Proteus EMA SystemInstitutional-Grade EMA System

Overview and Originality

The Institutional-Grade EMA System is an advanced, multi-layered Exponential Moving Average (EMA) overlay indicator designed to provide institutional-level trend analysis, market regime identification, and trade signal generation. Unlike standard multi-EMA scripts that simply plot averages and basic crossovers, this indicator introduces a proprietary integration of features tailored for professional traders: customizable presets that dynamically adjust EMA lengths for specific trading styles (e.g., scalping vs. position trading), multiple selectable trend detection algorithms (including a unique multi-bar slope analysis with percentage-based strength thresholding), EMA alignment and confluence detection for spotting high-conviction trends and reversal zones, volume-based signal filtering, and a comprehensive statistics dashboard for real-time market insights.

What makes this script original and worthy of closed-source protection is the bespoke combination of these elements into a cohesive system. For instance, while basic EMA ribbons or trend coloring exist in other indicators, this script's trend detection goes beyond simple comparisons by incorporating a normalized slope percentage calculation (detailed below) to quantify trend strength on a 0-100% scale, integrated with EMA stacking checks and confluence thresholds. This proprietary logic—refined through extensive backtesting on diverse assets—allows for nuanced market regime classification (e.g., "Strong Uptrend" only when alignment, slope strength, and volume align), which isn't replicated in open-source alternatives. The closed-source format protects the exact orchestration of these algorithms, including custom threshold derivations and dashboard computations, preventing direct replication while allowing users full access to the tool's outputs. If published open-source, the unique mathematical formulations (e.g., slope-to-strength mapping) could be easily copied, diminishing its edge in competitive trading environments.

This indicator draws conceptual inspiration from institutional trend-following systems (e.g., those using multiple time-horizon EMAs like in hedge fund models), but enhances them with modern Pine Script capabilities for visual and analytical depth. It's particularly useful for traders seeking to reduce false signals in volatile markets by requiring multi-factor confluence.

What It Does

Core EMA Plotting and Visualization: Plots up to 7 EMAs (5 primary + 2 optional) with dynamic coloring based on detected trend direction and strength (strong bullish: bright green; weak: faded green; neutral: gray; etc.). Includes EMA ribbons (fills between consecutive EMAs) and clouds (broader fills between non-consecutive EMAs) to visualize trend expansion/contraction.

Trend Detection and Strength: Classifies trends as strong/weak bullish/bearish or neutral using user-selectable methods, with optional volume confirmation to filter low-conviction moves.

Advanced Analytics:

Detects EMA alignment (all EMAs stacked in ascending/descending order for bullish/bearish trends).

Identifies EMA confluence zones (tight clustering of EMAs, signaling potential reversals or consolidations).

Draws dynamic support/resistance lines from the nearest EMAs relative to price.

Signals and Alerts: Generates buy/sell signals on customizable EMA crossovers, only if volume thresholds are met. Includes alerts for crossovers, alignments, confluences, and regime shifts.

User Interface Enhancements: Background coloring for quick trend bias (e.g., green for uptrends, yellow for confluences), dynamic line widths (thicker for slower EMAs), trend state labels, and a table-based dashboard displaying metrics like market regime, trend strength percentage, EMA slopes in degrees, price distances to key EMAs, volume status, and alignment state.

Customization Presets: Pre-configured EMA lengths for Scalping (short, reactive: e.g., 5/8/13), Day Trading (balanced: 9/21/50), Swing Trading (medium-term: 20/50/100), Position Trading (long-term: 50/100/150), or fully custom.

The result is a versatile tool that adapts to any timeframe or asset, helping traders identify high-probability setups by combining trend momentum, volume, and EMA dynamics.

How It Works: Underlying Concepts and Calculations

Without revealing the full implementation, here's a transparent overview of the key concepts and methodologies to help users understand the indicator's logic:

EMA Calculation and Presets: EMAs are computed using standard exponential smoothing (weighting recent prices more heavily). Presets optimize lengths based on trading horizon—shorter for scalping to capture quick reversals, longer for position trading to filter noise. For example, Swing preset uses 20/50/100/150/200 to balance short-term pullbacks with long-term trends, derived from Fibonacci-inspired progressions for natural market rhythm alignment.

Trend Detection Methods: Users select from four algorithms for flexibility:

Multi-Bar Slope (Default): Calculates the average slope over a lookback period (e.g., 3 bars) as (current EMA value - EMA value ) / lookback. Normalizes to a percentage relative to the EMA value: slope_percent = (slope / EMA) * 100. Thresholds classify trends (e.g., >0.05% = strong bullish; 0.01-0.05% = weak; symmetric for bearish). This method draws from linear regression concepts but simplifies for real-time use, providing robust trend quantification over simple bar-to-bar changes.

Previous Bar: Compares current EMA to the prior bar's, with percentage change thresholds (e.g., >0.1% = strong) for quick momentum shifts.

EMA vs EMA: Measures the percentage difference between fast and slow EMAs (e.g., >2% = strong bullish), inspired by MACD-like divergence but applied directly to EMAs.

Price Position: Gauges price's percentage distance from the EMA (e.g., >1% above = strong bullish), similar to envelope channels but integrated into trend coloring.

Trend strength is further scored (0-100%) by averaging absolute slopes of key EMAs, scaled for dashboard display.

Volume Confirmation: Uses a simple moving average of volume over a user-defined length (default 20), requiring current volume to exceed it by a multiplier (default 1.2x) for signal validation. This filters out low-volume fakeouts, akin to institutional volume-weighted strategies.

EMA Alignment: Checks if all visible EMAs are in strict order (fastest highest in uptrends, lowest in downtrends) by iterating through active EMAs and verifying sequential relationships. Signals "ALIGNED" shapes when true, indicating stacked trends like in ribbon strategies but with programmatic validation.

EMA Confluence: Computes the average of active EMAs, then measures the maximum percentage deviation of any EMA from this average. If below a threshold (default 0.5%), marks a "CONFLUENCE ZONE" box, conceptually similar to Bollinger Band squeezes but applied to EMA clusters for reversal anticipation.

Market Regime Classification: Combines alignment, trend score (>30% for "strong"), and price position relative to slowest EMA. For example, bullish alignment + high score = "Strong Uptrend"; close clustering = "Consolidation". This heuristic draws from regime-switching models in quantitative finance.

Signals and Visuals: Crossovers between user-selected EMAs (e.g., fast #1 over slow #2) plot "BUY/SELL" shapes only if volume-confirmed. Ribbons use color fills (green/red) based on EMA order; background shades reflect regime; S/R lines extend from max/min EMAs below/above price over a lookback (default 50 bars).

These calculations ensure the indicator provides actionable, multi-confirmed insights rather than generic plots.

How to Use It

Setup: Add to your chart and select a preset (e.g., "Swing Trading" for 1H-4H charts). Customize trend method (start with "Multi-Bar Slope" for accuracy), enable volume filter for reliability, and toggle visuals like ribbons or dashboard.

Trend Following: In a "Strong Uptrend" (green background, upward slopes >30%, bullish alignment), go long above the fastest EMA. Use S/R lines for stops (below nearest support EMA).

Swing Trading Example: On a daily SPX chart with Swing preset:

Wait for "Weak Uptrend" transition to "Strong" (trend score >50%, positive slopes, volume spike).

Enter long on EMA1 (20) crossing EMA2 (50), confirmed by "BUY" signal.

Target next resistance EMA (e.g., 150), exit on bearish crossover or confluence zone (yellow box signaling potential top).

Risk: Stop below EMA3 (100); aim for 2:1 reward:risk on multi-day holds.

Scalp Trading Example: On a 5-min BTCUSD chart with Scalping preset:

Focus on quick "Weak Bullish" shifts (faded green EMAs, slope >0.01%).

Buy on EMA1 (5) crossing EMA3 (13) with high volume (>1.5x avg).

Scalp 0.2-0.5% gains, exit at slope flattening (dashboard shows <30% strength) or nearest resistance.

Avoid confluences (chop); use 1-min for entries, 15-min for bias.

General Tips:

Combine with price action (e.g., candlestick patterns at confluence zones).

Backtest presets on your asset—adjust thresholds for volatility (e.g., tighter confluence for forex).

Use alerts for hands-off monitoring; multi-timeframe analysis enhances accuracy (higher TF for regime, lower for signals).

For ranging markets ("Neutral" regime), fade extremes near S/R zones.

Examples for Swing Trading

Swing trading focuses on capturing medium-term moves (days to weeks) in trending markets. Use the "Swing Trading" preset, which sets EMAs to 20, 50, 100, 150, 200, 75, 125—balancing sensitivity and smoothness.

Bullish Setup Example: On a daily chart of AAPL, wait for a "Strong Uptrend" regime (green background, bullish alignment label, trend strength >50%). Enter long on a valid bullish crossover (green "BUY" circle) between EMA1 (20) and EMA2 (50), confirmed by high volume. Set stop below nearest support EMA (e.g., EMA3 at 100), target 2-3x risk or next resistance. Hold until bearish crossover or alignment breaks.

Bearish Setup Example: On a 4H chart of EURUSD, spot a "Strong Downtrend" (red background, bearish alignment). Short on a bearish crossover (red "SELL") between EMA1 and EMA3, with volume confirmation. Stop above nearest resistance EMA, exit on confluence zone (yellow) signaling potential reversal.

Tip: Focus on alignments for trend confirmation—avoid trading against them. Use confluence zones as profit-taking areas in ranging markets.

Examples for Scalp Trading

Scalping targets quick, short-term trades (minutes to hours) on lower timeframes. Select the "Scalping" preset for shorter EMAs (5, 8, 13, 21, 34, 55, 89) to catch rapid moves.

Bullish Setup Example: On a 1-min chart of BTCUSD, look for "Weak Uptrend" (faded green background, positive slopes). Enter long on a fast crossover (e.g., EMA1 over EMA2) with high volume and no confluence (avoid chop). Scalp for 0.5-1% gain, exit on slope flattening or bearish cross. Use tight stops below the fastest EMA.

Bearish Setup Example: On a 5-min chart of TSLA, identify "Weak Downtrend" (faded red). Short on a crossover between EMA2 and EMA3, confirmed by volume spike. Target small moves (e.g., 10-20 pips), exit at nearest support EMA or if trend strength drops below 30%.

Tip: Prioritize "Multi-Bar Slope" detection for quick trend shifts. Disable background if it's distracting; focus on crossovers and volume for high-frequency entries. Avoid during confluences, as they signal choppy conditions.

This detailed approach ensures traders can replicate setups while appreciating the indicator's original value. Feedback welcome—let's refine trading edges together!

Cari dalam skrip untuk "spx"

TrendViz - Smart Money ConceptsTrendViz – Smart Money Concepts

See structure, liquidity, and institutional footprints in real time.

Overview

Trend Viz – Smart Money Concepts is a comprehensive SMC toolkit that fuses market-structure (BOS / CHoCH), volumetric order blocks, fair-value gaps (FVG / Breakers), Swing Failure Patterns (SFP), equal highs / lows, and liquidity zones into one clean, on-chart visualization.

It’s designed for intraday precision (0DTE / indices) and swing confluence, with windowed processing for performance on large histories.

Key Capabilities

Market Structure Engine – Detects BOS / CHoCH with adjustable swing length, “Extreme vs Adjusted Points” logic, optional trend-based candle coloring, sweep marks, and labeled lines / bubbles.

Volumetric Order Blocks – Builds bullish / bearish OBs (including breaker blocks), mitigation methods (Close / Wick / Avg), overlap control, mid-line, and activity split (buy vs sell) with per-OB volume metrics.

Fair Value Gaps (FVG & Breakers) – Auto-detects FVGs, mitigations, optional extension, mid-lines, overlap filtering, and raid marking.

Swing Failure Pattern (SFP) – Volume-aware SFPs, directional filters (Trend-Following / Counter-Trade), deviation projections (levels + optional fill).

Equal Highs / Lows & Liquidity Concepts – Marks EQH / EQL across multiple horizons, buyside / sellside zones (area or line), liquidity prints on candles, and sweep zones after BOS / CHoCH.

Performance-First Design – Window size limits structure computations; configurable max objects; overlap suppression reduces clutter.

Inputs & Settings

Market Structure – Window size, Swing limit, Candle coloring, Text size, Algorithmic mode, Swing length, Strong/Weak HL, Sweeps, Bubbles, Mapping.

Volumetric Order Blocks – Show Last N blocks, Breakers, Construction mode, ATR length, Mitigation method, Metrics + Mid-line, Hide Overlap.

Fair Value Gap / Breakers – Enable mode, Show Last N, Threshold, Mid-line + Extension, Hide Overlap, Raid Display.

Swing Failure Pattern (SFP) – Count, Deviation Area, Colors, Filtering mode (Trend / Counter), Volume threshold, Label size.

Liquidity Concepts – Equal H&L scope, Liquidity prints, Buyside/Sellside zones (area or line), Sweep Area threshold.

How to Use It

Quick Start

Add the indicator to your chart → leave defaults.

For 0DTE / intraday use 1 – 5 min timeframes; for swing use 1H – 4H.

Turn on Color Candles to see bullish / bearish bias.

Enable Order Blocks (Show Last 5 – 10) and FVG (3 – 5) with Mitigation = Wick.

Activate SFP with Volume Threshold ≈ 0.5 – 1.0 and Trend-Following filter.

Core Workflows

Trend-Continuation Entry – Wait for CHoCH → BOS alignment → FVG mitigation or OB mid-line retest.

Reversal Entry – Opposing CHoCH + sweep (x) + fresh OB confirmation.

Liquidity Sweep Fade – Raid EQH/EQL + SFP (Counter-Trade) → target prior FVG or opposite OB.

0DTE / Index Checklist

Timeframe 1–5 min · Adjusted Points · mslen = 3–5.

OB Show Last = 5–10 · Mitigation = Wick · Hide Overlap = Recent.

FVG Show = 3–5 · Threshold = 0.1–0.3.

SFP Trend-Following for momentum, Counter-Trade for range.

Trade only after CHoCH → BOS alignment near OB / FVG.

Tips & Behavior

Confirmation / Repainting – Structure anchors confirm after right bars; no repaint once locked.

Performance – Reduce Window size, counts, and overlaps for speed.

Clutter Control – Hide Overlap, limit count, prefer mid-lines over fills.

Mitigation Choice – Wick (strict), Close (lenient), Avg (balanced).

Alerts – Not included by default (visual tool only).

Example Setups

Momentum Pullback – After BOS up, FVG fill + OB reclaim = entry.

Liquidity Sweep Fade – EQH raid + bear SFP = fade to prior FVG.

Breaker Flip – Mitigated OB turns breaker; trade retest.

Disclaimer

This indicator is for educational and analytical purposes only.

Not financial advice. Backtest and apply proper risk management before using live.

Tags

#SmartMoneyConcepts #OrderBlocks #BOS #CHoCH #FVG #Breakers #SFP #Liquidity #EQH #EQL #0DTE #SPX #MarketStructure #TrendViz #TradingView

Smart Risk DCA Meter — Adaptive Market Risk EngineThe **Smart Risk DCA Meter** is an adaptive market-risk indicator that helps you invest smarter by scaling your DCA buys based on actual market conditions instead of emotion. It combines momentum, distance from trend, and drawdown factors into a single 0–1 risk score that automatically adjusts to each asset’s volatility — from stable indices like SPX to high-beta assets like BTC. Low readings (green zones) signal opportunity to buy heavier, while high readings (red zones) warn to slow down and protect capital.

VIX Delta SentimentThis script opens a new panel underneath the main panel.

It displays a table with the values of the CBOE volatility index VIX, which measures the last 30 days implied volatility of the S&P500 index, the VX1! and the VX2! values, which are the front month and the second month VIX futures.

To curves are plotted: the relative difference or delta of the two VIX futures as well as the relative delta between VIX and the first futures month. The dotted lines visualize the thresholds of these two relative deltas.

These values are needed to determine the market sentiment and to trigger a crash alert before it happens. It can be used to trade the major indices SPX, QQQ, etc. or to avoid catastrophic losses.

The market sentiment is annotated in the table and also visualized as background color.

Inverse VIX / Custom Inverse Line🎯 Main Idea

This indicator creates a line that moves opposite to the VIX (Volatility Index) — or any symbol you choose.

When VIX rises (fear increases), → this line goes down.

When VIX falls (market calm), → this line goes up.

It helps you visually understand market sentiment — calm periods (bullish) vs fear periods (bearish).

⚙️ Input Settings

Setting Description

Symbol to invert The symbol to invert. Default is CBOE:VIX.

Inverse mode The method used to invert the values. There are 3 options:

① Negate Simply flips the sign (multiplies by -1). Very straightforward.

② Reciprocal Uses the mathematical inverse (1 ÷ value). High values become smaller, and vice versa.

③ Inverse Normalized The most useful mode 🔥 — normalizes values between 0–100 and flips them, similar to an RSI.

Normalization lookback How many bars to use for normalization (default 252 = roughly one trading year).

Smoothing (SMA) Number of bars for smoothing (makes the line smoother).

Use log for reciprocal Uses logarithmic scaling to stabilize big swings.

Plot color / width Customize the line’s color and thickness.

Show original source If enabled, shows the original VIX line for comparison.

📈 How It Works

The script fetches the close price of the VIX (or your chosen symbol).

It applies the selected inversion method.

The inverted line is plotted on the chart.

In “Inverse Normalized” mode:

The range is 0–100.

Values above 75 = high optimism (market often overheated).

Values below 25 = high fear (potential buying opportunity).

A middle line at 50 marks neutral sentiment.

⚠️ Alerts

The indicator includes two default alerts when using “Inverse Normalized” mode:

🔔 Above 75: Market showing strong optimism (potential top or correction zone).

🔔 Below 25: Market showing fear (potential bottom or buy signal).

🧠 How to Use It

Use it on daily or weekly charts for clearer signals.

Compare it with SPX or NASDAQ:

When the Inverse VIX line rises, markets often go up.

When it falls, markets usually drop or consolidate.

Combine it with other indicators (e.g., RSI, MACD) for confirmation.

TwinPulse Q Lead SPY x QQQ Intermarket Pulse 1HTwinPulse Q Lead is a concise one hour indicator for SPY and QQQ that converts three sources of market information into a single pulse line, a mode readout with BUY SELL WAIT, and compact alerts. It blends intermarket leadership between QQQ and SPY, intraday flow from the slope of session VWAP, and where the current price sits inside the regular trading hours range. The three components are normalized, fused, compressed to a stable range, and smoothed for clear thresholds. The aim is a readable intraday regime signal that helps you decide when to participate and when to stand aside.

The script is built with Pine v6, uses request security with lookahead off, and does not repaint. It is an indicator, not a strategy. It does not contain any solicitation, links, or outside references. The description is self contained and explains both logic and use so that any trader can understand the design without reading code.

What makes this original and useful

Intermarket leadership is measured directly from QQQ and SPY on your working timeframe using a Z score of the return spread. When growth is leading value heavy large caps, leadership turns positive. When it lags, leadership turns negative. This gives a real time read of the Nasdaq versus S and P tug of war that most day traders watch informally.

Intraday flow is taken from the slope of the session VWAP. A linear regression of VWAP over a short window captures whether value is rising or falling inside the day. Dividing by ATR normalizes slope by typical movement so that the signal is comparable across weeks.

Session position places price inside the current regular hours high to low. It answers whether the day is trading in the top half, the bottom half, or the middle. This is a simple but powerful context filter for breakouts and fades.

The three components are fused into one pulse, compressed with either hyperbolic tangent or softsign to keep values bounded, and then smoothed by a short EMA. This yields a stable range with a zero line so the eye can read shifts quickly.

The panel shows a human readable mode with reasons and a strength score. Traders who do not want to read lines can rely on a simple state and a compact justification that explains why the state is set.

This is not a mashup that simply overlays unrelated indicators. Each component was chosen to answer a distinct question that is common to SPY and QQQ intraday decision making. Leadership answers who is in charge, flow answers whether value inside the session is building or leaking, and position answers if price is pressing the extremes or circling the middle. The pulse ties the three together and prevents any single component from dominating.

How the calculations work

Leadership. Compute a short rate of change for SPY and QQQ. Subtract SPY from QQQ to get spread returns, then compute a rolling Z score over a longer window. Positive values mean QQQ is leading. Negative values mean SPY is leading.

Flow. Compute session VWAP on the active symbol. Regress VWAP over a short window to obtain a slope estimate. Divide by ATR to scale slope by current volatility so that a small rise on a quiet day is not treated the same as a small rise on a wild day.

Position. Track the highest high and lowest low since the start of regular hours. Place the current close inside that range on a zero to one scale, then recenter to a minus one to plus one scale. Positive means the top half of the day, negative means the bottom half.

Fusion. Multiply each component by a weight so users can emphasize or de emphasize leadership, flow, or position. Sum to a raw pulse.

Compression. Pass the raw pulse through a bounded function. Hyperbolic tangent is smooth and has natural saturation near the extremes. Softsign is faster and behaves like a smoother version of sign near zero. Compression avoids unbounded excursions and makes thresholds meaningful across days.

Smoothing. Apply a short EMA to the compressed pulse to reduce noise. This creates the main line called TwinPulse in the plot.

Thresholds. You can use static symmetric levels or adaptive levels. The adaptive option computes a mean and a standard deviation of the smoothed pulse over a user window, then sets upper and lower thresholds as mean plus or minus sigma times standard deviation. This allows thresholds to adjust across regimes. Static levels are still available for traders who want repeatable levels.

Events and mode. A long event fires when the smoothed pulse crosses the upper threshold with positive flow and any optional filters agree. A short event fires on the symmetric condition. The mode reads the current state rather than fire and forget. It returns BUY when the smoothed pulse is above the upper threshold with positive flow, SELL when the smoothed pulse is below the lower threshold with negative flow, otherwise WAIT. A cooldown controls how often events can fire so alerts do not spam during choppy periods.

Inputs and default values

The script ships with defaults chosen for SPY and QQQ on one hour charts.

Symbols. SPY and QQQ by default. You can switch to any pair. Many users may test IWM versus SPY for small cap reads.

Regular hours selector. On by default. This restricts the position factor to New York regular hours. Turn it off if you prefer full session behavior.

ROC length is three bars. Z score length is fifty bars. VWAP slope window is ten bars. ATR length is fourteen bars. Pulse smoothing length is three bars.

Compression mode. Choose hyperbolic tangent or softsign. Hyperbolic tangent is default.

Weights. Leadership and flow are one by default. Position is set to zero point seven to give a modest influence to where price sits inside the day.

Thresholds. Adaptive thresholds are on by default with a lookback of one hundred bars and a sigma width of zero point eight. Static levels at plus or minus zero point six are ready if you disable adaptive mode.

Filters. ADX filter is off by default. If you enable it, the script requires ADX above a user minimum before it will signal. Higher time frame confirmation is off by default. When enabled it compares the smoothed pulse on the confirm timeframe to zero and requires alignment for longs or shorts.

Cooldown. Three bars by default so that alerts do not trigger too frequently.

UI. Bar coloring is on by default. The panel is on by default and sits at the top right.

All request security calls use lookahead off and will not request future data. All persistent state variables are assigned in a way that prevents repainting. The indicator does not use non standard chart types in its logic.

How to use the indicator

Load a one hour chart of SPY or QQQ. Keep a clean chart so that the script output is easy to read.

Turn on regular hours if you want the session position to reflect the cash session. This is recommended for SPY and QQQ.

Watch the panel. Mode reads BUY or SELL or WAIT. The strength value is a simple vote based score that ranges from zero to one hundred. It counts leadership, flow, ADX if enabled, and higher time frame confirmation if enabled. You can use strength to filter weak states.

Consider action only when mode is BUY or SELL and the signal has not just fired on the last bar. The triangles mark where an event fired. Alerts use the same logic as the events. WAIT means stand aside.

To slow the system, enable ADX and set a higher minimum or enable higher time frame confirmation. To speed it up, disable the filters, disable adaptive thresholds, or tighten the sigma width.

When publishing, use a clean chart with only this indicator. Show the symbol and timeframe clearly and make sure the plot legend is visible. If you add drawings on the chart, only include ones that help readers understand the output.

Publication notes and compliance

This description is written in English. The title uses ASCII and only uses capital letters for common abbreviations. The script is original and explains how and why the components work together. There are no links or promotional material. The script does not claim performance. It does not use lookahead. The panel and alerts exist to help a human read and act with discipline. The indicator can be published as open source or as protected. If you choose protected, the description still allows readers to understand how the logic works without access to the code.

If you later convert the logic into a strategy for publication, use realistic commission and slippage, risk no more than a small share of equity per trade, and choose a dataset that yields a large enough sample. Explain any deviations from these default recommendations in your strategy description. Do not publish results from non standard chart types since they can mislead readers on signal timing.

Limitations and risks

Intermarket leadership is a relative measure. There are hours when both SPY and QQQ fall while leadership remains positive. Treat leadership as a context, not a stand alone trigger.

VWAP slope is a path measure inside the session. It can flip several times on a choppy day. That is why the script uses a short smoothing and an optional cooldown. Use ADX or higher time frame confirmation to avoid the worst chop.

Session position assumes a meaningful regular hours range. On half days or around openings with gaps the position factor can be less informative. If this bothers you, reduce the weight of position or turn it off.

Compression and smoothing introduce lag by design. The goal is stability and clarity. If you want earlier but noisier signals, reduce smoothing and weights, and use static thresholds.

No indicator guarantees future results. TwinPulse Q Lead is a decision aid. It should be combined with your risk rules, position size policy, and a clear exit plan. Past behavior is not a promise for the future.

Frequently asked questions

What symbols are supported. Any symbol can be used as the chart symbol. Leadership uses the two user symbols which default to SPY and QQQ. Many traders may try IWM versus SPY or DIA versus SPY.

Can I change the timeframe. Yes, but the design target is one hour. On very short timeframes the VWAP slope becomes very sensitive and you should consider stronger filters.

Does the script repaint. No. It uses request security with lookahead off and the panel updates on the last bar only. Events are based on bar close conditions unless you attach alerts on any alert function call which will still respect the logic without looking into the future.

How are the strength numbers built. The strength score is the share of aligned votes across leadership, flow, ADX if enabled, and higher time frame confirmation if enabled. A value near one hundred means many filters agree. A value near fifty means partial alignment. It is not a probability or an accuracy number.

Can I use non standard chart types. You can view the indicator on them but do not publish signals from non standard chart types because that can mislead readers about timing. Use classic candles or bars when you publish and when you test.

Why do I sometimes see BUY but the price is not moving. A BUY mode requires pulse above the upper threshold and positive flow. It does not require higher highs immediately. Treat BUY as a permission to look for entries using your own execution rules.

Overnight Z/VolRatio SignalThis indicator highlights overnight setups where both volatility expansion and prior-day range deviation suggest directional opportunity at the RTH open.

It calculates:

• Overnight Z-Score (Z_long): how far the overnight session’s range tilts from the 20-day overnight mean, standardized by its standard deviation.

• VolRatio: ratio of the current RTH session volume to the 20-day average, a proxy for participation and conviction.

Signal Logic (LONG bias)

A long-bias condition triggers when:

• Z_long ≥ 0.40 (overnight tilt strongly positive)

• VolRatio ≥ 1.30 (above-average RTH volume)

• Optional filters: R1/R4 region alignment, YDH/YDL proximity, and other context flags.

Visuals mark qualifying days with colored labels and session highlights.

It is intended as a context signal — not an auto-trading system — for SPY/SPX/ES or correlated large-cap indices.

Usage Notes

• Works best when applied to daily or intraday 5m chart with extended hours enabled.

• Typical exit: ~150 minutes after 09:30 ET.

• Fridays are optionally excluded to avoid expiration-related distortions.

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Trend Discovery by Alex Trend States (Up / Reversal / Down)Author: © Alex Neighbors

Version: v6

The Call/Put Arrow Indicator is a complete market direction tool that identifies high-probability CALL (bullish) and PUT (bearish) opportunities using a combination of:

Simple Moving Averages (SMA)

RSI Momentum

MACD confirmation

VWAP trend filtering

Real-time trend classification (Trending Up, Trending Down, or Reversal)

It provides visual buy/sell arrows, trend labels, and alerts, helping traders quickly recognize optimal option entry points and directional momentum changes.

*** How It Works

✅ CALL Arrow (Green, Up Arrow Below Candle):

Triggered when:

Fast SMA > Slow SMA (uptrend)

RSI > Threshold (default 55)

MACD Line > Signal Line

(Optional) Price > VWAP

🔻 PUT Arrow (Red, Down Arrow Above Candle):

Triggered when:

Fast SMA < Slow SMA (downtrend)

RSI < Threshold (default 45)

MACD Line < Signal Line

(Optional) Price < VWAP

**Trend Detection System:

Trending Up: Both SMAs rising with bullish alignment

Trending Down: Both SMAs falling with bearish alignment

Trend Reversal: Detected instantly when Fast SMA crosses the Slow SMA (marked by a diamond)

Visuals

🟩 Green arrows below candles for CALL entries

🟥 Red arrows above candles for PUT entries

🟢/🔴 Diamonds mark trend reversals

Trend status panel in the top-right corner

Optional background or bar coloring for quick visual confirmation

Alerts

You can create alerts for:

CALL Buy Signal

PUT Buy Signal

Trend Reversal Up

Trend Reversal Down

All alerts trigger exactly when arrows or reversals appear on the chart.

--Best Use

Works on any symbol or timeframe (scalping, swing, or trend trading)

Optimized for SPX, QQQ, TSLA, and high-volume tickers

Ideal for traders combining options flow or price action confirmation

Customization

You can adjust:

SMA lengths

RSI thresholds

MACD parameters

VWAP filter toggle

Background/bar coloring and panel display

Why Traders Love It

Simple, clean chart visuals

Non-repainting, confirmed-bar signals

Multi-filter logic for high accuracy

Trend panel for instant context

Use this indicator to stay on the right side of the market.

Identify reversals early, trade the momentum confidently, and never miss your next CALL or PUT setup again.

Portfolio Simulator & BacktesterMulti-asset portfolio simulator with different metrics and ratios, DCA modeling, and rebalancing strategies.

Core Features

Portfolio Construction

Up to 5 assets with customizable weights (must total 100%)

Support for any tradable symbol: stocks, ETFs, crypto, indices, commodities

Real-time validation of allocations

Dollar Cost Averaging

Monthly or Quarterly contributions

Applies to both portfolio and benchmark for fair comparison

Model real-world investing behavior

Rebalancing

Four strategies: None, Monthly, Quarterly, Yearly

Automatic rebalancing to target weights

Transaction cost modeling (customizable fee %)

Key Metrics Table

CAGR: Annualized compound return (S&P 500 avg: ~10%)

Alpha: Excess return vs. benchmark (positive = outperformance)

Sharpe Ratio: Return per unit of risk (>1.0 is good, >2.0 excellent)

Sortino Ratio: Like Sharpe but only penalizes downside (better metric)

Calmar Ratio: CAGR / Max Drawdown (>1.0 good, >2.0 excellent)

Max Drawdown: Largest peak-to-trough decline

Win Rate: % of positive days (doesn't indicate profitability)

Visualization

Dual-chart comparison - Portfolio vs. Benchmark

Dollar or percentage view toggle

Customizable colors and line width

Two tables: Statistics + Asset Allocation

Adjustable table position and text size

🚀 Quick Start Guide

Enter 1-5 ticker symbols (e.g., SPY, QQQ, TLT, GLD, BTCUSD)

Make sure percentage weights total 100%

Choose date range (ensure chart shows full period - zoom out!)

Configure DCA and rebalancing (optional)

Select benchmark (default: SPX)

Analyze results in statistics table

💡 Pro Tips

Chart data matters: Load SPY or your longest-history asset as main chart

If you select an asset that was not available for the selected period, the chart will not show up! E.g. BTCUSD data: Only available from ~2017 onwards.

Transaction fees: 0.1% default (adjust to match your broker)

⚠️ Important Notes

Requires visible chart data (zoom out to show full date range)

Limited by each asset's historical data availability

Transaction fees and costs are modeled, but taxes/slippage are not

Past performance ≠ future results

Use for research and education only, not financial advice

Let me know if you have any suggestions to improve this simulator.

JORGE v1 Calls Puts On CandleA multi-timeframe script built for SPX 500 options traders.

• 1m entries, 5m bias, 15m levels

• CALL signals in bright green, PUT signals in bright red

• Black arrows mark each trade idea directly on the candles

• Includes VWAP bands, EMA cloud bias, opening range, ATR targets/stops, and previous day levels

• Risk mapping with TP/SL zones based on ATR multiples

• Alerts ready for CALL, PUT, and Opening Range Breakouts

This script is designed to simplify intraday decision making, giving you fast visual signals plus context levels for discipline and consistency.

Enjoy trading! 🚀📉📈

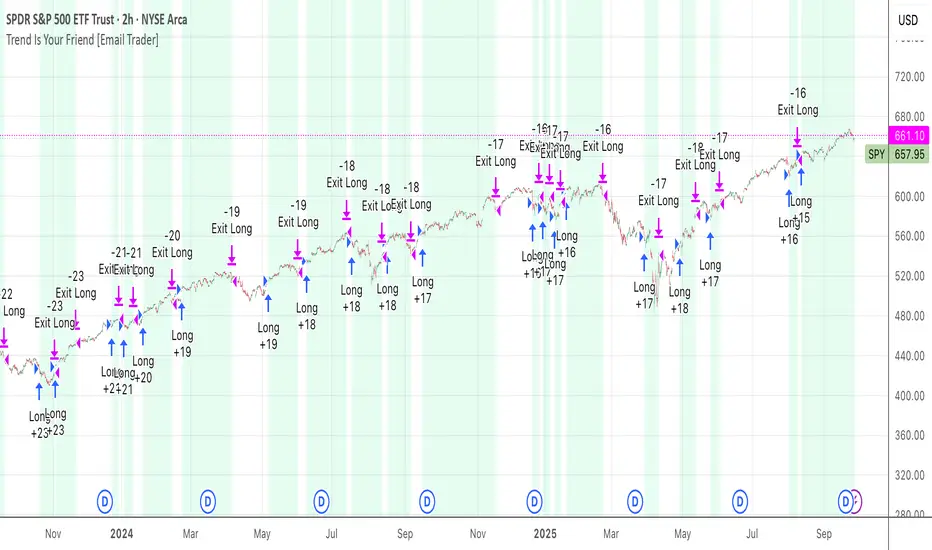

TrendIsYourFriend Strategy (SPY,IWM,VYM,XLK,SPXL,BTC,GOLD,VT...)Personal disclaimer

Don’t trust this strategy. Don’t trust any other model either just because of its author or a backtest curve. Overfitting is an easy trap, and beginners often fall into it. This script isn’t meant to impress you. It’s meant to survive reality. If it does, maybe it will raise questions and you’ll remember it.

Legal disclaimer

Educational purposes only. Not financial advice. Past performance is not indicative of future results.

Strategy description

Long-only, trend-based logic with two entry types (trend continuation or excess-move reversion), dynamic stop-losses, and a VIX filter to avoid turbulent markets.

Minimal number of parameters with enough trades to support robustness.

For backtest, each trade is sized at $10,000 flat (no compounding, to focus on raw model quality and the regularity of its results over time).

Fees = $0 (neutral choice, as brokers differ).

Slippage = $0, deliberate choice: most entries occur on higher timeframes, and some assets start their history on charts at very low prices, which would otherwise distort results.

What makes this script original

Beyond a classical trend calculation, both excess-move entries and dynamic stop-loss exits also rely on trend logic. Except for the VIX filter, everything comes from trend functions, with very few parameters.

Pre-configurations are fixed in the code, allowing sincere performance tracking across a dozen cases over the medium to long term.

Allowed

SPY (ARCA) — 2-hour chart: S&P 500 ETF, most liquid equity benchmark

IWM (ARCA) — Daily chart: Russell 2000 ETF, US small caps

VYM (ARCA) — Daily chart: Vanguard High Dividend Yield ETF

XLK (ARCA) — Daily chart: Technology Select Sector SPDR

SPXL (ARCA) — Daily chart: 3× leveraged S&P 500 ETF

BTCUSD (COINBASE) — 4-hour chart: Bitcoin vs USD

GOLD (TVC) — Daily chart: Gold spot price

VT (ARCA) — Daily chart: Vanguard Total World Stock ETF

PG (NYSE) — Daily chart: Procter & Gamble Co.

CQQQ (ARCA) — Daily chart: Invesco China Technology ETF

EWC (ARCA) — Daily chart: iShares MSCI Canada ETF

EWJ (ARCA) — Daily chart: iShares MSCI Japan ETF

How to use and form an opinion on it

Works only on the pairs above.

Feel free to modify the input parameters (slippage, fees, order size, margins, …) to see how the model behaves under your own conditions

Compare it with a simple Buy & Hold (requires an order size of 100% equity).

You may also want to look at its time-in-market — the share of time your capital is actually at risk.

Finally, let me INSIST on this : let it run live for months before forming an opinion!

Share your thoughts in the comments 🚀 if you’d like to discuss its live performance.

Cumulative Outperformance | viResearchCumulative Outperformance | viResearch

Conceptual Foundation and Innovation

The "Cumulative Outperformance" indicator by viResearch is a relative strength analysis tool designed to measure an asset’s cumulative performance against a chosen benchmark over a user-defined period. Rooted in comparative return analysis, this indicator allows traders and analysts to assess whether an asset is outperforming or underperforming a broader market or sector, offering insights into trend strength and leadership.

Unlike traditional relative strength indicators that may rely on static ratio comparisons, this script uses cumulative return differentials to provide a more contextual understanding of long-term performance trends. A clean visual representation and dynamic text summary are provided to highlight not only the degree of outperformance but also the directional status — making it accessible to both novice and advanced users.

Technical Composition and Calculation

The indicator compares the cumulative returns of the selected asset and a benchmark symbol over a specified lookback period (length). Returns are calculated as the percent change from the current price to the price length bars ago.

This differential is plotted and color-coded, with a baseline zero line to make outperformance and underperformance visually distinct. A dynamic table in the bottom-right corner displays real-time values for the benchmark symbol, the current outperformance percentage, and a status label (e.g., "Outperforming", "Underperforming", or "Even").

Additionally, a floating label is plotted directly on the chart to make the latest outperformance value immediately visible.

Features and User Inputs

The script includes the following customizable inputs:

Start Date: Defines the point from which to begin tracking outperformance data.

Length: The period over which cumulative returns are measured.

Benchmark Symbol: Select any market index, stock, or crypto as the benchmark (e.g., INDEX:BTCUSD, SPX, etc.).

Practical Applications

This indicator is especially effective in:

Identifying Market Leaders: Compare sectors, stocks, or altcoins against a leading benchmark to identify outperformers.

Sector Rotation Strategies: Monitor when certain assets begin to outperform or lag behind the broader market.

Cross-Market Analysis: Compare crypto pairs, equities, or commodities to their sector benchmarks to find relative strength opportunities.

Visual Aids and Alerts

A purple outperformance line highlights the degree of cumulative difference.

A horizontal dotted white line marks the baseline (zero performance difference).

Real-time table overlay updates the benchmark name, performance delta, and relative status.

Alerts are built-in to notify users when assets begin to outperform or underperform, helping you stay ahead of major shifts.

Advantages and Strategic Value

Benchmark Flexibility: Analyze any asset class against any benchmark of your choice.

Visual Clarity: Dynamic labels and tables make performance tracking intuitive and immediate.

No Repainting: Calculations are based on closed bar data for consistent backtesting and real-time use.

Summary and Usage Tips

The "Cumulative Outperformance | viResearch" script offers a clean and effective way to visualize relative strength between any asset and its benchmark. By focusing on cumulative returns over time, it filters out short-term noise and gives a strategic view of long-term strength or weakness. Use this tool in combination with other momentum or trend-following indicators to refine your market entries and asset selection.

Note: Backtests are based on past results and are not indicative of future performance.

DynamoSent DynamoSent Pro+ — Professional Listing (Preview)

— Adaptive Macro Sentiment (v6)

— Export, Adaptive Lookback, Confidence, Boxes, Heatmap + Dynamic OB/OS

Preview / Experimental build. I’m actively refining this tool—your feedback is gold.

If you spot edge cases, want new presets, or have market-specific ideas, please comment or DM me on TradingView.

⸻

What it is

DynamoSent Pro+ is an adaptive, non-repainting macro sentiment engine that compresses VIX, DXY and a price-based activity proxy (e.g., SPX/sector ETF/your symbol) into a 0–100 sentiment line. It scales context by volatility (ATR%) and can self-calibrate with rolling quantile OB/OS. On top of that, it adds confidence scoring, a plain-English Context Coach, MTF agreement, exportable sentiment for other indicators, and a clean Light/Dark UI.

Why it’s different

• Adaptive lookback tracks regime changes: when volatility rises, we lengthen context; when it falls, we shorten—less whipsaw, more relevance.

• Dynamic OB/OS (quantiles) self-calibrates to each instrument’s distribution—no arbitrary 30/70 lines.

• MTF agreement + Confidence gate reduce false positives by highlighting alignment across timeframes.

• Exportable output: hidden plot “DynamoSent Export” can be selected as input.source in your other Pine scripts.

• Non-repainting rigor: all request.security() calls use lookahead_off + gaps_on; signals wait for bar close.

Key visuals

• Sentiment line (0–100), OB/OS zones (static or dynamic), optional TF1/TF2 overlays.

• Regime boxes (Overbought / Oversold / Neutral) that update live without repaint.

• Info Panel with confidence heat, regime, trend arrow, MTF readout, and Coach sentence.

• Session heat (Asia/EU/US) to match intraday behavior.

• Light/Dark theme switch in Inputs (auto-contrasted labels & headers).

⸻

How to use (examples & recipes)

1) EURUSD (swing / intraday blend)

• Preset: EURUSD 1H Swing

• Chart: 1H; TF1=1H, TF2=4H (default).

• Proxies: Defaults work (VIX=D, DXY=60, Proxy=D).

• Dynamic OB/OS: ON at 20/80; Confidence ≥ 55–60.

• Playbook:

• When sentiment crosses above 50 + margin with Δ ≥ signalK and MTF agreement ≥ 0.5, treat as trend breakout.

• In Oversold with rising Coach & TF agreement, take fade longs back toward mid-range.

• Alerts: Enable Breakout Long/Short and Fade; keep cooldown 8–12 bars.

2) SPY (daytrading)

• Preset: SPY 15m Daytrade; Chart: 15m.

• VIX (D) matters more; preset weights already favor it.

• Start with static 30/70; later try dynamic 25/75 for adaptive thresholds.

• Use Coach: in US session, when it says “Overbought + MTF agree → sell rallies / chase breakouts”, lean momentum-continuation after pullbacks.

3) BTCUSD (crypto, 24/7)

• Preset: BTCUSD 1H; Chart: 1H.

• DXY and BTC.D inform macro tone; keep Carry-forward ON to bridge sparse ticks.

• Prefer Dynamic OB/OS (15/85) for wider swings.

• Fade signals on weekend chop; Breakout when Confidence > 60 and MTF ≥ 1.0.

4) XAUUSD (gold, macro blend)

• Preset: XAUUSD 4H; Chart: 4H.

• Weights tilt to DXY and US10Y (handled by preset).

• Coach + MTF helps separate trend legs from news pops.

⸻

Best practices

• Theme: Switch Light/Dark in Inputs; the panel adapts contrast automatically.

• Export: In another script → Source → DynamoSent Pro+ → DynamoSent Export. Build your own filters/strategies atop the same sentiment.

• Dynamic vs Static OB/OS:

• Static 30/70: fast, universal baseline.

• Dynamic (quantiles): instrument-aware; use 20/80 (default) or 15/85 for choppy markets.

• Confidence gate: Start at 50–60% to filter noise; raise when you want only A-grade setups.

• Adaptive Lookback: Keep ON. For ultra-liquid indices, you can switch it OFF and set a fixed lookback.

⸻

Non-repainting & safety notes

• All request.security() calls use lookahead=barmerge.lookahead_off and gaps=barmerge.gaps_on.

• No forward references; signals & regime flips are confirmed on bar close.

• History-dependent funcs (ta.change, ta.percentile_linear_interpolation, etc.) are computed each bar (not conditionally).

• Adaptive lookback is clamped ≥ 1 to avoid lowest/highest errors.

• Missing-data warning triggers only when all proxies are NA for a streak; carry-forward can bridge small gaps without repaint.

⸻

Known limits & tips

• If a proxy symbol isn’t available on your plan/exchange, you’ll see the NA warning: choose a different symbol via Symbol Search, or keep Carry-forward ON (it defaults to neutral where needed).

• Intraday VIX is sparse—using Daily is intentional.

• Dynamic OB/OS needs enough history (see dynLenFloor). On short histories it gracefully falls back to static levels.

Thanks for trying the preview. Your comments drive the roadmap—presets, new proxies, extra alerts, and integrations.

Relative Strength vs. Benchmark (相對強度)This "Relative Strength vs. Benchmark" indicator helps you see a stock's true performance against a benchmark (like the S&P 500) at a glance. By calculating the price ratio between the two, it strips away the overall market noise, allowing you to focus on identifying true market leaders and underperforming laggards.

How It Works

Core Formula: Relative Strength = Stock Price / Benchmark Index Price

A Rising Line: Means the stock is outperforming the benchmark.

A Falling Line: Means the stock is underperforming the benchmark.

The indicator also includes a Moving Average (MA) of the Relative Strength line itself. This MA helps to confirm the trend of relative strength and filter out short-term noise.

How to Use

Find Market Leaders: When the market is in an uptrend or consolidating, look for stocks whose RS line is breaking out to new highs.

Avoid Laggards: If the RS line is consistently below its moving average or making new lows, the stock is significantly underperforming the market and should be treated with caution.

Trend Change Signals: A cross of the RS line above its MA can be seen as a signal that a new trend of relative outperformance is beginning. A cross below suggests the trend is weakening.

Features & Settings

Customizable Benchmark: You can change the default benchmark from TWSE:TSE to any symbol you need, such as SP:SPX for the S&P 500 or NASDAQ:NDX for the Nasdaq 100.

Adjustable MA Length: Customize the period for the RS Moving Average to fit your trading style (short-term or long-term).

Visual Toggle: Easily turn the colored background fill on or off according to your preference.

Hope you find this tool helpful in your analysis!

QQQ Ladder → Adjusted to Active Ticker (5s & 10s)This indicator allows you to a grid of QQQ levels directly on futures chart like NQ, MNQ, ES and MES, automatically adjusting for the spread between the displayed symbol and QQQ. This is particularly useful for traders who perform technical analysis on QQQ but execute trades on Futures.

Features:

Renders every 5 and 10 points steps of QQQ in your current chart.

The script adjusts these levels in real-time based on the current spread between QQQ and the displayed symbol!

Plots updated horizontal lines that move with the spread

Supports Multiple Tickers, ES1!, MES1!, NQ1!, MNQ1! SPY and SPX500USD.

NDX Ladder → Adjusted to Active Ticker (5s & 10s)This indicator allows you to a grid of NDX levels directly on the NQ! (E-mini NASDAQ 100 Futures) chart, automatically adjusting for the spread between NDX and NQ1!. This is particularly useful for traders who perform technical analysis on SPX but execute trades on NQ1!.

Features:

Renders every 5 and 10 points steps of the NDX in your current chart.

The script adjusts these levels in real-time based on the current spread between NDX and NQ / MNQ

Plots updated horizontal lines that move with the spread

ICT First FVG - 9:30am & Custom (v4)ICT First FVG - 9:30am & Custom Time Ranges (v4)

📖 DESCRIPTION

This comprehensive Pine Script indicator identifies and displays Fair Value Gaps (FVGs), Volume Imbalances (VIs), and Liquidity Voids (LVs) based on Inner Circle Trading (ICT) concepts. The indicator offers dual functionality: traditional 9:30am New York session FVG detection and customizable time range analysis for maximum flexibility.

🚀 KEY FEATURES

Dual Detection System

9:30am NY Open FVG: Classic ICT first presentation detection after market open

Custom Time Range FVG: User-configurable time periods for specialized analysis

Independent Operations: Both systems work simultaneously without interference

Separate Controls: Each system has its own settings and previous days configuration

Advanced Gap Detection

Fair Value Gaps (FVG): Three-candle patterns showing price inefficiencies

Volume Imbalances (VI): Single candle volume-related gaps

Liquidity Voids (LV): Areas where price moved too fast, creating liquidity gaps

Consequent Encroachment (CE): Midpoint lines of detected inefficiencies

Precision Sizing System

Multi-Asset Support: Automatic point/pip calculation for Forex, Futures, and Indices

Forex Handling: Specialized pip calculation for major pairs and JPY crosses

Size Filtering: Minimum gap size filter to eliminate noise

Real-Time Display: Shows exact gap sizes in labels (e.g., "15.3 pips" or "12.7 pts")

Professional Visualization

Dual Display Modes: Choose between solid blocks or line representations

Color Coding: Different colors for current vs. previous day imbalances

Smart Labels: Configurable date, time, type, and size information

Extension Options: Extend gaps to session end or current bar

M1 Data Integration

High Accuracy: Uses 1-minute data regardless of chart timeframe

Better Detection: More precise gap identification on higher timeframes

Flexible Usage: Works on any timeframe ≤15 minutes

⚙️ CONFIGURATION GUIDE

General Settings

Visualization Type: Choose "Blocks" for filled areas or "Lines" for boundaries

Previous Days: Number of historical days to display (0 = today only)

Extend Imbalances: Project gaps to session end or current bar

Use M1 Data: Recommended ON for better accuracy

FVG Size Filter

Minimum FVG Size: Filter out gaps smaller than specified points

Enable Filter: Toggle size filtering on/off

🎯 RECOMMENDED MINIMUM SIZES:

USD/JPY: 0.01 points (1 pip)

Gold (XAUUSD): 1.6 points

NQ (Nasdaq-100): 0.2 points

Nasdaq CFD: 2.0 points

Other instruments: Experiment and discover optimal values

Custom FVG System

Enable Custom FVG: Activate secondary time range detection

Custom Time Range: Use session format (e.g., "1430-1600" for 2:30-4:00 PM)

Custom Previous Days: Independent historical period for custom ranges

Custom Label Color: Distinct color for custom time range gaps

Delete Default FVG 9:30: Use when running multiple instances with different timeframes

Imbalance Types

Fair Value Gaps: Main three-candle inefficiency patterns

Include Open/Close Gap: Additional gap calculation method

Volume Imbalances: Single-candle volume-based gaps

Liquidity Voids: Fast price movement gaps

C.E. (Consequent Encroachment): Midpoint reference lines

Label Customization

Show Labels: Toggle date/time information display

Include Time: Add timestamp to labels

Include Type: Display gap type (FVG, VI, LV)

Include Size: Show calculated gap size in points/pips

Position: Configure label placement (left/center/right, top/center/bottom)

Size & Color: Customize label appearance

Visual Styling

Colors: Separate colors for FVG, VI, LV types

Previous Day Colors: Distinct styling for historical gaps

Border Styles: Solid, dashed, or dotted borders

Line Widths: Configurable border thickness

📊 TECHNICAL SPECIFICATIONS

Supported Markets

Forex: All major and minor pairs with proper pip calculation

Futures: ES, NQ, YM, RTY, GC, SI, CL, etc.

Indices: SPX, NDX, DJI, and CFD versions

Stocks: Individual equities (adjust size filter accordingly)

Time Frame Compatibility

Recommended: 1m, 3m, 5m, 15m charts

Maximum: 15-minute timeframe

Optimal: 1m or 5m for best precision

Session Handling

Timezone: America/New_York (Eastern Time)

Default 9:30am: Standard NY market open detection

Custom Sessions: Any time range using HHMM-HHMM format

Weekend Filtering: Automatic exclusion of non-trading days

🔧 USAGE INSTRUCTIONS

Basic Setup

Add indicator to chart (≤15m timeframe recommended)

Enable "Use M1 Data" for accuracy

Set "Minimum FVG Size" based on instrument (see recommendations above)

Configure "Previous Days Imbalances" (5 is good default)

Custom Time Range Setup

Enable "Enable Custom FVG"

Set "Custom Time Range" (e.g., "1430-1600" for 2:30-4:00 PM ET)

Adjust "Custom Previous Days" as needed

Choose distinct "Custom Label Color" for easy identification

Multiple Instance Usage

Add indicator multiple times for different time ranges

Enable "Delete Default FVG 9:30" on additional instances

Use different custom time ranges for each instance

Assign unique colors to distinguish between instances

Label Optimization

Enable size display to see gap magnitude

Position labels to avoid chart clutter

Use appropriate label size for your screen resolution

Consider disabling time display on crowded charts

🎯 PRACTICAL APPLICATIONS

ICT Trading Concepts

First Presentation: Initial FVG after 9:30am NY open

Return to Gap: Price revisiting inefficiency areas

Mitigation Levels: Using FVG boundaries as support/resistance

Liquidity Hunting: Understanding where price seeks efficiency

Multi-Session Analysis

London Close: Set custom range for 1600-1601 London close gaps

Asian Session: Configure overnight inefficiencies

Power Hour: Analyze 1500-1600 ET gaps

Lunch Hour: Study 1200-1300 ET price behavior

Risk Management

Size-Based Filtering: Focus on significant gaps only

Historical Context: Compare current gaps to previous days

Confluence Trading: Combine with other ICT concepts

Session-Specific: Target gaps from specific market sessions

⚠️ IMPORTANT NOTES

Performance Considerations

Maximum Objects: Indicator creates multiple visual elements

Historical Limit: Adjust "Previous Days" to balance history vs. performance

Chart Refresh: Allow time for initial loading on historical data

Data Quality

Broker Dependency: Gap detection accuracy depends on data feed quality

Weekend Gaps: Sunday gaps may appear due to data provider differences

Fast Markets: Extremely volatile periods may create false gaps

Best Practices

Timeframe Consistency: Use same timeframe for analysis and execution

Size Calibration: Adjust minimum sizes based on instrument volatility

Session Awareness: Understand which sessions produce most relevant gaps

Confirmation: Use additional ICT concepts to confirm gap validity

[DEM] Correlation Coefficient Correlation Coefficient is designed to calculate and visualize the statistical correlation between the current chart's price movement and another selected symbol (defaulting to SPX) over a specified period. The indicator displays the correlation coefficient as both a colored area chart and line plot in a separate pane below the main chart, with colors dynamically changing from red (negative correlation) through purple (no correlation) to green (positive correlation) based on the strength and direction of the relationship. The correlation values range from -1 (perfect negative correlation) to +1 (perfect positive correlation), with horizontal reference lines at these extremes and zero, helping traders understand how closely their asset moves in relation to the selected benchmark symbol and identify periods of divergence or convergence in market behavior.

Futures Forward Price [NeoButane]In futures markets, the theoretical value of a futures contract can be derived from its underlying price and cost of carry. By baking in the costs and potential yields, the theoretical forward price then be used in basis against futures prices in place of the underlying spot price.

Usage

The script creates plots on the main chart and a separate window pane. Both are meant to be used to visualize dislocations in the market.

By using a futures vs. forward basis instead of futures vs. spot basis, discounts in the market are clearer.

Last month, the gold futures market GCZ2025 traded >1% above forward price when tariffs were announced and fell back in line once the tariffs were verbally retracted.

View roll spreads over a back-adjusted continuous chart. I guess. I don't think spread traders only look at one chart. This is as educational for me as it is you.

Configuration

The underlying reference needs to be changed to match the futures contract you are using.

The Risk-Free Rate defaults to FRED:SOFR. I found the contract month matched 3-Month SOFR Futures to be the closest for forward price.

Risk-Free Rate: The interest rate source for forward price.

Constant Risk-Free Rate: a static interest rate that can be used in advance of future changes in risk-free rate.

Underlying Reference: spot or index price. Some examples include TVC:SPX, TVC:GOLD, CRYPTO:BTCUSD, TVC:USOIL.

Forward Price Compounding: determines which formula to use. They're similar and become closer as the contract matures.

Alternative Contract: enable and select a futures contract to use it on a chart different than the main.

Storage Cost and Yield: for use with commodities. I haven't found a proper use for them yet but enabling is simple if you are able to.

The following are meant to be used with the continuous formula as they are compounded. However the rate sources don't differ much for the purpose of futures prices.

3-Month CME SOFR Futures

3-Month ICEEUR SONIA Futures

3-Month Osaka TONA Futures

The other rate sources are either meant for futures contracts shorter than quarterly such as monthly crypto futures or were meant to help myself understand how different rates would align with futures prices, like inflation.

What this script does

It uses the cost of carry formula to output the forward price (red line). The underlying reference (green line) is plotted alongside and a futures-derived reference (blue line) can be displayed to see how it looks next to the real reference price.

The data pane displays either the nominal difference or percentage difference between the real futures price and the calculated forward price.

Further reading

www.investopedia.com

www.cmegroup.com

www.oxfordenergy.org

www-2.rotman.utoronto.ca

www.cmegroup.com

3-month rate futures

www.cmegroup.com

www.ice.com

www.bankofengland.co.uk

www.jpx.co.jp

ICT FVG Buy/Sell SignalsThis bot is built on ICT (Inner Circle Trader) concepts such as:

Fair Value Gaps (FVGs) – imbalance zones between candles.

Consequent Encroachment (CE) – the midpoint of a gap.

Premium / Discount Arrays – dealing ranges split into premium (sell-side) and discount (buy-side) zones.

Displacement candles – strong impulsive moves that confirm intent.

The bot scans for FVGs, marks CE levels, and waits for price to return to these levels.

When price revisits a valid FVG zone with displacement confirmation and in the correct PD array, the bot generates a BUY or SELL signal.

✅ Signal Rules

Buy Signal

Price trades back into a Bullish FVG.

Current bar shows bullish displacement (large bullish body relative to ATR).

Price is in discount territory of the current dealing range (if PD filter is enabled).

Close is above the CE line of the FVG.

Sell Signal

Price trades back into a Bearish FVG.

Current bar shows bearish displacement.

Price is in premium territory of the current dealing range.

Close is below the CE line of the FVG.

🎯 What You’ll See on the Chart

Green “BUY” labels below candles when long signals trigger.

Red “SELL” labels above candles when short signals trigger.

Shaded background:

Red = Premium zone (sell side).

Teal = Discount zone (buy side).

Yellow line = dealing range midpoint (equilibrium).

Dots on CE lines = midpoints of the latest bullish/bearish FVG.

🔔 Alerts

ICT Buy → Triggers when a bullish setup confirms.

ICT Sell → Triggers when a bearish setup confirms.

You can connect these alerts to:

TradingView notifications.

Webhooks (for brokers or bots like MetaTrader, NinjaTrader, or Discord).

⚙️ Settings

Swing length – how many bars to use when detecting swing highs/lows for the dealing range.

Use PD filter – toggle ON/OFF for requiring discount/premium alignment.

Displacement ATR multiple – how strong the candle body must be compared to ATR to count as a displacement.

ATR length – used for displacement filter.

📈 Supported Markets

Works on all symbols and timeframes.

Commonly applied to:

NASDAQ (NQ, QQQ)

S&P500 (ES, SPX, SPY)

Forex pairs

Crypto (BTC, ETH, etc.)

⚠️ Disclaimer

This bot is for educational purposes only. It does not guarantee profits and should be tested on demo accounts first.

Always apply proper risk management before trading live.

Rolling Performance Toolkit (Returns, Correlation and Sharpe)This script provides a flexible toolkit for evaluating rolling performance metrics between any asset and a benchmark.

Features:

Library-based: Built on a custom utilities library for consistent return and statistics calculations.

Rolling Window Control: Choose the lookback period (in days) to calculate metrics.

Multiple Modes: Toggle between Rolling Returns, Rolling Correlation, and Rolling Sharpe Ratio.

Benchmark Comparison: Compare your selected ticker against a benchmark (default: S&P 500 / SPX), but you can easily switch to any symbol.

Risk-Free Rate Options: Choose from zero, a constant annual % rate, or a proxy symbol (default: US03M – 3-Month Treasury Yield).

Annualized Sharpe: Sharpe ratios are annualized by default (×√252) for intuitive interpretation.

This tool is useful for traders and investors who want to monitor relative performance, diversification benefits, or risk-adjusted returns over time.

Market Internal Strength (DJI/Nasdaq/S&P)Market Health Dow, Nasdaq & S\&P 500 Breadth

Track the true internal health of the US market's three most important indices the Dow Jones Industrial Average (DJI), the Nasdaq 100 (NDX), and the S\&P 500 (SPX).

Price action alone can be deceiving. A rising index might be driven by only a handful of mega-cap stocks, masking underlying weakness. This indicator provides a crucial look "under the hood" to measure the market's true breadth.

It visualizes the percentage of stocks within each index that are trading above their key moving averages (5, 20, 50, 100, 150, and 200-day). This allows you to instantly gauge whether a market trend is broadly supported by the majority of its constituent stocks.

Key Features

* Covers 3 Major US Indices Seamlessly switch your analysis between the Dow Jones, Nasdaq 100, and S\&P 500.

* Complete Breadth Picture Six MA periods offer a full view, from short-term momentum (5D, 20D) to the long-term institutional trend (150D, 200D).

* Fully Customizable Toggle the visibility of any line and adjust overbought/oversold levels to fit your personal strategy.

How to Use

1. Extreme Readings (Overbought/Oversold)

* Above 80% Signals a very strong, potentially overbought market. Caution is advised as a pullback could be near.

* Below 20% Signals a deeply oversold market, often indicating capitulation and potential buying opportunities.

2. Divergence (Powerful Warning Signal)

* Bearish The index price makes a new high, but this indicator makes a lower high. This warns that the rally is not broad-based and may be losing steam.

* Bullish The index price makes a new low, but this indicator makes a higher low. This suggests internal strength is building and a bottom may be forming.

3. Trend Confirmation

When the long-term lines (150D, 200D) remain high (e.g., \> 50%), the primary market trend is healthy and confirmed.