Green to Red Money RailsWhat this indicator does

Green to Red Money Rails (G2R Rails) is a price-action tool that draws dynamic “rails” from recent swing lows and highs. It tracks how support and resistance are shifting so you can see where trend pressure is building or weakening.

Core logic (high level)

Detects pivot lows and stores the last three (L1, L2, L3).

Builds green support “fans”: inner dotted rails L1→L2 and L2→L3, plus a main solid base rail L1→L3.

Detects pivot highs and, when the last high is lower than the previous one, draws a red resistance rail from H2→H3.

Optional labels mark the most recent swing low (“L”) and swing high (“H”).

How to use it

Use the green rails as dynamic support zones for trend-following, pullback entries, or stop placement.

Use the red rail as a visual ceiling in downtrends: breaks above it can signal the end of a sell-off; rejections at it confirm sellers still in control.

Works best on liquid markets and swing-trading timeframes (for example, 1h–1D). Always combine with your own risk management and higher-timeframe context.

This script does not auto-generate signals or manage risk for you; it is a visual framework for reading structure and building your own trading plans.

Kripto

CDVI – First Crypto Dominance Volatility Index by Armi GoldmanThe Crypto Dominance Volatility Index (CDVI) is the first volatility-based indicator designed specifically to analyze the stability and instability of dominance flows in the crypto market.

Instead of measuring price volatility, CDVI focuses on the volatility of market dominance itself — a structural driver behind capital rotation cycles such as Bitcoin Season, Altseason, accumulation zones, and macro cycle transitions.

CDVI transforms dominance changes into a clear volatility index that highlights compression, expansion, and regime shifts.

How it works

CDVI calculates the absolute or percentage-based realized volatility of your chosen dominance benchmark (BTC.D, TOTAL.D, or any dominance index available on TradingView).

The indicator then:

1. Smooths the volatility curve using adjustable parameters

2. Builds a long-term mean to identify regime structure

3. Computes percentile zones over a rolling lookback window

4. Highlights high-risk and low-risk dominance conditions using color-coded backgrounds

This creates a clean, noise-reduced volatility representation of the dominance market.

Why it looks like this

The CDVI curve is intentionally smooth and cyclical because dominance volatility behaves differently from price volatility:

• Dominance tends to trend slowly, then spike violently during rotation phases

• Periods of prolonged compression often occur before large macro moves

• Volatility bursts cluster during transitions (e.g. BTC → Alts, cycle tops, market-wide repricing)

The percentile zones (90% / 10%) give structural thresholds for extreme conditions.

Background color reveals when dominance volatility enters these extremes, creating visually clear “regime blocks.”

How to interpret CDVI

High CDVI (above the 90th percentile):

• Dominance instability

• Capital rotation phases are active

• Market is repricing sector allocations

• Often appears near Altseason tops or bottoms

• Signals caution for trend traders and opportunity for rotation traders

Low CDVI (below the 10th percentile):

• Compression and calm dominance

• Accumulation and structural balance

• Often precedes major expansions in Bitcoin or Alt markets

• Useful for anticipating cycle transitions before they break out

Long-term mean:

• Helps identify when the market is in a high-vol or low-vol regime

• Crossings around the mean often coincide with early cycle shifts

How to use CDVI in practice

1. Cycle Timing

Use CDVI to detect when the market moves from calm → expansion or expansion → exhaustion.

Low CDVI usually precedes major moves. High CDVI often marks transition turbulence.

2. BTC vs Altcoins Rotation

Combine CDVI with BTC.D / TOTAL2 / TOTAL3 to detect rotation windows.

High CDVI = dominance is unstable → rotations happen.

Low CDVI = dominance is stable → trending environment.

3. Risk Management

High CDVI suggests elevated structural risk (dominance shifting).

Low CDVI supports directional conviction.

4. Confluence with Price

When both price volatility and dominance volatility expand together → macro transition.

When price is volatile but CDVI is flat → noise, not structural change.

Who this indicator is for

• Cycle analysts

• Macro crypto traders

• BTC vs Alts rotation traders

• Portfolio allocators

• Long-term investors looking at structural market phases

CDVI is designed as a clean, structural tool for understanding volatility not of price — but of market power distribution.

Dumb Money Flow - Retail Panic & FOMO# Dumb Money Flow (DMF) - Retail Panic & FOMO

## 🌊 Overview

**Dumb Money Flow (DMF)** is a powerful **contrarian indicator** designed to track the emotional state of the retail "herd." It identifies moments of extreme **Panic** (irrational selling) and **FOMO** (irrational buying) by analyzing on-chain data, volume anomalies, and price velocity.

In crypto markets, retail traders often buy the top (FOMO) and sell the bottom (Panic). This indicator helps you do the opposite: **Buy when the herd is fearful, and Sell when the herd is greedy.**

---

## 🧠 How It Works

The indicator combines multiple data points into a single **Sentiment Index** (0-100), normalized over a 90-day period to ensure it always uses the full range of the chart.

### 1. Panic Index (Bearish Sentiment)

Tracks signs of capitulation and fear. High values contribute to the **Panic Zone**.

* **Exchange Inflows:** Spikes in funds moving to exchanges (preparing to sell).

* **Volume Spikes:** High volume during price drops (panic selling).

* **Price Crash (ROC):** Rapid, emotional price drops over 3 days.

* **Volatility (ATR):** High market nervousness and instability.

### 2. FOMO Index (Bullish Sentiment)

Tracks signs of euphoria and greed. High values contribute to the **FOMO Zone**.

* **Exchange Outflows:** Funds moving to cold storage (HODLing/Greed).

* **Profitable Addresses:** When >90% of holders are in profit, tops often form.

* **Parabolic Rise:** Rapid, unsustainable price increases.

---

## 🎨 Visual Guide

The indicator uses a distinct color scheme to highlight extremes:

* **🟢 Dark Green Zone (> 80): Extreme FOMO**

* **Meaning:** The crowd is euphoric. Risk of a correction is high.

* **Action:** Consider taking profits or looking for short entries.

* **🔴 Dark Burgundy Zone (< 20): Extreme Panic**

* **Meaning:** The crowd is capitulating. Prices may be oversold.

* **Action:** Look for buying opportunities (catching the knife with confirmation).

* **🔵 Light Blue Line:**

* The smoothed moving average of the sentiment, helpful for seeing the trend direction.

---

## 🛠️ How to Use (Trading Strategies)

### 1. Contrarian Reversals (The Primary Strategy)

* **Buy Signal:** Wait for the line to drop deep into the **Burgundy Panic Zone (< 20)** and then start curling up. This indicates that the worst of the selling pressure is over.

* **Sell Signal:** Wait for the line to spike into the **Green FOMO Zone (> 80)** and then start curling down. This suggests buying exhaustion.

### 2. Divergences

* **Bullish Divergence:** Price makes a **Lower Low**, but the DMF Indicator makes a **Higher Low** (less panic on the second drop). This is a strong reversal signal.

* **Bearish Divergence:** Price makes a **Higher High**, but the DMF Indicator makes a **Lower High** (less FOMO/buying power on the second peak).

### 3. Trend Confirmation (Midline Cross)

* **Crossing 50 Up:** Sentiment is shifting from Fear to Greed (Bullish).

* **Crossing 50 Down:** Sentiment is shifting from Greed to Fear (Bearish).

---

## ⚙️ Settings

* **Data Source:** Defaults to `INTOTHEBLOCK` for on-chain data.

* **Crypto Asset:** Auto-detects BTC/ETH, but can be forced.

* **Normalization Period:** Default 90 days. Determines the "window" for defining what is considered "Extreme" relative to recent history.

* **Weights:** You can customize how much each factor (Volume, Inflows, Price) contributes to the index.

---

**Disclaimer:** This indicator is for educational purposes only. "Dumb Money" analysis is a probability tool, not a crystal ball. Always manage your risk.

**Indicator by:** @iCD_creator

**Version:** 1.0

**Pine Script™ Version:** 6

---

## Updates & Support

For questions, suggestions, or bug reports, please comment below or message the author.

**Like this indicator? Leave a 👍 and share your feedback!**

Alos Volume Profile Candles (SVP)ALOS Volume Profile Candles (SVP)

Summary

IMPORTANT: This indicator is designed to be used only with TradingView's 'Session Volume Profile' chart type. It will not work correctly with standard candle charts.

This indicator powerfully visualizes intra-session price action by dividing a single session profile into a specific number of equal-sized synthetic candles.

Instead of viewing a session as one single block, you can now break it down into parts (like quarters or thirds) to see how price behaved during each segment of the profile.

Key Features

Custom Session Slicing: Set "Candles per session" to 4 to see the session in quarters, 6 to see it in sixths, or any number you choose.

Full Session Control: Works perfectly with any custom session time, including complex overnight sessions (like '1800-1700' for CME crypto futures)

Accurate OHLC Calculation: Each synthetic candle correctly calculates and displays its own Open, High, Low, and Close for its specific time slice.

Clean Charting: Use the "Keep last sessions" input to control how many old sessions are drawn, preventing chart clutter and keeping your analysis focused on recent price action.

How to Use

On your TradingView chart, change the chart type to "Session Volume Profile".

Add the "ALOS Volume Profile Candles (SVP)" indicator to your chart.

Set your desired Session time in the indicator settings (or keep the default).

Choose the number of Candles per session you want to divide it into.

Adjust Keep last sessions to control how much history is displayed.

This tool is ideal for traders who want to analyze price behavior during the opening, middle, and closing parts of a session, or for breaking down long 24-hour crypto sessions into more manageable chunks.

Smart Money Flow - Exchange & TVL Composite# Smart Money Flow - Exchange & TVL Composite Indicator

## Overview

The **Smart Money Flow (SMF)** indicator combines two powerful on-chain metrics - **Exchange Flows** and **Total Value Locked (TVL)** - to create a composite index that tracks institutional and "smart money" movement in the cryptocurrency market. This indicator helps traders identify accumulation and distribution phases by analyzing where capital is flowing.

## What It Does

This indicator normalizes and combines:

- **Exchange Net Flow** (from IntoTheBlock): Tracks Bitcoin/Ethereum movement to and from exchanges

- **Total Value Locked** (from DefiLlama): Measures capital locked in DeFi protocols

The composite index is displayed on a 0-100 scale with clear zones for overbought/oversold conditions.

## Core Concept

### Exchange Flows

- **Negative Flow (Outflows)** = Bullish Signal

- Coins moving OFF exchanges → Long-term holding/accumulation

- Indicates reduced selling pressure

- **Positive Flow (Inflows)** = Bearish Signal

- Coins moving TO exchanges → Preparation for selling

- Indicates potential distribution phase

### Total Value Locked (TVL)

- **Rising TVL** = Bullish Signal

- Capital flowing into DeFi protocols

- Increased ecosystem confidence

- **Falling TVL** = Bearish Signal

- Capital exiting DeFi protocols

- Decreased ecosystem confidence

### Combined Signals

**🟢 Strong Bullish (70-100):**

- Exchange outflows + Rising TVL

- Smart money accumulating and deploying capital

**🔴 Strong Bearish (0-30):**

- Exchange inflows + Falling TVL

- Smart money preparing to sell and exiting positions

**⚪ Neutral (40-60):**

- Mixed or balanced flows

## Key Features

### ✅ Auto-Detection

- Automatically detects chart symbol (BTC/ETH)

- Uses appropriate exchange flow data for each asset

### ✅ Weighted Composite

- Customizable weights for Exchange Flow and TVL components

- Default: 50/50 balance

### ✅ Normalized Scale

- 0-100 index scale

- Configurable lookback period for normalization (default: 90 days)

### ✅ Signal Zones

- **Overbought**: 70+ (Strong bullish pressure)

- **Oversold**: 30- (Strong bearish pressure)

- **Extreme**: 85+ / 15- (Very strong signals)

### ✅ Clean Interface

- Minimal visual clutter by default

- Only main index line and MA visible

- Optional elements can be enabled:

- Background color zones

- Divergence signals

- Trend change markers

- Info table with detailed metrics

### ✅ Divergence Detection

- Identifies when price diverges from smart money flows

- Potential reversal warning signals

### ✅ Alerts

- Extreme overbought/oversold conditions

- Trend changes (crossing 50 line)

- Bullish/bearish divergences

## How to Use

### 1. Trend Confirmation

- Index above 50 = Bullish trend

- Index below 50 = Bearish trend

- Use with price action for confirmation

### 2. Reversal Signals

- **Extreme readings** (>85 or <15) suggest potential reversal

- Look for divergences between price and indicator

### 3. Accumulation/Distribution

- **70+**: Accumulation phase - smart money buying/holding

- **30-**: Distribution phase - smart money selling

### 4. DeFi Health

- Monitor TVL component for DeFi ecosystem strength

- Combine with exchange flows for complete picture

## Settings

### Data Sources

- **Exchange Flow**: IntoTheBlock real-time data

- **TVL**: DefiLlama aggregated DeFi TVL

- **Manual Mode**: For testing or custom data

### Indicator Settings

- **Smoothing Period (MA)**: Default 14 periods

- **Normalization Lookback**: Default 90 days

- **Exchange Flow Weight**: Adjustable 0-100%

- **Overbought/Oversold Levels**: Customizable thresholds

### Visual Options

- Show/Hide Moving Average

- Show/Hide Zone Lines

- Show/Hide Background Colors

- Show/Hide Divergence Signals

- Show/Hide Trend Markers

- Show/Hide Info Table

## Data Requirements

⚠️ **Important Notes:**

- Uses **daily data** from IntoTheBlock and DefiLlama

- Works on any chart timeframe (data updates daily)

- Auto-switches between BTC and ETH based on chart

- All other crypto charts default to BTC exchange flow data

## Best Practices

1. **Use on Daily+ Timeframes**

- On-chain data is daily, most effective on D/W/M charts

2. **Combine with Price Action**

- Use as confirmation, not standalone signals

3. **Watch for Divergences**

- Price making new highs while indicator falling = warning

4. **Monitor Extreme Zones**

- Sustained readings >85 or <15 indicate strong conviction

5. **Context Matters**

- Consider broader market conditions and fundamentals

## Calculation

1. **Exchange Net Flow** = Inflows - Outflows (inverted for index)

2. **TVL Rate of Change** = % change over smoothing period

3. **Normalize** both metrics to 0-100 scale

4. **Composite Index** = (ExchangeFlow × Weight) + (TVL × Weight)

5. **Smooth** with moving average

## Disclaimer

This indicator uses on-chain data for analysis. While valuable, it should not be used as the sole basis for trading decisions. Always combine with other technical analysis tools, fundamental analysis, and proper risk management.

On-chain data reflects blockchain activity but may lag price action. Use this indicator as part of a comprehensive trading strategy.

---

## Credits

**Data Sources:**

- IntoTheBlock: Exchange flow metrics

- DefiLlama: Total Value Locked data

**Indicator by:** @iCD_creator

**Version:** 1.0

**Pine Script™ Version:** 6

---

## Updates & Support

For questions, suggestions, or bug reports, please comment below or message the author.

**Like this indicator? Leave a 👍 and share your feedback!**

OTT Volatility [RunRox]📊 OTT Volatility is an indicator developed by the RunRox team to pinpoint the most optimal time to trade across different markets.

OTT stands for Optimal Trade Time Volatility and is designed primarily for markets without a fixed trading session, such as cryptocurrencies that trade 24/7. At the same time, it works equally well on any other market.

🔶 The concept is straightforward. The indicator takes a specified number of historical periods (Samples) and statistically evaluates which hours of the day or which days show the highest volatility for the selected asset.

As a result, it highlights time windows with elevated volatility where traders can focus on searching for trade setups and building positions.

🔶 As the core volatility metric, the indicator uses ATR (Average True Range) to measure intraday volatility. Then it calculates the average ATR value over the last N Samples, creating a statistically stable estimate of typical volatility for the selected asset.

🔶 Statistically, during these highlighted periods the market shows higher-than-average volatility.

This means that in these time windows price is more likely to be subject to stronger moves and potential manipulation, making them attractive for active trade execution and position management.

⚠️ However, historical behavior does not guarantee future results.

These periods should be treated only as zones where volatility has a higher probability of being above normal, not as a promise of movement.

As shown in the screenshot above, the indicator also projects potential future volatility based on historical data. This helps you better plan your trading hours and align your activity with periods where volatility is statistically expected to be higher or lower.

🔶 Current Volatility – as shown in the screenshot above, you can also monitor the real-time volatility of the market without any statistical averaging.

On top of that, you can overlay the current volatility on top of the statistical volatility levels, which makes it easy to see whether the market is now trading in a high- or low-volatility regime relative to its usual behavior.

4 display modes – you can choose any visualization style that fits your trading workflow:

Absolute – displays the raw volatility values.

Relative – shows volatility relative to its typical levels.

Average Centered – centers volatility around its average value.

Trim Low Value – filters out low-volatility noise and highlights only more significant moves.

This indicator helps you define the most effective trading hours on any market by relying on historical volatility statistics.

Use it to quickly see when your market tends to be more active and to structure your trading sessions around those periods.

✅ We hope this tool becomes a useful part of your trading toolkit and helps you improve the quality of your decisions and timing.

BTC Future CME Cross-Market DetectorProject Spec: BTC CME Cross-Market Detector

1. Project Overview

Indicator Name

CME Cross-Market Detector

Objective

To identify high-probability trade setups by detecting and confirming "smart money" activity across two distinct market venues simultaneously: a primary crypto exchange (e.g., Bybit, Binance) and the institutional CME futures market.

Core Philosophy

Price movements are often preceded by the positioning of large, institutional players ("smart money"). While their activity can be seen on any single exchange, the signal becomes exceptionally reliable when the same footprint appears at the same time in both the broader crypto derivatives market and the highly regulated institutional futures market. This dual-market confirmation acts as a powerful noise filter, isolating signals that have a higher probability of follow-through.

2. Key Concepts & Signal Logic

The indicator's entire foundation rests on confirming that specific conditions are met on two datasets at the same time: (1) The user's current chart (e.g., BYBIT:BTCUSDT) and (2) The CME Bitcoin Futures chart (CME:BTC1!).

Smart Volume Analysis

To gauge buying vs. selling pressure, the total volume of a single candle is algorithmically split. This is not a perfect science but an effective estimation based on the candle's structure.

Buying Pressure is considered proportional to the distance the price closed from the low. Buying Pressure ≈ Total Volume × ((Close - Low) / (High - Low))

Selling Pressure is considered proportional to the distance the price closed from the high. Selling Pressure ≈ Total Volume × ((High - Close) / (High - Low))

Signal Trigger Conditions

For a potential signal to be identified on each market independently, two conditions must be met:

Volume Spike: The volume of the current candle must be significantly higher than the recent average volume (e.g., >150% of the 20-period moving average). This shows a sudden, high level of interest.

Pressure Imbalance: The estimated buying pressure must overwhelm the selling pressure by a certain factor (e.g., 3x), or vice versa for a sell signal. This indicates a clear directional intent.

The Final Confirmed Signal

A signal is only considered valid and plotted on the chart when the Signal Trigger Conditions (both Volume Spike and Pressure Imbalance) are met on both the primary chart and the CME chart on the very same candle.

3. Signal Strength Calculation

The percentage shown on the chart is a Signal Strength Score (0-100%), which rates the quality and conviction of the confirmed signal.

The score is calculated as follows:

Base Score Calculation (0-100 points): A base score is calculated for each market (primary and CME) by combining two factors:

Volume Component (0-50 pts): Measures the intensity of the volume spike. A 300% volume spike will score higher than a 150% spike.

Imbalance Component (0-50 pts): Measures the intensity of the buy/sell pressure ratio. A 5x imbalance will score higher than a 3x imbalance.

Advanced Modifiers (Bonus Points): The base score is then enhanced with bonus points for favorable conditions:

Trend Alignment (+10 pts): A buy signal that occurs during a clear uptrend receives extra points.

Candle Structure (+10 pts): A buy signal on a candle with a long lower wick (indicating rejection of lower prices) receives extra points.

Final Averaged Score: The final percentage you see is the average of the two individual strength scores calculated for the primary exchange and the CME market.

4. Visualization

Energy Waves: Signals are displayed as circles. Green for Buy Signals (below the candle) and Red for Sell Signals (above the candle).

Dynamic Sizing: The size of the circle directly reflects the Signal Strength Score, categorized into four distinct levels (e.g., 10%+, 40%+, 60%+, and 80%+) for at-a-glance interpretation.

Percentage Labels: Each signal is plotted with its precise, final strength score for clear analysis.

5. Summary: Steps to Replicate the Logic

To recreate this indicator, follow these high-level steps for each candle on the chart:

Gather Data: Fetch the Open, High, Low, Close, and Volume data for the primary chart asset AND for the corresponding CME Bitcoin Futures symbol (CME:BTC1!).

Calculate Buy/Sell Pressure: For both datasets, use the "Smart Volume Analysis" formula to estimate the buying and selling pressure for the current candle.

Check for Volume Spikes: For both datasets, calculate a simple moving average of the volume. Check if the current candle's volume exceeds this average by a set threshold (e.g., 150%).

Check for Pressure Imbalance: For both datasets, check if the buying pressure is greater than the selling pressure by a set multiplier (e.g., 3.0), or vice versa.

Confirm the Signal: A final signal is only valid if the conditions from both Step 3 and Step 4 are true for both datasets on the same candle.

Calculate Strength: If a signal is confirmed, compute a strength score (0-100) for each dataset based on the intensity of the volume spike and pressure imbalance. Add bonus points for confluence factors like trend alignment.

Finalize and Plot: Average the two strength scores from each market. Plot a colored, sized circle on the chart that visually represents this final averaged score, and display the score as a text label.

Last but not least, the idea of the indicator is inspired by 52SIGNAL

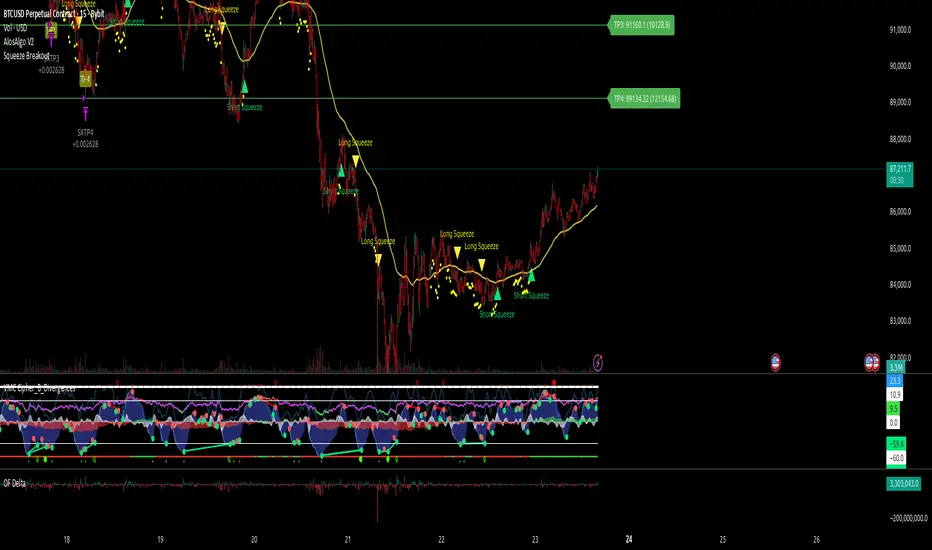

AlosAlgo V2 (BETA)— V2 BETA —

V2 – 2025-11-21 (Update)

• Rebuilt the core signal engine to remove repainting – higher-timeframe Heikin Ashi / Renko now use confirmed bars only for more stable signals & alerts.

• Added Trend Filter MA so longs are only taken above the MA and shorts only below (optional).

• Added MACD momentum filter and Price Action filter (Higher Low for longs, Lower High for shorts) to cut a lot of chop.

• Introduced a loss-streak “circuit breaker” – after X consecutive losing trades the strategy pauses for a set number of bars.

• New TP/SL engine with 2 modes: ATR-based or Fixed % moves, with 4 staged TPs plus an optional runner and break-even SL after TP2.

• Cleaned up TP/SL lines & labels so levels are fixed per trade and easier to read.

• General refactor for more realistic backtests, better live behaviour and easier parameter tuning compared to V1.

ABOUT

AlosAlgo V2 is a multi-timeframe trend + momentum strategy designed for BTC and other high-liquidity markets. It takes directional bias from a higher timeframe, then filters that bias with volatility, momentum and simple price-action structure before it ever opens a trade.

Purely rule-based, no AI / Bayesian / ML.

Core idea

– Use higher-timeframe structure for direction.

– Only trade when trend, momentum and basic price action agree.

– Manage exits with multiple TPs, an optional runner and a hard SL so risk is defined from the start.

Setups

Two main engines:

• Open/Close – Higher-timeframe Heikin Ashi body direction (close vs open) as the core trend signal.

• Renko – ATR-based Renko feed with EMA cross (fast vs slow) as the core trend signal.

Classic sideways filters (ATR + RSI) can be layered on top if you want to only trade in trending or ranging conditions.

Filters added in V2

• Trend Filter MA – Longs only above the MA, shorts only below (length configurable).

• Momentum Filter – Optional MACD filter; only takes longs when MACD is bullish and shorts when MACD is bearish.

• Price Action Filter – Optional HL/LH logic using pivots: longs after a Higher Low, shorts after a Lower High.

• Loss-Streak Circuit Breaker – After N losing trades in a row, the strategy pauses entries for a set number of bars to avoid bad regimes / tilt.

Risk & exits

Two TP/SL modes:

• ATR mode – SL and TP1–TP4 based on ATR at entry (stopFactor / profitFactor).

• Fixed % mode – SL and TP1–TP4 defined as % moves from entry.

On entry the strategy:

• Opens a single position.

• Places 4 staged TPs (TP1–TP4) with user-defined % sizing.

• Optionally leaves a “runner” managed only by SL and trend changes.

• Can move SL to break-even automatically after TP2 (toggle).

All TP/SL levels are locked at entry and drawn on the chart with labels so you can see exactly what the trade is trying to do.

Non-repainting behaviour

V2 is refactored to avoid the repainting behaviour that V1 used. Higher-timeframe and Renko data are taken from confirmed bars only, and entries are based on state (e.g. > / <) instead of repaint-prone crosses. Backtests are much closer to what you’ll see live, and alerts line up with executed trades more reliably.

How to use (suggested defaults)

• Setup: Open/Close

• TPSType: Fixed %

• Trend Filter: ON

• Momentum Filter: ON

• Price Action Filter: ON

• Sideways Filter: No Filtering

Then tweak TP/SL distances and filters per asset + timeframe, and forward-test before sizing up.

Disclaimer

This is not financial advice, not a guarantee of profit and not a “set and forget” money printer. Always forward-test, paper trade and tune risk before using real capital or automation. Markets change – this is a tool, not a promise.

[CASH] Crypto And Stocks Helper (MultiPack w. Alerts)ATTENTION! I'm not a good scripter. I have just learned a little basics for this project, stolen code from other public scripts and modified it, and gotten help from AI LLM's.

If you want recognition from stolen code please tell me to give you the credit you deserve.

The script is not completely finished yet and contains alot of errors but my friends and family wants access so I made it public.

_________________________________________________________________________________

CASH has multiple indicators (a true all-in-one multipack), guides and alerts to help you make better trades/investments. It has:

- Bitcoin Bull Market Support Band

- Dollar Volume

- 5 SMA and 5 EMA

- HODL Trend (a.k.a SuperTrend) indicator

- RSI, Volume and Divergence indicators w. alerts

More to come as well, like Backburner and a POC line from Volume Profile.

Everything is fully customizable, appearance and off/on etc.

More information and explainations along with my guides you can find in settings under "Input" and "Style".

BTC Risk Metric DCA Adapter (3Commas Webhook Strategy)Risk Metric DCA Adapter (3Commas Webhook Strategy) - WORK IN PROGRESS

This Pine Script strategy, originally inspired by the Risk Metric Indicator, is fundamentally engineered as an Adapter to interface with external trading bots like 3Commas via Webhooks. It calculates a dynamic market risk score and translates that score into specific dollar-cost averaging (DCA) entry levels and tiered profit-taking exits.

Key Features & Logic

Risk Metric Calculation (Credit to The Trading Parrot):

The strategy incorporates a complex, multi-timeframe Risk Metric calculation based on daily and weekly moving averages (SMA) and standard deviation (StDev). This metric aims to quantify the current market overextension or compression relative to long-term historical data. The resulting score dictates the level of conviction for a new trade.

Tiered DCA Entry Sizing:

The strategy defines three distinct Buy Levels (L1, L2, L3) corresponding to increasingly favorable (lower) Risk Metric scores.

L1 (Base): Risk is moderate, initiating the minimum defined trade amount.

L2 (Scaled): Risk is low, initiating L1 amount + L2 amount.

L3 (Aggressive): Risk is very low, initiating L1 + L2 + L3 amounts.

Tiered Profit-Taking Exits:

The strategy implements a staggered, partial profit-taking approach based on the Risk Metric rising:

Sell L1 & L2: Closes a percentage of the current position when the Risk Metric reaches defined high thresholds, locking in partial profits.

Sell L3 (Full Exit): Closes the remaining position when the Risk Metric reaches the highest defined threshold.

The Adapter Function (Webhook Integration)

This script is unique because it uses the Pine Script strategy() function to trigger Order Fills, which are necessary to access powerful placeholders in the TradingView alert system.

Trigger Type: The alert must be set to trigger on Any order fill.

Dynamic Webhook Data: Instead of using fixed alert() commands, the strategy generates dynamic labels (e.g., BUY_ENTRY_L3_USD_1000 or SELL_L1_PCT_25) using the strategy.entry and strategy.close commands.

Data Transfer: The alert message then uses the placeholder {{strategy.order.comment}} to pass these dynamic labels to the 3Commas bot, allowing the bot to execute the precise action (e.g., start_deal_with_volume_in_quote_currency or close_deal_at_market_percentage).

Full Strategy Webhook payload

{

"secret": "YOUR_3COMMAS_SECRET_KEY",

"max_lag": "300",

"timestamp": "{{timenow}}",

"trigger_price": "{{close}}",

"tv_exchange": "{{exchange}}",

"tv_instrument": "{{ticker}}",

"action": "{{strategy.order.action}}",

"bot_uuid": "YOUR_BOT_UUID",

"strategy_info": {

"market_position": "{{strategy.market_position}}",

"market_position_size": "{{strategy.market_position_size}}",

"prev_market_position": "{{strategy.prev_market_position}}",

"prev_market_position_size": "{{strategy.prev_market_position_size}}"

},

"order": {

"amount": "{{strategy.order.contracts}}",

"currency_type": "base",

"comment": "{{strategy.order.comment}}"

}

}

Disclaimer: This script is an adapter tool and does not guarantee profit. Trading requires manual configuration of risk settings, bot parameters, and adherence to platform-specific setup instructions.

TernTable: Crypto SectorsTernTables:CryptoSecs

This was hung on my Sector ETFs script to see if I could filter some noise from crypto by applying a GICS (Global Industry Classification Standard) style sector model to the crypto markets.

Crypto classification is certainly a little more nuanced so not completely straightforward.

It was designed to filter a researched and organised view of generally recognised cryptocurrency sectors and their confirmed constituent components.

The main purpose was a shot at displaying live crypto market data on my chart with instantaneous visual analysis, using leader laggard colour logic for performance indication, plus bullish bearish colour logic using the header for instant visual sector strength analysis.

This was never going to be an exhaustive tool of course and amazingly only or two of the sector lists wont fit on your laptop screen without zooming but it’s UI versatility both in custom display and custom threshold functionality is very effective. Viewing a coin on your watchlist with its sector overlayed in the chart brings the optional visual alert function into consideration. All basic but all effective and all customisable

Can't ignore the educational value either it’s teaching by osmosis what the sectors do and which coins go where clues to why.

As an after thought - I added a live stock market filter for 20 sector-specific ETFs like SPY, QQQ, XLV, XLF, allowing the comparison of the live performance of traditional financial sectors to live crypto sector data without leaving your chart.

Not certain how often it will need to be updated and any feedback re the legitimacy and accuracy of its components is kindly welcomed it is up to date at date of publishing.

It’s pretty easy to use, here is a list what you're getting with sector classifications with brief descriptions

CMC 20

CoinMarketCap Top 20: the largest cryptos by market cap. Great starting point to see what the overall market is doing

ETFs

All major U.S.-listed Bitcoin & Ethereum ETFs. Lets you compare crypto performance directly with traditional finance

Layer 0

Foundational interoperability protocols (Polkadot, Cosmos, ICP, etc.). These are the “bridges” that allow different blockchains to communicate

Layer 1

Independent base-layer blockchains that run their own consensus and security (Bitcoin, Ethereum, Solana, Cardano, TON, etc.).

Layer 2

Scaling networks built on top of Layer 1s to increase speed and lower fees (Arbitrum, Optimism, Base, Polygon, zk-rollups, etc.)

Layer 3

Application-specific chains or rollups designed for one purpose (gaming chains, DeFi-specific, social, etc.)

Web3

The “ownership internet”: gaming tokens, NFTs, metaverse land, music/streaming platforms, social tokens, and creator-economy projects

DeFi

Decentralised Finance: lending platforms, decentralized exchanges, derivatives, yield aggregators, and insurance protocols

Decentralised Storage

Blockchain-based alternatives to AWS/Google Cloud (Filecoin, Arweave, Storj, etc.)

Oracles

Data providers that feed off-chain information (prices, weather, sports results) into smart contracts

Privacy

Privacy coins and protocols that obfuscate transaction details (Monero, Zcash, Beam, etc.)

Yield & Lending

Protocols focused purely on lending, borrowing, and yield generation

DEX

Pure decentralized exchanges (Uniswap, SushiSwap, Jupiter, GMX, etc.)

DAO

Governance tokens of major decentralized autonomous organizations (Maker, Lido, Aave, ENS, etc.)

Infrastructure / Middleware

The picks-and-shovels layer: node services, RPC providers, indexing, cross-chain bridges, etc

Real World Assets (RWA)

Tokenised traditional assets: treasuries, real estate, private credit, stablecoins backed by real-world collateral

Restaking & Liquid Restaking

EigenLayer ecosystem and liquid-restaking tokens (eigen, ether.fi, Pendle, etc.). Currently the fastest-growing narrative

Traditional Sector ETFs

Classic U.S. sector ETFs (SPY, QQQ, XLF, XLE, XLV, XLY, etc.). Extra layer of analysis by comparing live stock market conditions with livecrypto market conditions

A list of the UI Toggles

* Sector Dropdown

• Select Sector: Choose the sector to display (e.g., CMC 20, Layer 1, DeFi, etc.)

* Custom Tickers

• Enter Tickers: Input custom coin tickers (e.g., BTCUSD, ETHUSD) to track specific assets

* Show % Change Row

• Toggle On/Off: Display the % change row for each sector/coin

* Show Current Price Row

• Toggle On/Off: Display the current price for each sector/coin

* Show Price-Diff Row

• Toggle On/Off: Display the price difference (current price - previous day's price)

* Show Spacer Row

• Toggle On/Off: Add a spacer row between data rows for clarity

* Table Position

• Select Position: Choose the position of the data table on your chart (Top Left, Top Right, etc.)

Visual Options:

* Show Sector Name

• Toggle On/Off: Display the sector name pane label on chart

* Custom Bull/Bear Threshold

• Toggle On/Off: Set a custom threshold for bullish/bearish sector performance

• Threshold (%): Set the percentage threshold (e.g., 50%) for bullish/bearish classification

* Show Live % in Header

• Toggle On/Off: Display the live percentage change in the table header

* Dynamic Decimal Formatting

• Toggle On/Off: Enable dynamic formatting for numbers display.

* Sort by % Change

• Toggle On/Off: Sort sectors by % change in performance

* Enable Alerts

• Toggle On/Off: Enable alerts based on performance thresholds

* Alert Threshold (%)

• Set Threshold: Define the percentage threshold (e.g.,70%) for triggering alerts

* Cooldown (bars)

• Toggle On/Off: Enable cooldown to prevent alerts from triggering too quickly

• Cooldown Duration: Set the cooldown period in bars (e.g., 10 bars)

* % Threshold Mode

• Toggle On/Off: Enable % Threshold Mode to filter sectors based on a percentage change threshold

• Threshold %: Set the percentage for filtering sectors (e.g., only show sectors with > 5% change)

A lot of toggles probably left once favourites are set but this UI interface does allow experimentation with the utility of channelling raw live data through custom designed filters. Just saying !

I need to include this of course

This indicator provides sector-based organisation and real-time performance visualisation for cryptocurrencies. It is not intended to predict price movements or guarantee outcomes. Crypto assets carry significant risk, including loss of capital. Past performance does not guarantee future results. All data and sector classifications are best-effort and may be incomplete, inaccurate, or outdated. Nothing in this script should be interpreted as financial advice. You are solely responsible for your own trading decisions.

That’s it really, I am currently pleased with how this indicator turned out, if you have a crypto trading toolkit put this in it.

Liquidity Hunt Detector PDH/PDL [SmartFoxy]Liquidity Hunt Detector PDH/PDL

The Liquidity Hunt Detector (LHD) is designed to identify and anticipate liquidity grabs around the:

• Previous Day High (PDH);

• Previous Day Low (PDL).

It builds dynamic trigger levels that highlight where price may deliver its first impulse before reaching PDH/PDL.

The Liquidity Hunt Detector (LHD) identifies high-probability reversals and continuations around the Previous Day High (PDH) and Previous Day Low (PDL).

It dynamically tracks the market’s move from the session open, builds trigger levels toward PDH/PDL, and highlights where liquidity is most likely to be taken.

When price taps a Trigger Up/Down level, the indicator generates Long/Short signals with optional confirmation from the integrated MA Ribbon , ensuring only high-quality, trend-aligned setups are shown.

When price interacts with these trigger levels, the indicator generates signals that help traders evaluate the market structure and prepare for potential entries.

Designed for Forex, Crypto, Indices, Stocks , the LHD provides a clean and intuitive structure for navigating intraday liquidity grabs, session impulses, and directional bias shifts.

The indicator is built from three fully independent modules, each of which can be used separately:

Liquidity Hunt Detector (LHD)

Moving Average Ribbon (MA Ribbon)

Previous Day High/Low (PDH/PDL) levels

Liquidity Hunt Detector (LHD) Logic

1.1 Display LHD – Enables or disables the entire Liquidity Hunt Detector module.

1.2 Max Days – Number of previous days used to generate PDH/PDL levels.

1.3 GMT – Corrects all time-based calculations based on your broker/session timezone.

1.4 Calculation Method (Point A Logic)

1) Static Method

Point A = the session’s opening price.

Trigger lines are calculated strictly as a percentage of the move A → PDH or A → PDL.

Intraday fluctuations do not affect the calculation.

2) Dynamic Method

Point A updates using the current intraday high/low:

• If price forms a new low, Point A updates for the PDH-side calculations;

• If price forms a new high, Point A updates for the PDL-side calculations.

This produces trigger lines that reflect the true live market structure rather than a fixed opening reference.

1.5 Main OTT Time (Operational Trading Time)

This is the core time window during which the indicator:

• updates Point A;

• calculates trigger levels;

• validates PDH/PDL;

• draws AB / AC movement structure;

• generates entry signals.

Outside this window, no new signals or recalculations occur.

⚠ If your broker’s first candle opens at a non-standard time (e.g., 00:08), adjust the OTT start time to avoid visual artifacts.

1.6 Show Line A – Displays the opening price level (Point A) until the end of the OTT window.

Style, width, and color are customizable.

1.7 Show Line AB — Price Movement Toward PDH.

Static Method – Single line: A → PDH

Dynamic Method – Two segments:

• A → Daily Low;

• Daily Low → PDH.

If PDH is swept, the “B” label switches to Sweep PDH.

1.8 Show Line AC – Price Movement Toward PDL.

Static Method – Single line: A → PDL

Dynamic Method – Two segments:

• A → Daily High;

• Daily High → PDL.

If PDL is swept, the “C” label switches to Sweep PDL.

1.9 Show Trigger Up Line (LONG Trigger) – Defines the level where the Long signal can activate.

By default, at 50% of the A → PDH movement.

When price touches this line, the script may:

• show a LONG label;

• trigger an alert.

All visual parameters are customizable.

1.10 Show Trigger Up Line (LONG Trigger)

Same logic as Trigger Up, but based on A → PDL.

1.11 Show Main Zone (OTT Zone) – Visual background highlighting of the active OTT window.

Helps instantly see:

• whether signals are allowed;

• how much time remains in the trading window?

Color and opacity are adjustable.

1.12 Upper Zone (toward PDH) – Tracks the protected area towards PDH.

Updates dynamically with new highs.

1.13 Lower Zone (toward PDL) – Tracks the zone toward PDL.

Updates dynamically with new lows.

1.14 Show Labels – Displays reference labels (A, B, C, Trigger Up, Trigger Down).

Label size is customizable.

1.15 Add Price – Adds the exact price value to each label.

1.16 Change Color after Sweep PDH or PDL – After PDH or PDL is broken, the indicator automatically recolors lines and labels to visually confirm the sweep.

1.17 Show SHORT Label – Displays the SHORT entry label when all conditions for a bearish signal are met.

Style parameters are set in the previous blocks.

1.18 Alert on Bearish Trigger Down – Triggers an alert when the price activates the bearish trigger.

1.19 Show LONG Label – Displays the LONG entry label when bullish conditions are met.

Style parameters are set in the previous blocks.

1.20 Alert on Bullish Trigger Up – Triggers an alert when the price activates the bullish trigger.

1.21 Alerts Active Time – Defines a custom time interval during which trigger signals are allowed.

Even if price touches a trigger level,

❗ signals will NOT be generated outside this allowed time.

Useful for:

• avoiding Asian session signals;

• reducing noise in low-liquidity periods.

1.22 Labels and Alerts Display Mode

Two settings modes:

• On Trigger (Instant Mode) – Signals appear immediately when price touches the trigger.

• On Candle Close (Conservative Mode) – Signals form only after the candle closes beyond the trigger level.

A more conservative option.

1.23 Delay LHD Signal Until MA Ribbon Confirms Direction – If enabled, LHD signals will NOT fire until the MA Ribbon produces a matching directional signal.

Logic:

• Price hits the trigger → LHD conditions become “armed”;

• The indicator waits;

• When MA Ribbon confirms trend direction (Long/Short);

• The final LHD label + alert is generated.

This ensures LHD trades are filtered and aligned with MA-based trend confirmation.

⚠ Works only when the MA Ribbon module is active.

AlosAlgoAlosAlgo Version: 1 BETA

A multi-timeframe, ATR-driven trend strategy with flexible entry engines (Open/Close vs Renko), optional HTF Heikin Ashi filtering, and a built-in 3-stage take-profit model designed to be backtested on TradingView and automated via webhooks.

@MO_XBT - EMA/MA ToolkitClean set of EMAs & MAs I use for trend tracking, momentum shifts, and cross signals

If you found this useful, follow me on X: @mo_xbt

Adaptive Volume Trend - [RZ]Adaptive Volume Trend

Introduction

The Adaptive Volume Trend is a dynamic, volume-weighted trend detection indicator designed to identify significant directional shifts in market momentum. By integrating price and volume data into a single adaptive framework, it helps traders visualize when market participation supports upward or downward trends.

The indicator adapts to volatility conditions through statistical measures, offering a refined approach to trend confirmation beyond traditional moving averages.

Key Features

Dynamic Volume-Weighted Analysis : Utilizes a Volume-Weighted Moving Average (VWMA) combined with exponential smoothing to account for both price movement and traded volume.

Adaptive Thresholding : Implements a rolling standard deviation-based system that automatically adjusts sensitivity to volatility and market conditions.

Color-Coded Trend Visualization : Optional bar and line coloring dynamically represent bullish and bearish market states for intuitive chart interpretation.

Alert Conditions : Built-in alerts notify users when bullish or bearish thresholds are breached, enabling timely trading decisions.

Customizable Parameters : Users can modify VWMA length, smoothing period, threshold sensitivity, and color settings to align with their preferred trading style or asset characteristics.

How It Works

The indicator calculates a smoothed VWMA of the closing price weighted by trading volume, then compares the logarithmic deviation of price from this adaptive average. A dynamic standard deviation is applied over a defined period to establish upper and lower threshold bands that represent statistically significant price deviations.

When the oscillator crosses above the upper threshold, it signals potential bullish strength supported by rising volume.

When it falls below the lower threshold, it indicates bearish dominance or weakening momentum.

A scoring mechanism assigns values (+1 for bullish, –1 for bearish) which drive both bar and line color changes, providing immediate visual feedback.

The EMA overlay line, color-shifted by signal strength, further emphasizes ongoing directional trends.

This adaptive mechanism ensures responsiveness during high-volatility markets while filtering noise during consolidation phases.

ES

NVIDIA

GOLD

Conclusion

The Adaptive Volume Trend indicator offers traders a balanced, adaptive framework to analyze volume-backed price movements. By dynamically adjusting to volatility and market participation, it enhances the reliability of trend detection and visual clarity on charts. It serves as a valuable addition for traders seeking volume-informed trend confirmation and dynamic market structure insights.

Disclaimer

This indicator is provided for educational and analytical purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. Past performance is not indicative of future results. Users should conduct their own analysis and manage risk appropriately before making any trading decisions.

XenoSmooth Predictive Candles - Advanced Heikin Ashi CandlesXenoSmooth Predictive Candles

Summary in one paragraph

A synthetic candle engine for crypto, FX, equities, and futures on intraday to swing timeframes. It reduces noise and flip delay so structure is easier to read. The core novelty is a predictive open with inertia plus slope lead fused with a zero lag body filter and an overshoot based wick model normalized by the real range and capped by ATR. Add it to a clean chart, hide regular candles if desired, and tune lengths. Shapes can move while the bar is open and settle on close. For conservative workflows read on bar close.

Scope and intent

• Markets. Major FX pairs, index futures, large cap equities, liquid crypto

• Timeframes. One minute to daily

• Purpose. Faster and smoother visual structure than Heikin Ashi while keeping causality and realistic wicks

Originality and usefulness

• Unique concept. Predictive open with inertia and slope lead plus selectable zero lag body filter and ATR capped wick overshoot in percent of real range

• Failure mode addressed. Late flips in chop and unreal long wicks from raw extremes

• Testability. Every control is an input. Users can toggle body method, lengths, clipping, and percent modeling

• Portable yardstick. ATR based wick cap and percent of bar range scale across symbols

Method overview in plain language

Build a robust base price from O, H, L, and extra weight on Close. Smooth it with a chosen filter to produce the synthetic close. Drive a predictive open that follows the synthetic close with tunable inertia and a small lead from the last bar slope. Model wicks as the portion of the real extremes that extends beyond the synthetic body, smooth that overshoot, normalize by the bar range if selected, then cap by ATR to avoid tail spikes. Clamp synthetic values to the real high and low if enabled.

Base measures

• Range basis. True Range for the ATR cap and High minus Low for percent normalization

• Return basis. Not used

Components

• Body Base Blend. Weighted O H L with a close bias to stabilize the base

• Zero Lag Body Filter. ZLEMA or Super Smoother or WMA to set the synthetic close

• Predictive Open. Inertial follow of the synthetic close plus a slope lead term

• Wick Overshoot Model. Smoothed extension beyond the body, optional percent of real range, ATR cap

• Clamp Option. Keeps synthetic open and close inside the real bar range

Fusion rule

• Synthetic close equals filtered base

• Synthetic open equals previous open plus inertia times distance to synthetic close plus slope lead

• Wicks equal smoothed overshoot above and below the body, optionally percent of range then converted back to price and capped by ATR

Inputs with guidance

Setup

• Signal timeframe. Uses the chart timeframe

• Invert direction. Not applicable

• Session windows. Not applicable

Logic

• Body length. Core smoothing length for the synthetic close. Typical 6 to 14. Higher gives smoother and slower. Lower gives faster flips

• Body method. ZLEMA or Super Smoother or WMA. ZLEMA is fastest. Super Smoother is calmest

• Close weight in base. 0 to 1. Higher gives stronger emphasis on close and less noise

• Open inertia. 0 to 1. Higher makes the open follow the close more tightly

• Lead gain. 0 to 1. Higher adds more phase lead. Keep modest to avoid overshoot

• Clamp body to real range. On keeps synthetic body inside high and low

• Wick smooth length. Typical 4 to 10. Higher reduces jitter

• Overshoot as percent. On stabilizes wicks across regimes

• ATR length. Typical 10 to 20 for the cap

• Max wick equals ATR times. 0 disables. 1.0 to 2.0 contains extreme tails

Filters

• Efficiency or trend filter. Not used

• Micro versus macro range relation. Not used

• Location filter. Not used

Realism and responsible publication

• No performance claims

• Intrabar motion reminder. Shapes can move while a bar forms and settle on close

• Strategies must use standard candles for signals and orders

Honest limitations and failure modes

• High impact releases and thin liquidity can distort wicks and produce gaps that any smoother cannot predict

• Very quiet regimes can reduce contrast. Consider longer body length

• Session time on the chart controls the definition of each bar

EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

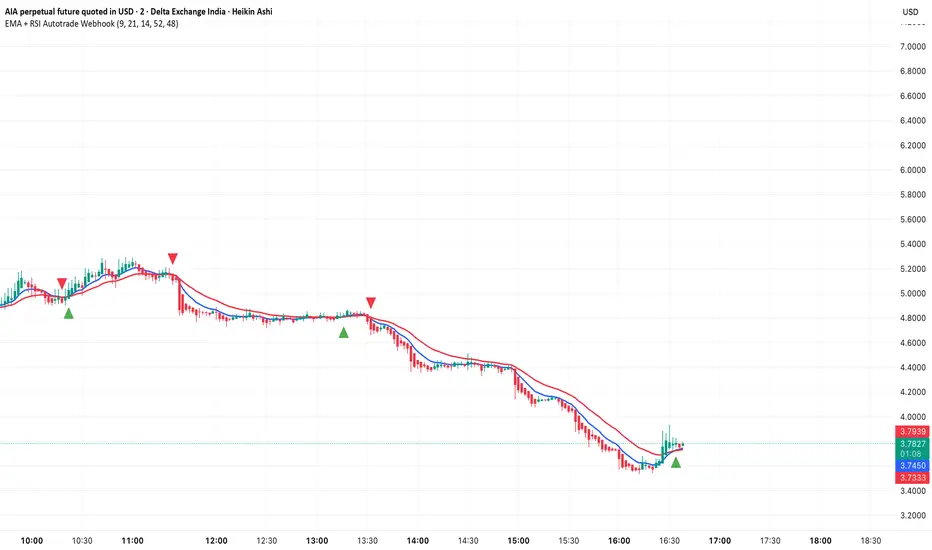

EMA + RSI Autotrade Webhook - VarunOverview

The EMA + RSI Autotrade Webhook is a powerful trend-following indicator designed for automated crypto futures trading. This indicator combines the reliability of Exponential Moving Average (EMA) crossovers with RSI momentum filtering to generate high-probability buy and sell signals optimized for webhook integration with crypto exchanges like Delta Exchange, Binance Futures, and Bybit.Key Features

Simple & Effective: Uses proven EMA 9/21 crossover strategy

RSI Momentum Filter: Eliminates low-probability trades in ranging markets

Webhook Ready: Two clean alerts (LONG Entry, SHORT Entry) for seamless automation

Exchange Compatible: Works with Delta Exchange, 3Commas, Alertatron, and other webhook platforms

Zero Lag Signals: Real-time alerts on crossover confirmation

Visual Clarity: Clean chart markers for easy signal identification

How It Works

Entry Signals:

LONG Entry: Triggers when EMA 9 crosses above EMA 21 AND RSI is above 52 (bullish momentum confirmed)

SHORT Entry: Triggers when EMA 9 crosses under EMA 21 AND RSI is below 48 (bearish momentum confirmed)

Technical Components:

Fast EMA: 9-period (tracks short-term price action)

Slow EMA: 21-period (identifies primary trend)

RSI: 14-period (confirms momentum strength)

RSI Long Threshold: 52 (filters weak bullish signals)

RSI Short Threshold: 48 (filters weak bearish signals)

Best Use Cases

Crypto Futures Trading: Bitcoin, Ethereum, Altcoin perpetual contracts

Automated Trading Bots: Integration with Delta Exchange webhooks, TradingView alerts

Timeframes: Optimized for 15-minute charts (works on 5min-1H)

Markets: Trending crypto markets with clear directional moves

Risk Management: Best used with 1-2% stop loss per trade (managed externally)

Webhook Automation Setup

Add indicator to your TradingView chart

Create alerts for "LONG Entry" and "SHORT Entry"

Configure webhook URL from your exchange (Delta Exchange, Binance, etc.)

Use alert message: Entry LONG {{ticker}} @ {{close}} or Entry SHORT {{ticker}} @ {{close}}

Exchange automatically reverses positions on opposite signals

Advantages

✅ No manual trading required - fully automated

✅ Eliminates emotional trading decisions

✅ Catches trending moves early with EMA crossovers

✅ RSI filter reduces whipsaws in choppy markets

✅ Works 24/7 without monitoring

✅ Simple two-alert system (easy to manage)

✅ Compatible with multiple exchanges via webhooksStrategy Philosophy

This indicator follows a trend-following with momentum confirmation approach. By waiting for both EMA crossover AND RSI confirmation, it ensures you're entering trades with genuine momentum behind them, not just random price noise. The tight RSI thresholds (52/48) keep you aligned with the prevailing trend.Recommended Settings

Timeframe: 15-minute (primary), 5-minute (scalping), 1-hour (swing)

Markets: BTC/USDT, ETH/USDT, high-liquidity altcoin perpetuals

Position Sizing: 100% capital per signal (exchange manages reversals)

Stop Loss: 2% (managed via exchange or external bot)

Leverage: 1-2x for conservative approach, up to 5x for aggressive

Important Notes

⚠️ This indicator generates entry signals only - position reversals are handled automatically by your exchange

⚠️ Always backtest on historical data before live trading

⚠️ Use proper risk management and position sizing

⚠️ Best performance in trending markets; may generate false signals in tight ranges

⚠️ Requires TradingView Premium or higher for webhook functionalityTags

cryptocurrency futures automated-trading ema-crossover rsi webhook delta-exchange tradingview-alerts trend-following momentum bitcoin ethereum crypto-bot algo-trading 15-minute-strategy

Axel AltsOverview

Axel Alts is a higher-timeframe-aware overlay that forms a two-line support band for altcoins using a sticky, threshold-and-step progression. It draws an Upper Support (mid) and a Lower Support (low) derived from evolving local lows, with smoothed transitions and an optional halving-cycle bear-window background.

The goal is disciplined context: identify controlled pullbacks into support in constructive regimes and avoid emotional chasing. All core settings are fixed for consistent behavior across symbols.

Core logic (concepts, not implementation)

• Two baseline levels are computed as fractional distances from the current base and then smoothed.

• A sticky mechanism advances each line toward its target only when deviation is material, and in capped steps. This reduces whipsaw and preserves structure.

• Visual easing smooths transitions so curves remain stable and readable.

• Rendering accounts for higher-timeframe structure and uses interpolation on lower timeframes for visual continuity; values do not look ahead and finalize on higher-timeframe closes.

• An optional bear-window background is derived from halving dates to flag a more cautious phase between the late part of one cycle and the run-up to the next.

Inputs

• Parameters are locked (lengths, fractions, sticky thresholds/steps, easing radii, bear-window bounds). No user-tweakable inputs—this prevents overfitting and improves repeatability.

How to read it

• The zone between Upper Support and Lower Support is the preferred “controlled pullback” area in constructive regimes.

• Persistent closes above Upper Support indicate strength; orderly reactions into the band can be constructive.

• Sustained closes below Lower Support warn of deterioration; be cautious with aggressive longs until recovery.

• The bear-window background suggests a more conservative stance on risk and size.

• Confirmations are best taken on daily/weekly closes; short-term pokes through the band are often noise.

Practical use cases

• Altcoin rotation: prioritize names holding the band; de-prioritize those persisting below it.

• Dollar-Cost Averaging (DCA) context: scale within the band during favorable regimes.

• Risk framing: tighten or reduce exposure on breaks below Lower Support or during the bear window.

• Confluence: combine with volume/volatility tools and market-wide risk gauges.

Best practices

• Rely on daily/weekly closes for confirmation.

• Pair with market structure (HH/HL vs. LH/LL) and higher-timeframe support/resistance.

• Consider broader cycle context (e.g., halving windows) before scaling risk.

Technical notes

• Non-repainting: values finalize on the close of the higher timeframe used by each calculation.

• Interpolation on lower timeframes is for continuity only; it is not forward-looking.

• Bear-window boundaries are fixed and derived from publicly known Bitcoin halving dates.

• The fill between lines is fixed in the current configuration.

Who it is for

• Traders who want a fixed-rules, repeatable context for alt pullbacks and trend health.

• Systematic users who prefer deterministic, non-tunable overlays for portfolio discipline.

Limitations & disclosures

• Closed-source; for educational and analytical use only.

• Not financial advice. Markets involve risk; past performance does not guarantee future results.

Release notes

• Includes sticky progression for both support lines with eased transitions.

• Improved visual continuity on lower timeframes while respecting higher-timeframe structure.

• Added halving-based bear-window highlighting (bounds are fixed).

Originality & why closed-source

This is not a reimplementation of public open-source scripts. Axel Alts integrates (1) sticky threshold-and-step progression, (2) dual support lines built from fractional levels off evolving lows with separate smoothing, (3) visual easing for stability, and (4) a halving-based bear window. The interaction of thresholds/steps, smoothing, and the regime window is proprietary and tuned to retain structure while limiting lag. The source is closed to protect this implementation.

Integration, not a mashup

Axel Alts is a single, self-contained framework. It does not merely merge indicators; its components are designed to work together to form a unified support band with a clear reading protocol (hold within the band, caution below, close-based confirmations, optional bear-window context).

Indicator, not a strategy

This publication is an indicator overlay, not a trading strategy. It includes no backtests, position logic, performance claims, or risk assumptions. Use it as analytical context within your own risk management.

Comparison to common tools

Compared to standard moving-average channels or volatility bands, Axel Alts emphasizes (1) structure retention via sticky thresholds/steps, (2) smoother visuals through eased transitions, and (3) explicit cycle context via the halving-based bear window.

Bull Bear Indicator# Bull Bear Indicator - TradingView Script Description

## Overview

The Bull Bear Indicator is a powerful visual tool that instantly identifies market sentiment by coloring all candlesticks based on their position relative to a moving average. This indicator helps traders quickly identify bullish and bearish market conditions at a glance.

## Key Features

### 🎨 Visual Bull/Bear Identification

- **Green Candles**: Price is at or above the moving average (Bullish condition)

- **Red Candles**: Price is below the moving average (Bearish condition)

- Complete candle coloring including body, wicks, and borders for maximum clarity

### 📊 Flexible Moving Average Options

- **MA Type**: Choose between Simple Moving Average (MA) or Exponential Moving Average (EMA)

- **Timeframe**: Select Weekly or Daily timeframe for the moving average calculation

- **Customizable Period**: Adjust the MA/EMA period (default: 50)

### 📈 Smooth Moving Average Line

- Displays a smooth blue moving average line on the chart

- Automatically adapts to your selected timeframe and MA type

- Provides clear visual reference for trend identification

## How It Works

The indicator calculates a moving average (MA or EMA) based on your selected timeframe (Weekly or Daily). It then compares the current price to this moving average:

- **Bull Market**: When price ≥ Moving Average → Candles turn **GREEN**

- **Bear Market**: When price < Moving Average → Candles turn **RED**

## Configuration Options

1. **MA Type**: Choose "MA" for Simple Moving Average or "EMA" for Exponential Moving Average

2. **Timeframe**: Select "Weekly" for weekly-based MA or "Daily" for daily-based MA

3. **MA Period**: Set the number of periods for the moving average calculation (default: 50)

## Use Cases

- **Trend Identification**: Quickly identify overall market trend direction

- **Entry/Exit Signals**: Use color changes as potential entry or exit signals

- **Multi-Timeframe Analysis**: Combine with different chart timeframes for comprehensive analysis

- **Visual Clarity**: Reduce chart clutter while maintaining essential trend information

## Best Practices

- Use Weekly MA for longer-term trend identification

- Use Daily MA for shorter-term trend analysis

- Combine with other technical indicators for confirmation

- Adjust the MA period based on your trading style and timeframe

## Technical Details

- Built with Pine Script v6

- Overlay indicator (displays on main chart)

- Optimized for performance

- Compatible with all TradingView chart types

---

**Note**: This indicator is for educational and informational purposes only. Always conduct your own analysis and risk management before making trading decisions.

TPAmacd — Free by TPA OG💎 TPAmacd — Free by TPA OG

Professional Divergence Detection for Confident Technical Analysis

🧭 Overview

TPAmacd is an advanced divergence-analysis tool built for traders who value precision, adaptability, and clarity.

It automatically identifies bullish and bearish divergences on the MACD histogram, confirms momentum shifts, and provides a clean, customizable visual framework — helping you interpret market transitions with greater confidence.

⚙️ Key Features

- Auto-detected Bullish / Bearish Divergences — instantly highlights potential momentum shifts.

- Multi-Timeframe Compatibility — analyze divergences seamlessly across any chart period.

- Histogram Reversal Alerts — get notified as momentum changes direction.

- Customizable Settings — choose between EMA / SMA, set color themes, and adjust visual precision.

- Efficient, Lightweight Design — optimized for clarity and performance on all devices.

📈 Why Traders Choose TPAmacd

- Professional-grade divergence mapping

- Intuitive design — minimal clutter, maximum context

- Adaptable for scalping, swing, or long-term analysis

- Clear alerts and smooth integration with your workflow

⚠️ Important Disclaimer

This script is provided for educational and informational purposes only.

It does not constitute financial, investment, or trading advice.

No indicator, including TPAmacd or any related tools by TPA OG, can guarantee accuracy or profitability.

All trading involves risk, and past performance is not indicative of future results.

Always perform independent analysis and use appropriate risk-management practices before placing any trade.

Crypto Breadth Engine [alex975]

A normalized crypto market breadth indicator with a customizable 40 coin input panel — revealing whether rallies are broad and healthy across major coins and altcoins or led by only a few.

📊 Overview

The Crypto Breadth Engine measures the real participation strength of the crypto market by analyzing the direction of the 40 largest cryptocurrencies by market capitalization.

⚙️ How It Works

Unlike standard breadth tools that only count assets above a moving average, this indicator measures actual price direction:

+1 if a coin closes higher, –1 if lower, 0 if unchanged.

The total forms a Breadth Line, statistically normalized using standard deviation to maintain consistent readings across timeframes and volatility conditions.

🧩 Dynamic Input Mask

All 40 cryptocurrencies are fully editable via the input panel, allowing users to easily replace or customize the basket (Top 40, Layer-1s, DeFi, Meme Coins, AI Tokens, etc.) without touching the code.

This flexibility keeps the indicator aligned with the evolving crypto market.

🧭 Trend Bias

The indicator classifies market structure as Bullish, Neutral, or Bearish, based on how the Breadth Line aligns with its moving averages (10, 20, 50).

💡 Dashboard

A compact on-chart table displays in real time:

• Positive and negative coins

• Participation percentage

• Current trend bias

🔍 Interpretation

• Rising breadth → broad, healthy market expansion

• Falling breadth → narrowing participation and structural weakness

Ideal for TOTAL, TOTAL3, or custom crypto baskets on 1D,1W.

Developed by alex975 – Version 1.0 (2025).

-------------------------------------------------------------------------------------

🇮🇹 Versione Italiana

📊 Panoramica

Il Crypto Breadth Engine misura la partecipazione reale del mercato crypto, analizzando la direzione delle 40 principali criptovalute per capitalizzazione.

Non si limita a contare quante coin sono sopra una media mobile, ma calcola la variazione effettiva del prezzo:

+1 se sale, –1 se scende, 0 se invariato.

La somma genera una Breadth Line normalizzata statisticamente, garantendo letture coerenti su diversi timeframe e fasi di volatilità.

🧩 Mascherina dinamica

L’indicatore include una mascherina d’input interattiva che consente di modificare o sostituire liberamente i 40 ticker analizzati (Top 40, Layer-1, DeFi, Meme Coin, ecc.) senza intervenire nel codice.

Questo lo rende sempre aggiornato e adattabile all’evoluzione del mercato crypto.

⚙️ Funzionamento e Trend Bias

Classifica automaticamente il mercato come Bullish, Neutral o Bearish in base alla relazione tra la breadth e le medie mobili (10, 20, 50 periodi).

💡 Dashboard

Una tabella compatta mostra in tempo reale:

• Numero di coin positive e negative

• Percentuale di partecipazione

• Stato attuale del trend

🔍 Interpretazione

• Breadth in crescita → mercato ampio e trend sano

• Breadth in calo → partecipazione ridotta e concentrazione su pochi asset

Ideale per analizzare TOTAL, TOTAL3 o panieri personalizzati di crypto.

Funziona su timeframe 1D, 4H, 1W.

Sviluppato da alex975 – Versione 1.0 (2025).

Grizzly Brahman · PRO SCALPERGrizzly Brahman TMAX 4 is a fourth-generation Trend-Momentum-Adaptive Crossover system built to identify true intraday direction and volatility alignment before price acceleration begins.

It combines adaptive moving-average bands, momentum filtration, and trend-fill logic to produce crystal-clear long/short zones directly on the chart.

Preset Modes

“Aggressive / Balanced / Disciplined” presets optimize responsiveness for scalping, intra-day, or swing conditions.

Session Shading & ORB Levels

Optional overlays for Opening Range Breakout, Pre-Market High/Low, and Previous Day High/Low to frame liquidity targets.

Heikin Ashi Compatibility

Optimized to read momentum flow cleanly on Heikin Ashi charts for false-breakout filtering.

Momentum Bands

Adaptive outer bands act as over-extension or “take-profit” zones — similar to ATR channels but smoothed for consistency.

How to Use

Identify Trend Zone — watch for color fill change and TMA alignment.

Enter on Marker Confirmation — green triangle = long momentum confirm, red triangle = short.

Manage Risk around outer TMA/ATR band touches or when color intensity fades.