values.

// This library function is used to scale change of value (price, volume) to a percentage value, just as the ROC indicator would do. It is good practice to scale arbitrary ranges to set boundaries when you try to train statistical model.

rateOfChange(value, base, hardlimit)

This function is a helper to scale a value change to its percentage value.

Parameters:

value (float)

base (float)

hardlimit (int)

Returns: per: A float comprised between 0 and 100

merge_pinbar_babyblueLibrary "merge_pinbar_babyblue"

merge_pinbar: merge bars and check whether the bar is a pinbar

merge_pinbar_babyblue(period, max_bars)

merge_pinbar: merge bars and check whether the bar is a pinbar

Parameters:

period (simple int)

max_bars (simple int)

Returns: array:

DynamicMALibrary "DynamicMA"

Dynamic Moving Averages Library

Introduction

The Dynamic Moving Averages Library is a specialized collection of custom built functions designed to calculate moving averages dynamically, beginning from the first available bar. Unlike standard moving averages, which rely on fixed length lookbacks, this library ensures that indicators remain fully functional from the very first data point, making it an essential tool for analysing assets with short time series or limited historical data.

This approach allows traders and developers to build robust indicators that do not require a preset amount of historical data before generating meaningful outputs. It is particularly advantageous for:

Newly listed assets with minimal price history.

High-timeframe trading, where large lookback periods can lead to delayed or missing data.

By eliminating the constraints of fixed lookback periods, this library enables the seamless construction of trend indicators, smoothing functions, and hybrid models that adapt instantly to market conditions.

Comprehensive Set of Custom Moving Averages

The library includes a wide range of custom dynamic moving averages, each designed for specific analytical use cases:

SMA (Simple Moving Average) – The fundamental moving average, dynamically computed.

EMA (Exponential Moving Average) – Adaptive smoothing for better trend tracking.

DEMA (Double Exponential Moving Average) – Faster trend detection with reduced lag.

TEMA (Triple Exponential Moving Average) – Even more responsive than DEMA.

WMA (Weighted Moving Average) – Emphasizes recent price action while reducing noise.

VWMA (Volume Weighted Moving Average) – Accounts for volume to give more weight to high-volume periods.

HMA (Hull Moving Average) – A superior smoothing method with low lag.

SMMA (Smoothed Moving Average) – A hybrid approach between SMA and EMA.

LSMA (Least Squares Moving Average) – Uses linear regression for trend detection.

RMA (Relative Moving Average) – Used in RSI-based calculations for smooth momentum readings.

ALMA (Arnaud Legoux Moving Average) – A Gaussian-weighted MA for superior signal clarity.

Hyperbolic MA (HyperMA) – A mathematically optimized averaging method with dynamic weighting.

Each function dynamically adjusts its calculation length to match the available bar count, ensuring instant functionality on all assets.

Fully Optimized for Pine Script v6

This library is built on Pine Script v6, ensuring compatibility with modern TradingView indicators and scripts. It includes exportable functions for seamless integration into custom indicators, making it easy to develop trend-following models, volatility filters, and adaptive risk-management systems.

Why Use Dynamic Moving Averages?

Traditional moving averages suffer from a common limitation: they require a fixed historical window to generate meaningful values. This poses several problems:

New Assets Have No Historical Data - If an asset has only been trading for a short period, traditional moving averages may not be able to generate valid signals.

High Timeframes Require Massive Lookbacks - On 1W or 1M charts, a 200-period SMA would require 200 weeks or months of data, making it unusable on newer assets.

Delayed Signal Initialization - Standard indicators often take dozens of bars to stabilize, reducing effectiveness when trading new trends.

The Dynamic Moving Averages Library eliminates these issues by ensuring that every function:

Starts calculation from bar one, using available data instead of waiting for a lookback period.

Adapts dynamically across timeframes, making it equally effective on low or high timeframes.

Allows smoother, more responsive trend tracking, particularly useful for volatile or low-liquidity assets.

This flexibility makes it indispensable for custom script developers, quantitative analysts, and discretionary traders looking to build more adaptive and resilient indicators.

Final Summary

The Dynamic Moving Averages Library is a versatile and powerful set of functions designed to overcome the limitations of fixed-lookback indicators. By dynamically adjusting the calculation length from the first bar, this library ensures that moving averages remain fully functional across all timeframes and asset types, making it an essential tool for traders and developers alike.

With built-in adaptability, low-lag smoothing, and support for multiple moving average types, this library unlocks new possibilities for quantitative trading and strategy development - especially for assets with short price histories or those traded on higher timeframes.

For traders looking to enhance signal reliability, minimize lag, and build adaptable trading systems, the Dynamic Moving Averages Library provides an efficient and flexible solution.

SMA(sourceData, maxLength)

Dynamic SMA

Parameters:

sourceData (float)

maxLength (int)

EMA(src, length)

Dynamic EMA

Parameters:

src (float)

length (int)

DEMA(src, length)

Dynamic DEMA

Parameters:

src (float)

length (int)

TEMA(src, length)

Dynamic TEMA

Parameters:

src (float)

length (int)

WMA(src, length)

Dynamic WMA

Parameters:

src (float)

length (int)

HMA(src, length)

Dynamic HMA

Parameters:

src (float)

length (int)

VWMA(src, volsrc, length)

Dynamic VWMA

Parameters:

src (float)

volsrc (float)

length (int)

SMMA(src, length)

Dynamic SMMA

Parameters:

src (float)

length (int)

LSMA(src, length, offset)

Dynamic LSMA

Parameters:

src (float)

length (int)

offset (int)

RMA(src, length)

Dynamic RMA

Parameters:

src (float)

length (int)

ALMA(src, length, offset_sigma, sigma)

Dynamic ALMA

Parameters:

src (float)

length (int)

offset_sigma (float)

sigma (float)

HyperMA(src, length)

Dynamic HyperbolicMA

Parameters:

src (float)

length (int)

PaddingThe Padding library is a comprehensive and flexible toolkit designed to extend time series data within TradingView, making it an indispensable resource for advanced signal processing tasks such as FFT, filtering, convolution, and wavelet analysis. At its core, the library addresses the common challenge of edge effects by "padding" your data—that is, by appending additional data points beyond the natural boundaries of your original dataset. This extension not only mitigates the distortions that can occur at the endpoints but also helps to maintain the integrity of various transformations and calculations performed on the series. The library accomplishes this while preserving the ordering of your data, ensuring that the most recent point always resides at index 0.

Central to the functionality of this library are two key enumerations: Direction and PaddingType. The Direction enum determines where the padding will be applied. You can choose to extend the data in the forward direction (ahead of the current values), in the backward direction (behind the current values), or in both directions simultaneously. The PaddingType enum defines the specific method used for extending the data. The library supports several methods—including symmetric, reflect, periodic, antisymmetric, antireflect, smooth, constant, and zero padding—each of which has been implemented to suit different analytical scenarios. For instance, symmetric padding mirrors the original data across its boundaries, while reflect padding continues the trend by reflecting around endpoint values. Periodic padding repeats the data, and antisymmetric padding mirrors the data with alternating signs to counterbalance it. The antireflect and smooth methods take into account the derivatives of your data, thereby extending the series in a way that preserves or smoothly continues these derivative values. Constant and zero padding simply extend the series using fixed endpoint values or zeros. Together, these enums allow you to fine-tune how your data is extended, ensuring that the padding method aligns with the specific requirements of your analysis.

The library is designed to work with both single variable inputs and array inputs. When using array-based methods—particularly with the antireflect and smooth padding types—please note that the implementation intentionally discards the last data point as a result of the delta computation process. This behavior is an important consideration when integrating the library into your TradingView studies, as it affects the overall data length of the padded series. Despite this, the library’s structure and documentation make it straightforward to incorporate into your existing scripts. You simply provide your data source, define the length of your data window, and select the desired padding type and direction, along with any optional parameters to control the extent of the padding (using both_period, forward_period, or backward_period).

In practical application, the Padding library enables you to extend historical data beyond its original range in a controlled and predictable manner. This is particularly useful when preparing datasets for further signal processing, as it helps to reduce artifacts that can otherwise compromise the results of your analytical routines. Whether you are an experienced Pine Script developer or a trader exploring advanced data analysis techniques, this library offers a robust solution that enhances the reliability and accuracy of your studies by ensuring your algorithms operate on a more complete and well-prepared dataset.

Library "Padding"

A comprehensive library for padding time series data with various methods. Supports both single variable and array inputs, with flexible padding directions and periods. Designed for signal processing applications including FFT, filtering, convolution, and wavelets. All methods maintain data ordering with most recent point at index 0.

symmetric(source, series_length, direction, both_period, forward_period, backward_period)

Applies symmetric padding by mirroring the input data across boundaries

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with symmetric padding applied

method symmetric(source, direction, both_period, forward_period, backward_period)

Applies symmetric padding to an array by mirroring the data across boundaries

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with symmetric padding applied

reflect(source, series_length, direction, both_period, forward_period, backward_period)

Applies reflect padding by continuing trends through reflection around endpoint values

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with reflect padding applied

method reflect(source, direction, both_period, forward_period, backward_period)

Applies reflect padding to an array by continuing trends through reflection around endpoint values

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with reflect padding applied

periodic(source, series_length, direction, both_period, forward_period, backward_period)

Applies periodic padding by repeating the input data

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with periodic padding applied

method periodic(source, direction, both_period, forward_period, backward_period)

Applies periodic padding to an array by repeating the data

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with periodic padding applied

antisymmetric(source, series_length, direction, both_period, forward_period, backward_period)

Applies antisymmetric padding by mirroring data and alternating signs

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antisymmetric padding applied

method antisymmetric(source, direction, both_period, forward_period, backward_period)

Applies antisymmetric padding to an array by mirroring data and alternating signs

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antisymmetric padding applied

antireflect(source, series_length, direction, both_period, forward_period, backward_period)

Applies antireflect padding by reflecting around endpoints while preserving derivatives

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antireflect padding applied

method antireflect(source, direction, both_period, forward_period, backward_period)

Applies antireflect padding to an array by reflecting around endpoints while preserving derivatives

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antireflect padding applied. Note: Last data point is lost when using array input

smooth(source, series_length, direction, both_period, forward_period, backward_period)

Applies smooth padding by extending with constant derivatives from endpoints

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with smooth padding applied

method smooth(source, direction, both_period, forward_period, backward_period)

Applies smooth padding to an array by extending with constant derivatives from endpoints

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with smooth padding applied. Note: Last data point is lost when using array input

constant(source, series_length, direction, both_period, forward_period, backward_period)

Applies constant padding by extending endpoint values

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with constant padding applied

method constant(source, direction, both_period, forward_period, backward_period)

Applies constant padding to an array by extending endpoint values

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with constant padding applied

zero(source, series_length, direction, both_period, forward_period, backward_period)

Applies zero padding by extending with zeros

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with zero padding applied

method zero(source, direction, both_period, forward_period, backward_period)

Applies zero padding to an array by extending with zeros

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with zero padding applied

pad_data(source, series_length, padding_type, direction, both_period, forward_period, backward_period)

Generic padding function that applies specified padding type to input data

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with specified padding applied

method pad_data(source, padding_type, direction, both_period, forward_period, backward_period)

Generic padding function that applies specified padding type to array input

Namespace types: array

Parameters:

source (array) : Array of values to pad

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with specified padding applied. Note: Last data point is lost when using antireflect or smooth padding types

make_padded_data(source, series_length, padding_type, direction, both_period, forward_period, backward_period)

Creates a window-based padded data series that updates with each new value. WARNING: Function must be called on every bar for consistency. Do not use in scopes where it may not execute on every bar.

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing windowed data with specified padding applied

UtilityLibraryLibrary "UtilityLibrary"

A collection of custom utility functions used in my scripts.

milliseconds_per_bar()

Gets the number of milliseconds per bar.

Returns: (int) The number of milliseconds per bar.

realtime()

Checks if the current bar is the actual realtime bar.

Returns: (bool) `true` when the current bar is the actual realtime bar, `false` otherwise.

replay()

Checks if the current bar is the last replay bar.

Returns: (bool) `true` when the current bar is the last replay bar, `false` otherwise.

bar_elapsed()

Checks how much of the current bar has elapsed.

Returns: (float) Between 0 and 1.

even(number)

Checks if a number is even.

Parameters:

number (float) : (float) The number to evaluate.

Returns: (bool) `true` when the number is even, `false` when the number is odd.

sign(number)

Gets the sign of a float.

Parameters:

number (float) : (float) The number to evaluate.

Returns: (int) 1 or -1, unlike math.sign() which returns 0 if the number is 0.

atan2(y, x)

Derives an angle in radians from the XY coordinate.

Parameters:

y (float) : (float) Y coordinate.

x (float) : (float) X coordinate.

Returns: (float) Between -π and π.

clamp(number, min, max)

Ensures a value is between the `min` and `max` thresholds.

Parameters:

number (float) : (float) The number to clamp.

min (float) : (float) The minimum threshold (0 by default).

max (float) : (float) The maximum threshold (1 by default).

Returns: (float) Between `min` and `max`.

remove_gamma(value)

Removes gamma from normalized sRGB channel values.

Parameters:

value (float) : (float) The normalized channel value .

Returns: (float) Channel value with gamma removed.

add_gama(value)

Adds gamma into normalized linear RGB channel values.

Parameters:

value (float) : (float) The normalized channel value .

Returns: (float) Channel value with gamma added.

rgb_to_xyz(Color)

Extracts XYZ-D65 channels from sRGB colors.

Parameters:

Color (color) : (color) The sRGB color to process.

Returns: (float tuple)

xyz_to_rgb(x, y, z)

Converts XYZ-D65 channels to sRGB channels.

Parameters:

x (float) : (float) The X channel value.

y (float) : (float) The Y channel value.

z (float) : (float) The Z channel value.

Returns: (int tuple)

rgb_to_oklab(Color)

Extracts OKLAB-D65 channels from sRGB colors.

Parameters:

Color (color) : (color) The sRGB color to process.

Returns: (float tuple)

oklab_to_rgb(l, a, b)

Converts OKLAB-D65 channels to sRGB channels.

Parameters:

l (float) : (float) The L channel value.

a (float) : (float) The A channel value.

b (float) : (float) The B channel value.

Returns: (int tuple)

rgb_to_oklch(Color)

Extracts OKLCH channels from sRGB colors.

Parameters:

Color (color) : (color) The sRGB color to process.

Returns: (float tuple)

oklch_to_rgb(l, c, h)

Converts OKLCH channels to sRGB channels.

Parameters:

l (float) : (float) The L channel value.

c (float) : (float) The C channel value.

h (float) : (float) The H channel value.

Returns: (float tuple)

hues(l1, h1, l2, h2, dist)

Ensures the hue angles are set correctly for linearly interpolating OKLCH.

Parameters:

l1 (float) : (float) The first L channel value.

h1 (float) : (float) The first H channel value.

l2 (float) : (float) The second L channel value.

h2 (float) : (float) The second H channel value.

dist (string) : (string) The preferred angular distance to use. Options: `min` or `max` (`min` by default).

Returns: (float tuple)

lerp(a, b, t)

Linearly interpolates between two values.

Parameters:

a (float) : (float) The starting point (first value).

b (float) : (float) The ending point (second value).

t (float) : (float) The interpolation factor .

Returns: (float) Between `a` and `b`.

smoothstep(t, precise)

A non-linear (smooth) interpolation between 0 and 1.

Parameters:

t (float) : (float) The interpolation factor .

precise (bool) : (bool) Sets if the calc should be precise or efficient (`true` by default).

Returns: (float) Between 0 and 1.

ease(t, n, v, x1, y1, x2, y2)

A customizable non-linear interpolation between 0 and 1.

Parameters:

t (float) : (float) The interpolation factor .

n (float) : (float) The degree of ease (1 by default).

v (string) : (string) The easing variant type: `in-out`, `in`, or `out` (`in-out` by default).

x1 (float) : (float) Optional X coordinate of starting point (0 by default).

y1 (float) : (float) Optional Y coordinate of starting point (0 by default).

x2 (float) : (float) Optional X coordinate of ending point (1 by default).

y2 (float) : (float) Optional Y coordinate of ending point (1 by default).

Returns: (float) Between 0 and 1.

mix(color1, color2, blend, space, dist)

Linearly interpolates between two colors.

Parameters:

color1 (color) : (color) The first color.

color2 (color) : (color) The second color.

blend (float) : (float) The interpolation factor .

space (string) : (string) The color space to use for interpolating. Options: `rgb`, `oklab`, and `oklch` (`rgb` by default).

dist (string) : (string) The anglular distance to use for the hue change when the color space is set to `oklch`. Options: `min` and `max` (`min` by default).

Returns: (color) Blend of `color1` and `color2`.

waves█ OVERVIEW

This library intended for use in Bar Replay provides functions to generate various wave forms (sine, cosine, triangle, square) based on time and customizable parameters. Useful for testing and in creating oscillators, indicators, or visual effects.

█ FUNCTIONS

• getSineWave()

• getCosineWave()

• getTriangleWave()

• getSquareWave()

█ USAGE EXAMPLE

//@version=6

indicator("Wave Example")

import kaigouthro/waves/1

plot(waves.getSineWave(cyclesPerMinute=15))

█ NOTES

* barsPerSecond defaults to 10. Adjust this if not using 10x in Bar Replay.

* Phase shift is in degrees.

---

Library "waves"

getSineWave(cyclesPerMinute, bar, barsPerSecond, amplitude, verticalShift, phaseShift)

`getSineWave`

> Calculates a sine wave based on bar index, cycles per minute (BPM), and wave parameters.

Parameters:

cyclesPerMinute (float) : (float) The desired number of cycles per minute (BPM). Default is 30.0.

bar (int) : (int) The current bar index. Default is bar_index.

barsPerSecond (float) : (float) The number of bars per second. Default is 10.0 for Bar Replay

amplitude (float) : (float) The amplitude of the sine wave. Default is 1.0.

verticalShift (float) : (float) The vertical shift of the sine wave. Default is 0.0.

phaseShift (float) : (float) The phase shift of the sine wave in radians. Default is 0.0.

Returns: (float) The calculated sine wave value.

getCosineWave(cyclesPerMinute, bar, barsPerSecond, amplitude, verticalShift, phaseShift)

`getCosineWave`

> Calculates a cosine wave based on bar index, cycles per minute (BPM), and wave parameters.

Parameters:

cyclesPerMinute (float) : (float) The desired number of cycles per minute (BPM). Default is 30.0.

bar (int) : (int) The current bar index. Default is bar_index.

barsPerSecond (float) : (float) The number of bars per second. Default is 10.0 for Bar Replay

amplitude (float) : (float) The amplitude of the cosine wave. Default is 1.0.

verticalShift (float) : (float) The vertical shift of the cosine wave. Default is 0.0.

phaseShift (float) : (float) The phase shift of the cosine wave in radians. Default is 0.0.

Returns: (float) The calculated cosine wave value.

getTriangleWave(cyclesPerMinute, bar, barsPerSecond, amplitude, verticalShift, phaseShift)

`getTriangleWave`

> Calculates a triangle wave based on bar index, cycles per minute (BPM), and wave parameters.

Parameters:

cyclesPerMinute (float) : (float) The desired number of cycles per minute (BPM). Default is 30.0.

bar (int) : (int) The current bar index. Default is bar_index.

barsPerSecond (float) : (float) The number of bars per second. Default is 10.0 for Bar Replay

amplitude (float) : (float) The amplitude of the triangle wave. Default is 1.0.

verticalShift (float) : (float) The vertical shift of the triangle wave. Default is 0.0.

phaseShift (float) : (float) The phase shift of the triangle wave in radians. Default is 0.0.

Returns: (float) The calculated triangle wave value.

getSquareWave(cyclesPerMinute, bar, barsPerSecond, amplitude, verticalShift, dutyCycle, phaseShift)

`getSquareWave`

> Calculates a square wave based on bar index, cycles per minute (BPM), and wave parameters.

Parameters:

cyclesPerMinute (float) : (float) The desired number of cycles per minute (BPM). Default is 30.0.

bar (int) : (int) The current bar index. Default is bar_index.

barsPerSecond (float) : (float) The number of bars per second. Default is 10.0 for Bar Replay

amplitude (float) : (float) The amplitude of the square wave. Default is 1.0.

verticalShift (float) : (float) The vertical shift of the square wave. Default is 0.0.

dutyCycle (float) : (float) The duty cycle of the square wave (0.0 to 1.0). Default is 0.5 (50% duty cycle).

phaseShift (float) : (float) The phase shift of the square wave in radians. Default is 0.0.

Returns: (float) The calculated square wave value.

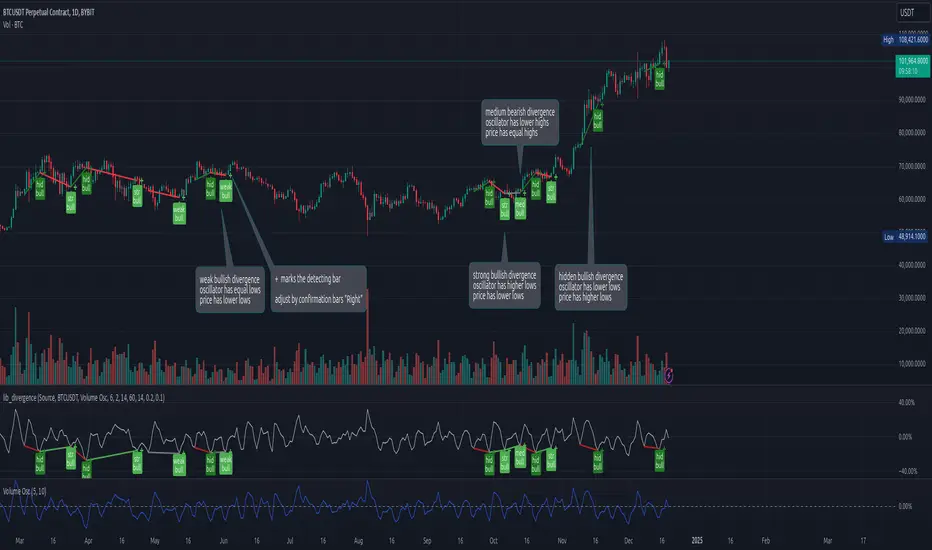

lib_divergenceLibrary "lib_divergence"

offers a commonly usable function to detect divergences. This will take the default RSI or other symbols / indicators / oscillators as source data.

divergence(osc, pivot_left_bars, pivot_right_bars, div_min_range, div_max_range, ref_low, ref_high, min_divergence_offset_fraction, min_divergence_offset_dev_len, min_divergence_offset_atr_mul)

Detects Divergences between Price and Oscillator action. For bullish divergences, look at trend lines between lows. For bearish divergences, look at trend lines between highs. (strong) oscillator trending, price opposing it | (medium) oscillator trending, price trend flat | (weak) price opposite trending, oscillator trend flat | (hidden) price trending, oscillator opposing it. Pivot detection is only properly done in oscillator data, reference price data is only compared at the oscillator pivot (speed optimization)

Parameters:

osc (float) : (series float) oscillator data (can be anything, even another instrument price)

pivot_left_bars (simple int) : (simple int) optional number of bars left of a confirmed pivot point, confirming it is the highest/lowest in the range before and up to the pivot (default: 5)

pivot_right_bars (simple int) : (simple int) optional number of bars right of a confirmed pivot point, confirming it is the highest/lowest in the range from and after the pivot (default: 5)

div_min_range (simple int) : (simple int) optional minimum distance to the pivot point creating a divergence (default: 5)

div_max_range (simple int) : (simple int) optional maximum amount of bars in a divergence (default: 50)

ref_low (float) : (series float) optional reference range to compare the oscillator pivot points to. (default: low)

ref_high (float) : (series float) optional reference range to compare the oscillator pivot points to. (default: high)

min_divergence_offset_fraction (simple float) : (simple float) optional scaling factor for the offset zone (xDeviation) around the last oscillator H/L detecting following equal H/Ls (default: 0.01)

min_divergence_offset_dev_len (simple int) : (simple int) optional lookback distance for the deviation detection for the offset zone around the last oscillator H/L detecting following equal H/Ls. Used as well for the ATR that does the equal H/L detection for the reference price. (default: 14)

min_divergence_offset_atr_mul (simple float) : (simple float) optional scaling factor for the offset zone (xATR) around the last price H/L detecting following equal H/Ls (default: 1)

@return A tuple of deviation flags.

QTALibrary "QTA"

This is simple library for basic Quantitative Technical Analysis for retail investors. One example of it being used can be seen here ().

calculateKellyRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns from bets.

Returns: The calculated Kelly Ratio, which indicates the optimal bet size based on winning and losing probabilities.

calculateAdjustedKellyFraction(kellyRatio, riskTolerance, fedStance)

Parameters:

kellyRatio (float) : The calculated Kelly Ratio.

riskTolerance (float) : A float representing the risk tolerance level.

fedStance (string) : A string indicating the Federal Reserve's stance ("dovish", "hawkish", or neutral).

Returns: The adjusted Kelly Fraction, constrained within the bounds of .

calculateStdDev(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the returns, or 0 if insufficient data.

calculateMaxDrawdown(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The maximum drawdown as a percentage.

calculateEV(avgWinReturn, winProb, avgLossReturn)

Parameters:

avgWinReturn (float) : The average return from winning bets.

winProb (float) : The probability of winning a bet.

avgLossReturn (float) : The average return from losing bets.

Returns: The calculated Expected Value of the bet.

calculateTailRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The Tail Ratio, or na if the 5th percentile is zero to avoid division by zero.

calculateSharpeRatio(avgReturn, riskFreeRate, stdDev)

Parameters:

avgReturn (float) : The average return of the investment.

riskFreeRate (float) : The risk-free rate of return.

stdDev (float) : The standard deviation of the investment's returns.

Returns: The calculated Sharpe Ratio, or na if standard deviation is zero.

calculateDownsideDeviation(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the downside returns, or 0 if no downside returns exist.

calculateSortinoRatio(avgReturn, downsideDeviation)

Parameters:

avgReturn (float) : The average return of the investment.

downsideDeviation (float) : The standard deviation of the downside returns.

Returns: The calculated Sortino Ratio, or na if downside deviation is zero.

calculateVaR(returns, confidenceLevel)

Parameters:

returns (array) : An array of floats representing the returns.

confidenceLevel (float) : A float representing the confidence level (e.g., 0.95 for 95% confidence).

Returns: The Value at Risk at the specified confidence level.

calculateCVaR(returns, varValue)

Parameters:

returns (array) : An array of floats representing the returns.

varValue (float) : The Value at Risk threshold.

Returns: The average Conditional Value at Risk, or na if no returns are below the threshold.

calculateExpectedPriceRange(currentPrice, ev, stdDev, confidenceLevel)

Parameters:

currentPrice (float) : The current price of the asset.

ev (float) : The expected value (in percentage terms).

stdDev (float) : The standard deviation (in percentage terms).

confidenceLevel (float) : The confidence level for the price range (e.g., 1.96 for 95% confidence).

Returns: A tuple containing the minimum and maximum expected prices.

calculateRollingStdDev(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling standard deviation of returns.

calculateRollingVariance(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling variance of returns.

calculateRollingMean(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling mean of returns.

calculateRollingCoefficientOfVariation(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling coefficient of variation of returns.

calculateRollingSumOfPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling sum of percent returns.

calculateRollingCumulativeProduct(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling cumulative product of returns.

calculateRollingCorrelation(priceReturns, volumeReturns, window)

Parameters:

priceReturns (array) : An array of floats representing the price returns.

volumeReturns (array) : An array of floats representing the volume returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling correlation.

calculateRollingPercentile(returns, window, percentile)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

percentile (int) : An integer representing the desired percentile (0-100).

Returns: An array of floats representing the rolling percentile of returns.

calculateRollingMaxMinPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: A tuple containing two arrays: rolling max and rolling min percent returns.

calculateRollingPriceToVolumeRatio(price, volData, window)

Parameters:

price (array) : An array of floats representing the price data.

volData (array) : An array of floats representing the volume data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling price-to-volume ratio.

determineMarketRegime(priceChanges)

Parameters:

priceChanges (array) : An array of floats representing the price changes.

Returns: A string indicating the market regime ("Bull", "Bear", or "Neutral").

determineVolatilityRegime(price, window)

Parameters:

price (array) : An array of floats representing the price data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the calculated volatility.

classifyVolatilityRegime(volatility)

Parameters:

volatility (array) : An array of floats representing the calculated volatility.

Returns: A string indicating the volatility regime ("Low" or "High").

method percentPositive(thisArray)

Returns the percentage of positive non-na values in this array.

This method calculates the percentage of positive values in the provided array, ignoring NA values.

Namespace types: array

Parameters:

thisArray (array)

_candleRange()

_PreviousCandleRange(barsback)

Parameters:

barsback (int) : An integer representing how far back you want to get a range

redCandle()

greenCandle()

_WhiteBody()

_BlackBody()

HighOpenDiff()

OpenLowDiff()

_isCloseAbovePreviousOpen(length)

Parameters:

length (int)

_isCloseBelowPrevious()

_isOpenGreaterThanPrevious()

_isOpenLessThanPrevious()

BodyHigh()

BodyLow()

_candleBody()

_BodyAvg(length)

_BodyAvg function.

Parameters:

length (simple int) : Required (recommended is 6).

_SmallBody(length)

Parameters:

length (simple int) : Length of the slow EMA

Returns: a series of bools, after checking if the candle body was less than body average.

_LongBody(length)

Parameters:

length (simple int)

bearWick()

bearWick() function.

Returns: a SERIES of FLOATS, checks if it's a blackBody(open > close), if it is, than check the difference between the high and open, else checks the difference between high and close.

bullWick()

barlength()

sumbarlength()

sumbull()

sumbear()

bull_vol()

bear_vol()

volumeFightMA()

volumeFightDelta()

weightedAVG_BullVolume()

weightedAVG_BearVolume()

VolumeFightDiff()

VolumeFightFlatFilter()

avg_bull_vol(userMA)

avg_bull_vol(int) function.

Parameters:

userMA (int)

avg_bear_vol(userMA)

avg_bear_vol(int) function.

Parameters:

userMA (int)

diff_vol(userMA)

diff_vol(int) function.

Parameters:

userMA (int)

vol_flat(userMA)

vol_flat(int) function.

Parameters:

userMA (int)

_isEngulfingBullish()

_isEngulfingBearish()

dojiup()

dojidown()

EveningStar()

MorningStar()

ShootingStar()

Hammer()

InvertedHammer()

BearishHarami()

BullishHarami()

BullishBelt()

BullishKicker()

BearishKicker()

HangingMan()

DarkCloudCover()

IndicatorsLibrary "Indicators"

cmf(lookback, n_to_smooth)

Calculates the Chaikin's Money Flow.

Parameters:

lookback (simple int)

n_to_smooth (simple int)

Returns: float The Money Flow value.

cmma(lookback, atr_length)

Calculates the CMMA (Close Minus Moving Average) indicator.

Parameters:

lookback (simple int)

atr_length (simple int)

Returns: float The CMMA value.

macd(fast_length, slow_length, n_to_smooth)

Calculates the normalized and scaled MACD.

Parameters:

fast_length (simple int)

slow_length (simple int)

n_to_smooth (simple int)

Returns: A tuple containing .

stochK(length, n_to_smooth)

Calculates a simplified Stochastic Oscillator.

Uses: 100 * ta.sma((close - lowest_low) / (highest_high - lowest_low), n_to_smooth)

Parameters:

length (simple int)

n_to_smooth (simple int)

Returns: float The Stochastic %K value.

williamsR(length)

Calculates the Williams %R using the stochK function.

Uses: -1 * (100 - stoch(length, 1))

Parameters:

length (simple int)

Returns: float The Williams %R value.

lib_kernelLibrary "lib_kernel"

Library "lib_kernel"

This is a tool / library for developers, that contains several common and adapted kernel functions as well as a kernel regression function and enum to easily select and embed a list into the settings dialog.

How to Choose and Modify Kernels in Practice

Compact Support Kernels (e.g., Epanechnikov, Triangular): Use for localized smoothing and emphasizing nearby data.

Oscillatory Kernels (e.g., Wave, Cosine): Ideal for detecting periodic patterns or mean-reverting behavior.

Smooth Tapering Kernels (e.g., Gaussian, Logistic): Use for smoothing long-term trends or identifying global price behavior.

kernel_Epanechnikov(u)

Parameters:

u (float)

kernel_Epanechnikov_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Triangular(u)

Parameters:

u (float)

kernel_Triangular_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Rectangular(u)

Parameters:

u (float)

kernel_Uniform(u)

Parameters:

u (float)

kernel_Uniform_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Logistic(u)

Parameters:

u (float)

kernel_Logistic_alt(u)

Parameters:

u (float)

kernel_Logistic_alt2(u, sigmoid_steepness)

Parameters:

u (float)

sigmoid_steepness (float)

kernel_Gaussian(u)

Parameters:

u (float)

kernel_Gaussian_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Silverman(u)

Parameters:

u (float)

kernel_Quartic(u)

Parameters:

u (float)

kernel_Quartic_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Biweight(u)

Parameters:

u (float)

kernel_Triweight(u)

Parameters:

u (float)

kernel_Sinc(u)

Parameters:

u (float)

kernel_Wave(u)

Parameters:

u (float)

kernel_Wave_alt(u)

Parameters:

u (float)

kernel_Cosine(u)

Parameters:

u (float)

kernel_Cosine_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel(u, select, alt_modificator)

wrapper for all standard kernel functions, see enum Kernel comments and function descriptions for usage szenarios and parameters

Parameters:

u (float)

select (series Kernel)

alt_modificator (float)

kernel_regression(src, bandwidth, kernel, exponential_distance, alt_modificator)

wrapper for kernel regression with all standard kernel functions, see enum Kernel comments for usage szenarios. performance optimized version using fixed bandwidth and target

Parameters:

src (float) : input data series

bandwidth (simple int) : sample window of nearest neighbours for the kernel to process

kernel (simple Kernel) : type of Kernel to use for processing, see Kernel enum or respective functions for more details

exponential_distance (simple bool) : if true this puts more emphasis on local / more recent values

alt_modificator (float) : see kernel functions for parameter descriptions. Mostly used to pronounce emphasis on local values or introduce a decay/dampening to the kernel output

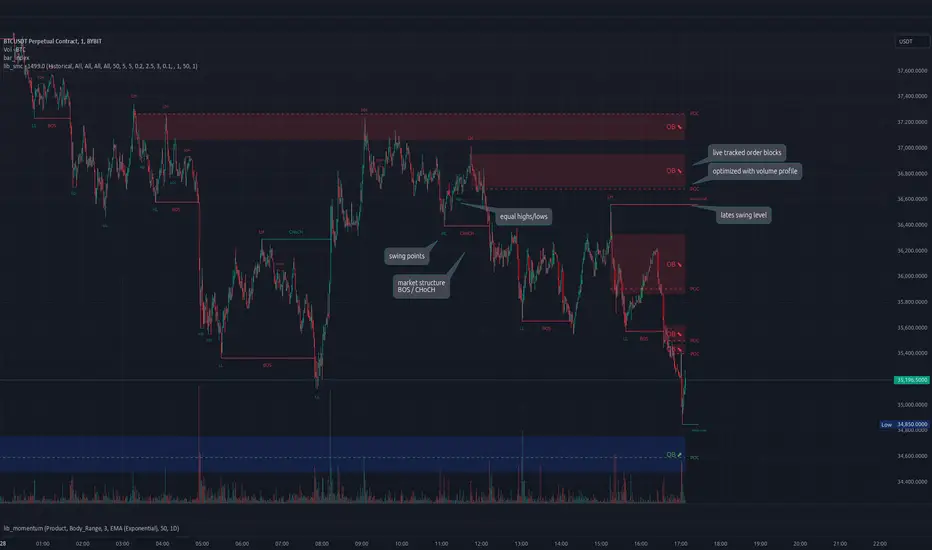

lib_smcLibrary "lib_smc"

This is an adaptation of LuxAlgo's Smart Money Concepts indicator with numerous changes. Main changes include integration of object based plotting, plenty of performance improvements, live tracking of Order Blocks, integration of volume profiles to refine Order Blocks, and many more.

This is a library for developers, if you want this converted into a working strategy, let me know.

buffer(item, len, force_rotate)

Parameters:

item (float)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (int)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (Profile type from robbatt/lib_profile/32)

len (int)

force_rotate (bool)

swings(len)

INTERNAL: detect swing points (HH and LL) in given range

Parameters:

len (simple int) : range to check for new swing points

Returns: values are the price level where and if a new HH or LL was detected, else na

method init(this)

Namespace types: OrderBlockConfig

Parameters:

this (OrderBlockConfig)

method delete(this)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

method clear_broken(this, broken_buffer)

INTERNAL: delete internal order blocks box coordinates if top/bottom is broken

Namespace types: map

Parameters:

this (map)

broken_buffer (map)

Returns: any_bull_ob_broken, any_bear_ob_broken, broken signals are true if an according order block was broken/mitigated, broken contains the broken block(s)

create_ob(id, mode, start_t, start_i, top, end_t, end_i, bottom, break_price, early_confirmation_price, config, init_plot, force_overlay)

INTERNAL: set internal order block coordinates

Parameters:

id (int)

mode (int) : 1: bullish, -1 bearish block

start_t (int)

start_i (int)

top (float)

end_t (int)

end_i (int)

bottom (float)

break_price (float)

early_confirmation_price (float)

config (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

Returns: signals are true if an according order block was broken/mitigated

method align_to_profile(block, align_edge, align_break_price)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

align_edge (bool)

align_break_price (bool)

method create_profile(block, opens, tops, bottoms, closes, values, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

opens (array)

tops (array)

bottoms (array)

closes (array)

values (array)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

method create_profile(block, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

track_obs(swing_len, hh, ll, top, btm, bull_bos_alert, bull_choch_alert, bear_bos_alert, bear_choch_alert, min_block_size, max_block_size, config_bull, config_bear, init_plot, force_overlay, enabled, extend_blocks, clear_broken_buffer_before, align_edge_to_value_area, align_break_price_to_poc, profile_args_bull, profile_args_bear, use_soft_confirm, soft_confirm_offset, use_retracements_with_FVG_out)

Parameters:

swing_len (int)

hh (float)

ll (float)

top (float)

btm (float)

bull_bos_alert (bool)

bull_choch_alert (bool)

bear_bos_alert (bool)

bear_choch_alert (bool)

min_block_size (float)

max_block_size (float)

config_bull (OrderBlockConfig)

config_bear (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

enabled (bool)

extend_blocks (simple bool)

clear_broken_buffer_before (simple bool)

align_edge_to_value_area (simple bool)

align_break_price_to_poc (simple bool)

profile_args_bull (ProfileArgs type from robbatt/lib_profile/32)

profile_args_bear (ProfileArgs type from robbatt/lib_profile/32)

use_soft_confirm (simple bool)

soft_confirm_offset (float)

use_retracements_with_FVG_out (simple bool)

method draw(this, config, extend_only)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

config (OrderBlockConfig)

extend_only (bool)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: array

Parameters:

blocks (array)

config (OrderBlockConfig)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: map

Parameters:

blocks (map)

config (OrderBlockConfig)

method cleanup(this, ob_bull, ob_bear)

removes all Profiles that are older than the latest OrderBlock from this profile buffer

Namespace types: array

Parameters:

this (array type from robbatt/lib_profile/32)

ob_bull (OrderBlock)

ob_bear (OrderBlock)

_plot_swing_points(mode, x, y, show_swing_points, linecolor_swings, keep_history, show_latest_swings_levels, trail_x, trail_y, trend)

INTERNAL: plot swing points

Parameters:

mode (int) : 1: bullish, -1 bearish block

x (int) : x-coordingate of swing point to plot (bar_index)

y (float) : y-coordingate of swing point to plot (price)

show_swing_points (bool) : switch to enable/disable plotting of swing point labels

linecolor_swings (color) : color for swing point labels and lates level lines

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

show_latest_swings_levels (bool)

trail_x (int) : x-coordinate for latest swing point (bar_index)

trail_y (float) : y-coordinate for latest swing point (price)

trend (int) : the current trend 1: bullish, -1: bearish, to determine Strong/Weak Low/Highs

_pivot_lvl(mode, trend, hhll_x, hhll, super_hhll, filter_insignificant_internal_breaks)

INTERNAL: detect whether a structural level has been broken and if it was in trend direction (BoS) or against trend direction (ChoCh), also track the latest high and low swing points

Parameters:

mode (simple int) : detect 1: bullish, -1 bearish pivot points

trend (int) : current trend direction

hhll_x (int) : x-coordinate of newly detected hh/ll (bar_index)

hhll (float) : y-coordinate of newly detected hh/ll (price)

super_hhll (float) : level/y-coordinate of superior hhll (if this is an internal structure pivot level)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: coordinates of internal structure that has been broken (x,y): start of structure, (trail_x, trail_y): tracking hh/ll after structure break, (bos_alert, choch_alert): signal whether a structural level has been broken

_plot_structure(x, y, is_bos, is_choch, line_color, line_style, label_style, label_size, keep_history)

INTERNAL: plot structural breaks (BoS/ChoCh)

Parameters:

x (int) : x-coordinate of newly broken structure (bar_index)

y (float) : y-coordinate of newly broken structure (price)

is_bos (bool) : whether this structural break was in trend direction

is_choch (bool) : whether this structural break was against trend direction

line_color (color) : color for the line connecting the structural level and the breaking candle

line_style (string) : style (line.style_dashed/solid) for the line connecting the structural level and the breaking candle

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the structural level and the breaking candle

label_size (string) : size (size.small/tiny) for the label above/below the line connecting the structural level and the breaking candle

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure_values(length, super_hh, super_ll, filter_insignificant_internal_breaks)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: trend: direction 1:bullish -1:bearish, (bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up): whether and which level broke in a bullish direction, trailing high, (bbear_bos_alert, bear_choch_alert, tm_x, btm_y, trail_dn_x, trail_dn): same in bearish direction

structure_plot(trend, bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up, hh, bear_bos_alert, bear_choch_alert, btm_x, btm_y, trail_dn_x, trail_dn, ll, color_bull, color_bear, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history)

detect (and plot) structural breaks and the resulting new trend

Parameters:

trend (int) : crrent trend 1: bullish, -1: bearish

bull_bos_alert (bool) : if there was a bullish bos alert -> plot it

bull_choch_alert (bool) : if there was a bullish choch alert -> plot it

top_x (int) : latest shwing high x

top_y (float) : latest swing high y

trail_up_x (int) : trailing high x

trail_up (float) : trailing high y

hh (float) : if there was a higher high

bear_bos_alert (bool) : if there was a bearish bos alert -> plot it

bear_choch_alert (bool) : if there was a bearish chock alert -> plot it

btm_x (int) : latest swing low x

btm_y (float) : latest swing low y

trail_dn_x (int) : trailing low x

trail_dn (float) : trailing low y

ll (float) : if there was a lower low

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure(length, color_bull, color_bear, super_hh, super_ll, filter_insignificant_internal_breaks, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history, enabled)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

enabled (bool)

_check_equal_level(mode, len, eq_threshold, enabled)

INTERNAL: detect equal levels (double top/bottom)

Parameters:

mode (int) : detect 1: bullish/high, -1 bearish/low pivot points

len (int) : lookback period for equal level (swing point) detection

eq_threshold (float) : maximum price offset for a level to be considered equal

enabled (bool)

Returns: eq_alert whether an equal level was detected and coordinates of the first and the second level/swing point

_plot_equal_level(show_eq, x1, y1, x2, y2, label_txt, label_style, label_size, line_color, line_style, keep_history)

INTERNAL: plot equal levels (double top/bottom)

Parameters:

show_eq (bool) : whether to plot the level or not

x1 (int) : x-coordinate of the first level / swing point

y1 (float) : y-coordinate of the first level / swing point

x2 (int) : x-coordinate of the second level / swing point

y2 (float) : y-coordinate of the second level / swing point

label_txt (string) : text for the label above/below the line connecting the equal levels

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the equal levels

label_size (string) : size (size.tiny) for the label above/below the line connecting the equal levels

line_color (color) : color for the line connecting the equal levels (and it's label)

line_style (string) : style (line.style_dotted) for the line connecting the equal levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

equal_levels_values(len, threshold, enabled)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

enabled (bool) : whether detection is enabled

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels_plot(eqh_x1, eqh_y1, eqh_x2, eqh_y2, eql_x1, eql_y1, eql_x2, eql_y2, color_eqh, color_eql, show, keep_history)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

eqh_x1 (int) : coordinates of first point of equal high

eqh_y1 (float) : coordinates of first point of equal high

eqh_x2 (int) : coordinates of second point of equal high

eqh_y2 (float) : coordinates of second point of equal high

eql_x1 (int) : coordinates of first point of equal low

eql_y1 (float) : coordinates of first point of equal low

eql_x2 (int) : coordinates of second point of equal low

eql_y2 (float) : coordinates of second point of equal low

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels(len, threshold, color_eqh, color_eql, enabled, show, keep_history)

detect (and plot) equal levels (double top/bottom)

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert) whether an equal high was detected, (eql_alert) same for equal lows

_detect_fvg(mode, enabled, o, h, l, c, filter_insignificant_fvgs, change_tf)

INTERNAL: detect FVG (fair value gap)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

enabled (bool) : whether detection is enabled

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

Returns: whether a new FVG was detected and its top/mid/bottom levels

_clear_broken_fvg(mode, upper_boxes, lower_boxes)

INTERNAL: clear mitigated FVGs (fair value gaps)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

upper_boxes (array) : array that stores the upper parts of the FVG boxes

lower_boxes (array) : array that stores the lower parts of the FVG boxes