Asian & London Session Highs/LowsAsian & London Session Highs/Lows with Extendable Lines

This TradingView script automatically marks the highs and lows of the Asian and London trading sessions for the most recent day, allowing traders to identify key levels during these active periods. The lines representing the high and low of each session are drawn at the exact price point where the high/low occurred, and they extend to the right for a customizable number of bars, helping to visualize how the price reacts to these key levels after the session ends.

Key Features:

Session High/Low Tracking: Automatically tracks the highest and lowest points for the Asian and London sessions.

Extendable Lines: Lines start at the exact bar where the high/low occurred and can be extended to the right for a specified number of bars.

Timezone Adjustment: Allows you to input a timezone offset to adjust session times based on your local time or desired market time zone.

Customizable Colors & Line Thickness: Adjust the color and thickness of the session high and low lines to suit your visual preferences.

Clear & Precise Levels: Helps identify important support and resistance levels, making it easier to spot market reactions around session highs and lows.

This indicator is perfect for day traders and those looking to trade during specific market hours, offering clear visual markers of session boundaries and critical price levels.

Cari dalam skrip untuk "track"

Dskyz (DAFE) Adaptive Regime - Quant Machine ProDskyz (DAFE) Adaptive Regime - Quant Machine Pro:

Buckle up for the Dskyz (DAFE) Adaptive Regime - Quant Machine Pro, is a strategy that’s your ultimate edge for conquering futures markets like ES, MES, NQ, and MNQ. This isn’t just another script—it’s a quant-grade powerhouse, crafted with precision to adapt to market regimes, deliver multi-factor signals, and protect your capital with futures-tuned risk management. With its shimmering DAFE visuals, dual dashboards, and glowing watermark, it turns your charts into a cyberpunk command center, making trading as thrilling as it is profitable.

Unlike generic scripts clogging up the space, the Adaptive Regime is a DAFE original, built from the ground up to tackle the chaos of futures trading. It identifies market regimes (Trending, Range, Volatile, Quiet) using ADX, Bollinger Bands, and HTF indicators, then fires trades based on a weighted scoring system that blends candlestick patterns, RSI, MACD, and more. Add in dynamic stops, trailing exits, and a 5% drawdown circuit breaker, and you’ve got a system that’s as safe as it is aggressive. Whether you’re a newbie or a prop desk pro, this strat’s your ticket to outsmarting the markets. Let’s break down every detail and see why it’s a must-have.

Why Traders Need This Strategy

Futures markets are a gauntlet—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional traps that punish the unprepared. Meanwhile, platforms are flooded with low-effort scripts that recycle old ideas with zero innovation. The Adaptive Regime stands tall, offering:

Adaptive Intelligence: Detects market regimes (Trending, Range, Volatile, Quiet) to optimize signals, unlike one-size-fits-all scripts.

Multi-Factor Precision: Combines candlestick patterns, MA trends, RSI, MACD, volume, and HTF confirmation for high-probability trades.

Futures-Optimized Risk: Calculates position sizes based on $ risk (default: $300), with ATR or fixed stops/TPs tailored for ES/MES.

Bulletproof Safety: 5% daily drawdown circuit breaker and trailing stops keep your account intact, even in chaos.

DAFE Visual Mastery: Pulsing Bollinger Band fills, dynamic SL/TP lines, and dual dashboards (metrics + position) make signals crystal-clear and charts a work of art.

Original Craftsmanship: A DAFE creation, built with community passion, not a rehashed clone of generic code.

Traders need this because it’s a complete, adaptive system that blends quant smarts, user-friendly design, and DAFE flair. It’s your edge to trade with confidence, cut through market noise, and leave the copycats in the dust.

Strategy Components

1. Market Regime Detection

The strategy’s brain is its ability to classify market conditions into five regimes, ensuring signals match the environment.

How It Works:

Trending (Regime 1): ADX > 20, fast/slow EMA spread > 0.3x ATR, HTF RSI > 50 or MACD bullish (htf_trend_bull/bear).

Range (Regime 2): ADX < 25, price range < 3% of close, no HTF trend.

Volatile (Regime 3): BB width > 1.5x avg, ATR > 1.2x avg, HTF RSI overbought/oversold.

Quiet (Regime 4): BB width < 0.8x avg, ATR < 0.9x avg.

Other (Regime 5): Default for unclear conditions.

Indicators: ADX (14), BB width (20), ATR (14, 50-bar SMA), HTF RSI (14, daily default), HTF MACD (12,26,9).

Why It’s Brilliant:

Regime detection adapts signals to market context, boosting win rates in trending or volatile conditions.

HTF RSI/MACD add a big-picture filter, rare in basic scripts.

Visualized via gradient background (green for Trending, orange for Range, red for Volatile, gray for Quiet, navy for Other).

2. Multi-Factor Signal Scoring

Entries are driven by a weighted scoring system that combines candlestick patterns, trend, momentum, and volume for robust signals.

Candlestick Patterns:

Bullish: Engulfing (0.5), hammer (0.4 in Range, 0.2 else), morning star (0.2), piercing (0.2), double bottom (0.3 in Volatile, 0.15 else). Must be near support (low ≤ 1.01x 20-bar low) with volume spike (>1.5x 20-bar avg).

Bearish: Engulfing (0.5), shooting star (0.4 in Range, 0.2 else), evening star (0.2), dark cloud (0.2), double top (0.3 in Volatile, 0.15 else). Must be near resistance (high ≥ 0.99x 20-bar high) with volume spike.

Logic: Patterns are weighted higher in specific regimes (e.g., hammer in Range, double bottom in Volatile).

Additional Factors:

Trend: Fast EMA (20) > slow EMA (50) + 0.5x ATR (trend_bull, +0.2); opposite for trend_bear.

RSI: RSI (14) < 30 (rsi_bull, +0.15); > 70 (rsi_bear, +0.15).

MACD: MACD line > signal (12,26,9, macd_bull, +0.15); opposite for macd_bear.

Volume: ATR > 1.2x 50-bar avg (vol_expansion, +0.1).

HTF Confirmation: HTF RSI < 70 and MACD bullish (htf_bull_confirm, +0.2); RSI > 30 and MACD bearish (htf_bear_confirm, +0.2).

Scoring:

bull_score = sum of bullish factors; bear_score = sum of bearish. Entry requires score ≥ 1.0.

Example: Bullish engulfing (0.5) + trend_bull (0.2) + rsi_bull (0.15) + htf_bull_confirm (0.2) = 1.05, triggers long.

Why It’s Brilliant:

Multi-factor scoring ensures signals are confirmed by multiple market dynamics, reducing false positives.

Regime-specific weights make patterns more relevant (e.g., hammers shine in Range markets).

HTF confirmation aligns with the big picture, a quant edge over simplistic scripts.

3. Futures-Tuned Risk Management

The risk system is built for futures, calculating position sizes based on $ risk and offering flexible stops/TPs.

Position Sizing:

Logic: Risk per trade (default: $300) ÷ (stop distance in points * point value) = contracts, capped at max_contracts (default: 5). Point value = tick value (e.g., $12.5 for ES) * ticks per point (4) * contract multiplier (1 for ES, 0.1 for MES).

Example: $300 risk, 8-point stop, ES ($50/point) → 0.75 contracts, rounded to 1.

Impact: Precise sizing prevents over-leverage, critical for micro contracts like MES.

Stops and Take-Profits:

Fixed: Default stop = 8 points, TP = 16 points (2:1 reward/risk).

ATR-Based: Stop = 1.5x ATR (default), TP = 3x ATR, enabled via use_atr_for_stops.

Logic: Stops set at swing low/high ± stop distance; TPs at 2x stop distance from entry.

Impact: ATR stops adapt to volatility, while fixed stops suit stable markets.

Trailing Stops:

Logic: Activates at 50% of TP distance. Trails at close ± 1.5x ATR (atr_multiplier). Longs: max(trail_stop_long, close - ATR * 1.5); shorts: min(trail_stop_short, close + ATR * 1.5).

Impact: Locks in profits during trends, a game-changer in volatile sessions.

Circuit Breaker:

Logic: Pauses trading if daily drawdown > 5% (daily_drawdown = (max_equity - equity) / max_equity).

Impact: Protects capital during black swan events (e.g., April 27, 2025 ES slippage).

Why It’s Brilliant:

Futures-specific inputs (tick value, multiplier) make it plug-and-play for ES/MES.

Trailing stops and circuit breaker add pro-level safety, rare in off-the-shelf scripts.

Flexible stops (ATR or fixed) suit different trading styles.

4. Trade Entry and Exit Logic

Entries and exits are precise, driven by bull_score/bear_score and protected by drawdown checks.

Entry Conditions:

Long: bull_score ≥ 1.0, no position (position_size <= 0), drawdown < 5% (not pause_trading). Calculates contracts, sets stop at swing low - stop points, TP at 2x stop distance.

Short: bear_score ≥ 1.0, position_size >= 0, drawdown < 5%. Stop at swing high + stop points, TP at 2x stop distance.

Logic: Tracks entry_regime for PNL arrays. Closes opposite positions before entering.

Exit Conditions:

Stop-Loss/Take-Profit: Hits stop or TP (strategy.exit).

Trailing Stop: Activates at 50% TP, trails by ATR * 1.5.

Emergency Exit: Closes if price breaches stop (close < long_stop_price or close > short_stop_price).

Reset: Clears stop/TP prices when flat (position_size = 0).

Why It’s Brilliant:

Score-based entries ensure multi-factor confirmation, filtering out weak signals.

Trailing stops maximize profits in trends, unlike static exits in basic scripts.

Emergency exits add an extra safety layer, critical for futures volatility.

5. DAFE Visuals

The visuals are pure DAFE magic, blending function with cyberpunk flair to make signals intuitive and charts stunning.

Shimmering Bollinger Band Fill:

Display: BB basis (20, white), upper/lower (green/red, 45% transparent). Fill pulses (30–50 alpha) by regime, with glow (60–95 alpha) near bands (close ≥ 0.995x upper or ≤ 1.005x lower).

Purpose: Highlights volatility and key levels with a futuristic glow.

Visuals make complex regimes and signals instantly clear, even for newbies.

Pulsing effects and regime-specific colors add a DAFE signature, setting it apart from generic scripts.

BB glow emphasizes tradeable levels, enhancing decision-making.

Chart Background (Regime Heatmap):

Green — Trending Market: Strong, sustained price movement in one direction. The market is in a trend phase—momentum follows through.

Orange — Range-Bound: Market is consolidating or moving sideways, with no clear up/down trend. Great for mean reversion setups.

Red — Volatile Regime: High volatility, heightened risk, and larger/faster price swings—trade with caution.

Gray — Quiet/Low Volatility: Market is calm and inactive, with small moves—often poor conditions for most strategies.

Navy — Other/Neutral: Regime is uncertain or mixed; signals may be less reliable.

Bollinger Bands Glow (Dynamic Fill):

Neon Red Glow — Warning!: Price is near or breaking above the upper band; momentum is overstretched, watch for overbought conditions or reversals.

Bright Green Glow — Opportunity!: Price is near or breaking below the lower band; market could be oversold, prime for bounce or reversal.

Trend Green Fill — Trending Regime: Fills between bands with green when the market is trending, showing clear momentum.

Gold/Yellow Fill — Range Regime: Fills with gold/aqua in range conditions, showing the market is sideways/oscillating.

Magenta/Red Fill — Volatility Spike: Fills with vivid magenta/red during highly volatile regimes.

Blue Fill — Neutral/Quiet: A soft blue glow for other or uncertain market states.

Moving Averages:

Display: Blue fast EMA (20), red slow EMA (50), 2px.

Purpose: Shows trend direction, with trend_dir requiring ATR-scaled spread.

Dynamic SL/TP Lines:

Display: Pulsing colors (red SL, green TP for Trending; yellow/orange for Range, etc.), 3px, with pulse_alpha for shimmer.

Purpose: Tracks stops/TPs in real-time, color-coded by regime.

6. Dual Dashboards

Two dashboards deliver real-time insights, making the strat a quant command center.

Bottom-Left Metrics Dashboard (2x13):

Metrics: Mode (Active/Paused), trend (Bullish/Bearish/Neutral), ATR, ATR avg, volume spike (YES/NO), RSI (value + Oversold/Overbought/Neutral), HTF RSI, HTF trend, last signal (Buy/Sell/None), regime, bull score.

Display: Black (29% transparent), purple title, color-coded (green for bullish, red for bearish).

Purpose: Consolidates market context and signal strength.

Top-Right Position Dashboard (2x7):

Metrics: Regime, position side (Long/Short/None), position PNL ($), SL, TP, daily PNL ($).

Display: Black (29% transparent), purple title, color-coded (lime for Long, red for Short).

Purpose: Tracks live trades and profitability.

Why It’s Brilliant:

Dual dashboards cover market context and trade status, a rare feature.

Color-coding and concise metrics guide beginners (e.g., green “Buy” = go).

Real-time PNL and SL/TP visibility empower disciplined trading.

7. Performance Tracking

Logic: Arrays (regime_pnl_long/short, regime_win/loss_long/short) track PNL and win/loss by regime (1–5). Updated on trade close (barstate.isconfirmed).

Purpose: Prepares for future adaptive thresholds (e.g., adjust bull_score min based on regime performance).

Why It’s Brilliant: Lays the groundwork for self-optimizing logic, a quant edge over static scripts.

Key Features

Regime-Adaptive: Optimizes signals for Trending, Range, Volatile, Quiet markets.

Futures-Optimized: Precise sizing for ES/MES with tick-based risk inputs.

Multi-Factor Signals: Candlestick patterns, RSI, MACD, and HTF confirmation for robust entries.

Dynamic Exits: ATR/fixed stops, 2:1 TPs, and trailing stops maximize profits.

Safe and Smart: 5% drawdown breaker and emergency exits protect capital.

DAFE Visuals: Shimmering BB fill, pulsing SL/TP, and dual dashboards.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

How to Use

Add to Chart: Load on a 5min ES/MES chart in TradingView.

Configure Inputs: Set instrument (ES/MES), tick value ($12.5/$1.25), multiplier (1/0.1), risk ($300 default). Enable ATR stops for volatility.

Monitor Dashboards: Bottom-left for regime/signals, top-right for position/PNL.

Backtest: Run in strategy tester to compare regimes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see regime shifts and stops.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance does not guarantee future results. Backtest results may differ from live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Slippage: 3

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Adaptive Regime - Quant Machine Pro is more than a strategy—it’s a revolution. Crafted with DAFE’s signature precision, it rises above generic scripts with adaptive regimes, quant-grade signals, and visuals that make trading a thrill. Whether you’re scalping MES or swinging ES, this system empowers you to navigate markets with confidence and style. Join the DAFE crew, light up your charts, and let’s dominate the futures game!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

ULTIMATE Price Action Oscillator with Volume-Based S/R - MehtaULTIMATE Price Action Oscillator with Volume-Based S/R (UPO-PRO-VOL)

Key Features:

Smart Oscillator: Combines price action momentum with customizable smoothing.

Volume-Confirmed S/R: Identifies high-confidence Support/Resistance levels when price crosses above-average volume.

Real-Time Tracking: Displays S/R levels with timestamps (IST) in a clean table.

Visual Alerts: Dashed lines + labels mark key levels for easy spotting.

⚠️ STRONG DISCLAIMER

❌ This indicator is for educational purposes only.

❌ Not financial advice. Trading involves risk—always conduct your own analysis.

❌ No guarantee of accuracy. Past performance ≠ future results.

❌ Adjust settings carefully. Test in a demo account first.

❌ Volume thresholds may vary by asset. Customize Volume Threshold Multiplier as needed.

📝 How to Use:

S/R Signals: Green "S" = Support (oscillator crosses up with high volume). Red "R" = Resistance (oscillator crosses down with high volume).

Table: Tracks latest S/R prices and formation time (IST).

Tweak Settings: Adjust Oscillator Length, Smoothing, and Volume Threshold for your trading style.

Tip: Combine with trend analysis for higher-probability trades!

Script Settings (Default):

Oscillator Length: 5 (Can be adjusted upto a maximum value of 200)

Smoothing: 3

S/R Lookback: 100 bars

Volume Threshold: 1.5x avg volume

GRASS Purple Cloud [MMD] MTFThis Pine Script code is a trading strategy designed for use on the TradingView platform. It implements a multi-timeframe (MTF) strategy called "GRASS Purple Cloud " that utilizes various technical indicators to generate buy and sell signals. Below is a breakdown of the key components of the script:

Key Components of the Strategy

Inputs:

HTF (Higher Time Frame): Allows the user to select a higher time frame for analysis.

ATR and Supertrend Parameters: Inputs for the Average True Range (ATR) and Supertrend indicator, which are used to determine market volatility and trend direction.

Buying and Selling Pressure Thresholds: These thresholds help define conditions for entering trades based on buying and selling pressure.

Backtest Date Range: Users can specify a date range for backtesting the strategy.

HTF Logic:

The htfLogic function calculates various values based on the selected higher time frame, including buying and selling conditions, which are then used to generate signals.

Signal State Tracking:

The script tracks the state of buy and sell signals using a variable xs, which changes based on the conditions defined in the htfLogic function.

Coloring and Labels:

The bars on the chart are colored green for buy signals and red for sell signals. Additionally, labels are plotted to indicate strong buy and sell signals.

EMA Plotting:

The script includes optional plotting of Exponential Moving Averages (EMAs) for 20, 50, and 200 periods, which can help traders identify trends.

Trade Management:

The strategy includes parameters for take profit (TP) and stop loss (SL) levels, allowing for risk management. The user can specify the percentage for TP and SL, as well as the number of units to sell at each level.

Entries and Exits:

The script defines conditions for entering long and short positions based on the buy and sell signals. It also manages exits based on TP and SL levels.

Trendline Logic:

The script identifies the last two significant highs to draw a trendline, which can help visualize market structure.

TP/SL Plotting:

The script plots the TP and SL levels on the chart for visual reference.

Reset After Exit:

After a trade is closed, the script resets the relevant variables to prepare for the next trade.

Usage

To use this strategy:

Adjust the input parameters as needed for your trading preferences.

Add the strategy to a chart to visualize the signals and performance.

Considerations

As with any trading strategy, it's essential to backtest and validate the performance over historical data before using it in live trading.

Market conditions can change, and past performance is not indicative of future results. Always use risk management practices when trading.

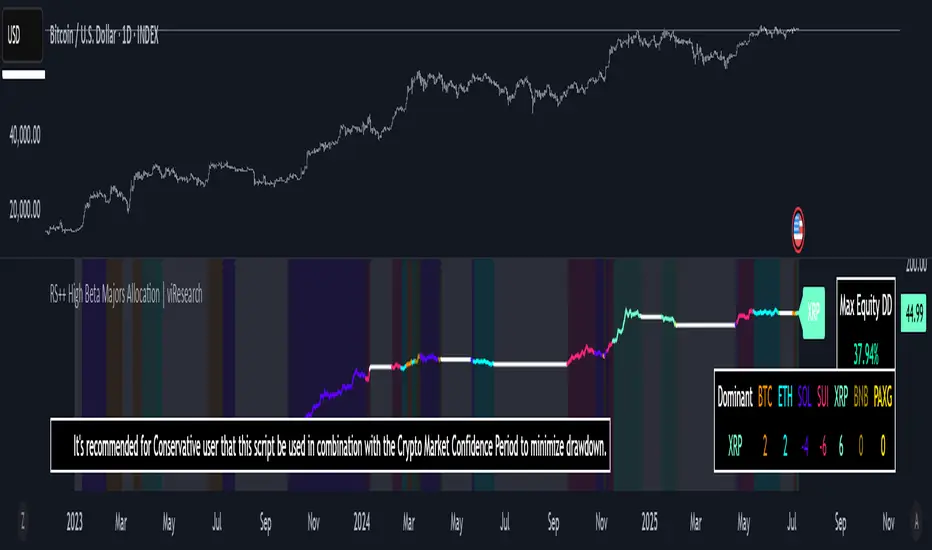

RS++ High Beta Majors Allocation | viResearchRS++ High Beta Majors Allocation | viResearch

Conceptual Foundation and Innovation

The "RS++ High Beta Majors Allocation" is a next-generation portfolio rotation algorithm designed to capture alpha from high-volatility (high-beta) crypto assets. Building on the RS+ framework, this strategy expands the asset pool beyond BTC, ETH, and SOL to include newer and more volatile contenders like SUI and XRP. The goal is to rotate dynamically among these five majors—allocating to the strongest trending asset while minimizing exposure during broad-market weakness.

The strategy introduces enhanced comparative scoring using a multi-layered relative strength matrix that accounts for cross-asset momentum in real-time. Combined with a regime-based trend filter, it adapts not only to market leadership but also to prevailing risk conditions, significantly improving capital efficiency over traditional buy-and-hold strategies.

Technical Composition and Calculation

At the heart of the RS++ model lies a sophisticated five-asset ratio matrix. Each asset is evaluated against the others using relative price ratios, and each pair is scored through a hybrid strength model based on universal trend filters and statistical thresholds.

Expanded Universe: The script evaluates BTC, ETH, SOL, SUI, and XRP—each chosen for their liquidity and volatility profile, enhancing the potential for outperformance.

Relative Strength Matrix: A 5x5 matrix compares all assets against one another to determine momentum dominance. The asset with the highest cumulative score is considered the dominant major.

Trend Regime Filter: Before allocation, both the market regime (via BTC or a custom source) and the individual asset must pass trend confirmation to qualify for inclusion, reducing whipsaw exposure.

Equity Tracking: A real-time system equity line tracks portfolio performance from a custom user-defined start date.

Drawdown Measurement: Maximum drawdown is computed in real-time to assess risk exposure.

Performance Metrics

The script measures key quantitative metrics to evaluate performance robustness:

Max Drawdown: Assesses capital risk and largest equity dip from peak to trough.

Sharpe/Sortino/Omega Ratios (optional in previous versions): Can be adapted for future inclusion.

ROC-Based Returns: Allocation logic and equity growth are tied to ROC (rate of change), making it highly responsive to price action.

User Interface and Features

This version introduces user-centric customization and quality-of-life improvements:

Asset Toggle via Tickers: Simply switch any ticker to "USDT" to exclude it from the rotation universe.

Equity Chart Overlay: Real-time equity plotted with color-coded trend backgrounds for easy interpretation of active holdings.

Dominant Asset Panel: A dashboard displays the currently allocated asset and scores of all assets for comparative insights.

Usage Recommendation: The script includes an embedded suggestion to pair this strategy with the Crypto Market Confidence Period indicator for even better macro-filtering.

Timeframe Guardrail: A soft enforcement feature suggests usage on the 1D timeframe for optimal accuracy.

Practical Applications

This strategy is ideal for traders who prefer a tactical, risk-managed approach to high-beta crypto portfolios. Use cases include:

Active Rotation Management: Switches capital between the strongest trending assets to capture momentum across cycles.

Macro Regime Sensitivity: The trend filter avoids allocation during weak macro trends, moving to cash and preserving equity.

High-Volatility Environments: Particularly effective in bull phases or during sector rotations where traditional assets underperform.

Strategic Value and Advantages

The RS++ script blends alpha-generation with institutional-level risk filtering, making it a powerful tool for active portfolio managers. The expanded universe allows for exposure to emerging market leaders while the scoring and filtering mechanism ensures trades are made with precision. Real-time equity visualization and intuitive alerts help traders stay aligned with system output without constant screen-watching.

Summary and Usage Tips

The "RS++ High Beta Majors Allocation" script offers a versatile and powerful method for crypto portfolio allocation with an emphasis on dynamic strength, risk control, and adaptability. Traders are encouraged to:

Use the recommended 1D timeframe for stability.

Pair the strategy with macro filters like the Crypto Market Confidence Period.

As always, backtest thoroughly and remember that no model guarantees future performance. Use this tool as part of a broader risk-managed trading framework.

Multi-MA Strategy Analyzer with BacktestMulti-MA Strategy Analyzer with Backtest

This TradingView Pine Script indicator is designed to analyze multiple moving averages (SMA or EMA) dynamically and identify the most profitable one based on historical performance.

Features

Dynamic MA Range:

Specify a minLength, maxLength, and step size.

Automatically calculates up to 20 MAs.

Custom MA Calculation:

Uses custom SMA and EMA implementations to support dynamic length values.

Buy/Sell Logic:

Buy when price crosses above a MA.

Sell when price crosses below.

Supports both long and short trades.

Performance Tracking:

Tracks PnL, number of trades, win rate, average profit, and drawdown.

Maintains individual stats for each MA.

Best MA Detection:

Automatically highlights the best-performing MA.

Optional showBestOnly toggle to focus only on the best line and its stats.

Visualization:

Up to 20 plot() calls (static) for MAs.

Green highlight for the best MA.

Color-coded result table and chart.

Table View

When showBestOnly = false, the table displays all MAs with stats.

When showBestOnly = true, the table displays only the best MA with a summary row.

Includes:

Best MA length

Total PnL

Number of trades

Win rate

Avg PnL per trade

Max Drawdown

Configuration

minLength (default: 10)

maxLength (default: 200)

step (default: 10)

useEMA: Toggle between EMA and SMA

showBestOnly: Focus on best-performing MA only

Notes

MA plotting is static, limited to 20 total.

Table supports highlighting and is optimized for performance.

Script is structured to run efficiently using arrays and simple int where required.

Potential Extensions

Add visual buy/sell arrows

Export stats to CSV

Strategy tester conversion

Custom date range filtering for backtesting

Author: Muhammad Wasim

Version: 1.0

Geometric Momentum Breakout with Monte CarloOverview

This experimental indicator uses geometric trendline analysis combined with momentum and Monte Carlo simulation techniques to help visualize potential breakout areas. It calculates support, resistance, and an aggregated trendline using a custom Geo library (by kaigouthro). The indicator also tracks breakout signals in a way that a new buy signal is triggered only after a sell signal (and vice versa), ensuring no repeated signals in the same direction.

Important:

This script is provided for educational purposes only. It is experimental and should not be used for live trading without proper testing and validation.

Key Features

Trendline Calculation:

Uses the Geo library to compute support and resistance trendlines based on historical high and low prices. The midpoint of these trendlines forms an aggregated trendline.

Momentum Analysis:

Computes the Rate of Change (ROC) to determine momentum. Breakout conditions are met only if the price and momentum exceed a user-defined threshold.

Monte Carlo Simulation:

Simulates future price movements to estimate the probability of bullish or bearish breakouts over a specified horizon.

Signal Tracking:

A persistent variable ensures that once a buy (or sell) signal is triggered, it won’t repeat until the opposite signal occurs.

Geometric Enhancements:

Calculates an aggregated trend angle and channel width (distance between support and resistance), and draws a perpendicular “breakout zone” line.

Table Display:

A built-in table displays key metrics including:

Bullish probability

Bearish probability

Aggregated trend angle (in degrees)

Channel width

Alerts:

Configurable alerts notify when a new buy or sell breakout signal occurs.

Inputs

Resistance Lookback & Support Lookback:

Number of bars to look back for determining resistance and support points.

Momentum Length & Threshold:

Period for ROC calculation and the minimum percentage change required for a breakout confirmation.

Monte Carlo Simulation Parameters:

Simulation Horizon: Number of future bars to simulate.

Simulation Iterations: Number of simulation runs.

Table Position & Text Size:

Customize where the table is displayed on the chart and the size of the text.

How to Use

Add the Script to Your Chart:

Copy the code into the Pine Script editor on TradingView and add it to your chart.

Adjust Settings:

Customize the inputs (e.g., lookback periods, momentum threshold, simulation parameters) to fit your analysis or educational requirements.

Interpret Signals:

A buy signal is plotted as a green triangle below the bar when conditions are met and the state transitions from neutral or sell.

A sell signal is plotted as a red triangle above the bar when conditions are met and the state transitions from neutral or buy.

Alerts are triggered only on the bar where a new signal is generated.

Examine the Table:

The table displays key metrics (breakout probabilities, aggregated trend angle, and channel width) to help evaluate current market conditions.

Disclaimer

This indicator is experimental and provided for educational purposes only. It is not intended as a trading signal or financial advice. Use this script at your own risk, and always perform your own research and testing before using any experimental tools in live trading.

Credit

This indicator uses the Geo library by kaigouthro. Special thanks to Cryptonerds and @Hazzantazzan for their contributions and insights.

Shadow Edge (Example)This script tracks hourly price extremes (highs/lows) and their equilibrium (midpoint), plotting them as dynamic reference lines on your chart. It helps visualize intraday support/resistance levels and potential price boundaries.

Key Features

Previous Hour Levels (Static Lines):

PH (Previous Hour High): Red line.

PL (Previous Hour Low): Green line.

P.EQ (Previous Hour Equilibrium): Blue midpoint between PH and PL.

Current Hour Levels (Dynamic/Dotted Lines):

MuEH (Current Hour High): Yellow dashed line (updates in real-time).

MuEL (Current Hour Low): Orange dashed line (updates in real-time).

Labels: Clear text labels on the right edge of the chart for easy readability.

How It Works

Hourly Tracking:

Detects new hours using the hour(time) function.

Resets high/low values at the start of each hour.

Stores the previous hour’s PH, PL, and P.EQ when a new hour begins.

Dynamic Updates:

Continuously updates MuEH and MuEL during the current hour to reflect the latest extremes.

Customization

Toggle visibility of lines via inputs:

Enable/disable PH, PL, P.EQ, MuEH, MuEL individually.

Adjustable colors and line styles (solid for previous hour, dashed for current hour).

Use Case

Intraday Traders: Identify hourly ranges, breakout/retracement opportunities, or mean-reversion setups.

Visual Reference: Quickly see where price is relative to recent hourly activity.

Technical Notes

Overlay: Plots directly on the price chart.

Efficiency: Uses var variables to preserve values between bars.

Labels: Only appear on the latest bar to avoid clutter.

This tool simplifies intraday price action analysis by combining historical and real-time hourly data into a single visual framework.

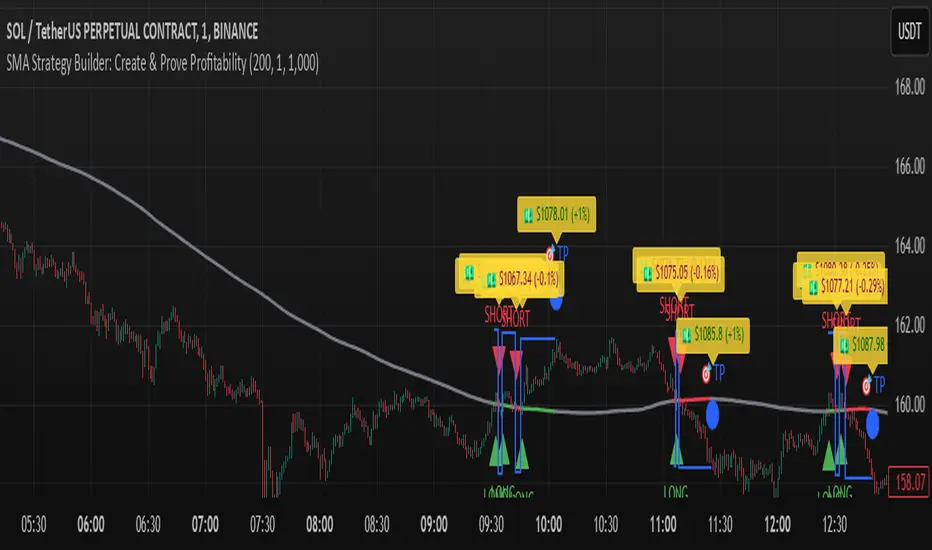

SMA Strategy Builder: Create & Prove Profitability📄 Pine Script Strategy Description (For Publishing on TradingView)

🎯 Strategy Title:

SMA Strategy Builder: Create & Prove Profitability

✨ Description:

This tool is designed for traders who want to build, customize, and prove their own SMA-based trading strategies. The strategy tracks capital growth in real-time, providing clear evidence of profitability after each trade. Users can adjust key parameters such as SMA period, take profit levels, and initial capital, making it a flexible solution for backtesting and strategy validation.

🔍 Key Features:

✅ SMA-Based Logic:

Core trading logic revolves around the Simple Moving Average (SMA).

SMA period is fully adjustable to suit various trading styles.

🎯 Customizable Take Profit (TP):

User-defined TP percentages per position.

TP line displayed as a Step Line with Breaks for clear segmentation.

Visual 🎯TP label for quick identification of profit targets.

💵 Capital Tracking (Proof of Profitability):

Initial capital is user-defined.

Capital balance updates after each closed trade.

Shows both absolute profit/loss and percentage changes for every position.

Darker green profit labels for better readability and dark red for losses.

📈 Capital Curve (Performance Visualization):

Capital growth curve available (hidden by default, can be enabled via settings).

📏 Dynamic Label Positioning:

Label positions adjust dynamically based on the price range.

Ensures consistent visibility across low and high-priced assets.

⚡ How It Works:

Long Entry:

Triggered when the price crosses above the SMA.

TP level is calculated as a user-defined percentage above the entry price.

Short Entry:

Triggered when the price crosses below the SMA.

TP level is calculated as a user-defined percentage below the entry price.

TP Execution:

Positions close immediately once the TP level is reached (no candle close confirmation needed).

🔔 Alerts:

🟩 Long Signal Alert: When the price crosses above the SMA.

🟥 Short Signal Alert: When the price crosses below the SMA.

🎯 TP Alert: When the TP target is reached.

⚙️ Customization Options:

📅 SMA Period: Choose the moving average period that best fits your strategy.

🎯 Take Profit (%): Adjust TP percentages for flexible risk management.

💵 Initial Capital: Set the starting capital for realistic backtesting.

📈 Capital Curve Toggle: Enable or disable the capital curve to track overall performance.

🌟 Why Use This Tool?

🔧 Flexible Strategy Creation: Adjust core parameters and create tailored SMA-based strategies.

📈 Performance Proof: Capital tracking acts as real proof of profitability after each trade.

🎯 Immediate TP Execution: No waiting for candle closures; profits lock in as soon as targets are hit.

💹 Comprehensive Performance Insights: Percentage-based and absolute capital tracking with dynamic visualization.

🏦 Clean Visual Indicators: Strategy insights made clear with dynamic labeling and adjustable visuals.

⚠️ Disclaimer:

This script is provided for educational and informational purposes only. Trading financial instruments carries risk, and past performance does not guarantee future results. Always perform your own due diligence before making any trading decisions.

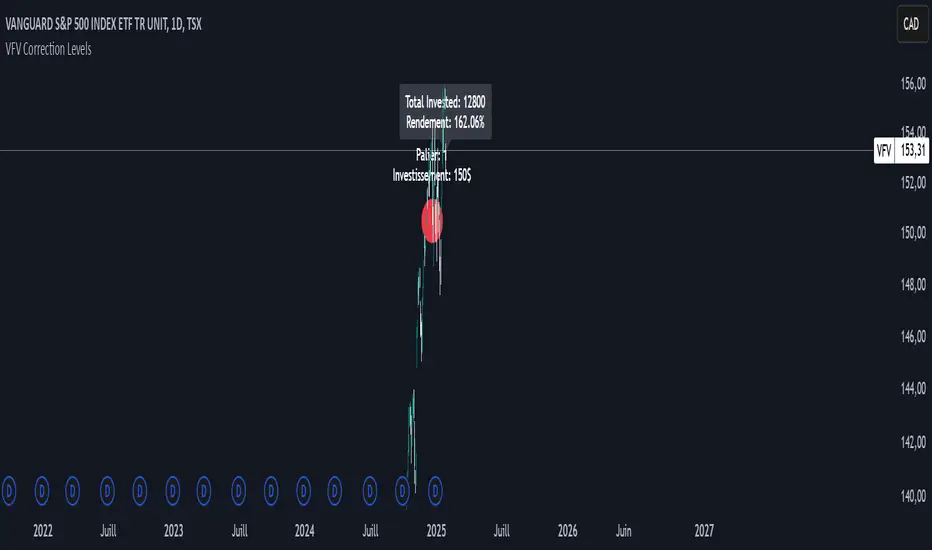

VFV Correction Levels

This Pine Script, "VFV Correction Levels," identifies significant daily price corrections and calculates corresponding investments based on fixed thresholds (paliers). Key features include:

Six predefined correction levels trigger investments between $150 and $600 based on the percentage drop.

Larger corrections correspond to higher investment amounts.

Graphical Indicators:

Visual labels mark correction levels and display investment amounts directly on the chart.

Investment Tracking:

Calculates total invested and tracks performance (yield percentage) relative to the initial correction price.

Sunil BB Blast Heikin Ashi StrategySunil BB Blast Heikin Ashi Strategy

The Sunil BB Blast Heikin Ashi Strategy is a trend-following trading strategy that combines Bollinger Bands with Heikin-Ashi candles for precise market entries and exits. It aims to capitalize on price volatility while ensuring controlled risk through dynamic stop-loss and take-profit levels based on a user-defined Risk-to-Reward Ratio (RRR).

Key Features:

Trading Window:

The strategy operates within a user-defined time window (e.g., from 09:20 to 15:00) to align with market hours or other preferred trading sessions.

Trade Direction:

Users can select between Long Only, Short Only, or Long/Short trade directions, allowing flexibility depending on market conditions.

Bollinger Bands:

Bollinger Bands are used to identify potential breakout or breakdown zones. The strategy enters trades when price breaks through the upper or lower Bollinger Band, indicating a possible trend continuation.

Heikin-Ashi Candles:

Heikin-Ashi candles help smooth price action and filter out market noise. The strategy uses these candles to confirm trend direction and improve entry accuracy.

Risk Management (Risk-to-Reward Ratio):

The strategy automatically adjusts the take-profit (TP) level and stop-loss (SL) based on the selected Risk-to-Reward Ratio (RRR). This ensures that trades are risk-managed effectively.

Automated Alerts and Webhooks:

The strategy includes automated alerts for trade entries and exits. Users can set up JSON webhooks for external execution or trading automation.

Active Position Tracking:

The strategy tracks whether there is an active position (long or short) and only exits when price hits the pre-defined SL or TP levels.

Exit Conditions:

The strategy exits positions when either the take-profit (TP) or stop-loss (SL) levels are hit, ensuring risk management is adhered to.

Default Settings:

Trading Window:

09:20-15:00

This setting confines the strategy to the specified hours, ensuring trading only occurs during active market hours.

Strategy Direction:

Default: Long/Short

This allows for both long and short trades depending on market conditions. You can select "Long Only" or "Short Only" if you prefer to trade in one direction.

Bollinger Band Length (bbLength):

Default: 19

Length of the moving average used to calculate the Bollinger Bands.

Bollinger Band Multiplier (bbMultiplier):

Default: 2.0

Multiplier used to calculate the upper and lower bands. A higher multiplier increases the width of the bands, leading to fewer but more significant trades.

Take Profit Multiplier (tpMultiplier):

Default: 2.0

Multiplier used to determine the take-profit level based on the calculated stop-loss. This ensures that the profit target aligns with the selected Risk-to-Reward Ratio.

Risk-to-Reward Ratio (RRR):

Default: 1.0

The ratio used to calculate the take-profit relative to the stop-loss. A higher RRR means larger profit targets.

Trade Automation (JSON Webhooks):

Allows for integration with external systems for automated execution:

Long Entry JSON: Customizable entry condition for long positions.

Long Exit JSON: Customizable exit condition for long positions.

Short Entry JSON: Customizable entry condition for short positions.

Short Exit JSON: Customizable exit condition for short positions.

Entry Logic:

Long Entry:

The strategy enters a long position when:

The Heikin-Ashi candle shows a bullish trend (green close > open).

The price is above the upper Bollinger Band, signaling a breakout.

The previous candle also closed higher than it opened.

Short Entry:

The strategy enters a short position when:

The Heikin-Ashi candle shows a bearish trend (red close < open).

The price is below the lower Bollinger Band, signaling a breakdown.

The previous candle also closed lower than it opened.

Exit Logic:

Take-Profit (TP):

The take-profit level is calculated as a multiple of the distance between the entry price and the stop-loss level, determined by the selected Risk-to-Reward Ratio (RRR).

Stop-Loss (SL):

The stop-loss is placed at the opposite Bollinger Band level (lower for long positions, upper for short positions).

Exit Trigger:

The strategy exits a trade when either the take-profit or stop-loss level is hit.

Plotting and Visuals:

The Heikin-Ashi candles are displayed on the chart, with green candles for uptrends and red candles for downtrends.

Bollinger Bands (upper, lower, and basis) are plotted for visual reference.

Entry points for long and short trades are marked with green and red labels below and above bars, respectively.

Strategy Alerts:

Alerts are triggered when:

A long entry condition is met.

A short entry condition is met.

A trade exits (either via take-profit or stop-loss).

These alerts can be used to trigger notifications or webhook events for automated trading systems.

Notes:

The strategy is designed for use on intraday charts but can be applied to any timeframe.

It is highly customizable, allowing for tailored risk management and trading windows.

The Sunil BB Blast Heikin Ashi Strategy combines two powerful technical analysis tools (Bollinger Bands and Heikin-Ashi candles) with strong risk management, making it suitable for both beginners and experienced traders.

Feebacks are welcome from the users.

BBSS+This Pine Script implements a custom indicator overlaying Bollinger Bands with additional features for trend analysis using Exponential Moving Averages (EMAs). Here's a breakdown of its functionality:

Bollinger Bands:

The script calculates the Bollinger Bands using a 20-period Simple Moving Average (SMA) as the basis and a multiplier of 2 for the standard deviation.

It plots the Upper Band and Lower Band in red.

EMA Calculations:

Three EMAs are calculated for the close price with periods of 5, 10, and 40.

The EMAs are plotted in green (5-period), cyan (10-period), and orange (40-period) to distinguish between them.

Trend Detection:

The script determines bullish or bearish EMA alignments:

Bullish Order: EMA 5 > EMA 10 > EMA 40.

Bearish Order: EMA 5 < EMA 10 < EMA 40.

Entry Signals:

Long Entry: Triggered when:

The close price crosses above the Upper Bollinger Band.

The Upper Band is above its 5-period SMA (indicating momentum).

The EMAs are in a bullish order.

Short Entry: Triggered when:

The close price crosses below the Lower Bollinger Band.

The Lower Band is below its 5-period SMA.

The EMAs are in a bearish order.

Trend State Tracking:

A variable tracks whether the market is in a Long or Short trend based on conditions:

A Long trend continues unless conditions for a Short Entry are met or the Upper Band dips below its average.

A Short trend continues unless conditions for a Long Entry are met or the Lower Band rises above its average.

Visual Aids:

Signal Shapes:

Triangle-up shapes indicate Long Entry points below the bar.

Triangle-down shapes indicate Short Entry points above the bar.

Bar Colors:

Green bars indicate a Long trend.

Red bars indicate a Short trend.

This script combines Bollinger Bands with EMA crossovers to generate entry signals and visualize market trends, making it a versatile tool for identifying momentum and trend reversals.

FT SessionsFT Sessions

Overview

The FT Sessions is a highly customizable and powerful indicator designed for intraday traders who focus on session-based analysis. This script visually highlights global market sessions—Asia, Frankfurt, London, and New York (AM & PM)—on the chart, making it easier to track session ranges and analyze intraday price movements.

Key Features

Customizable Session Times and Colors:

Define your own session times and assign unique colors for better visibility.

Session Range Visualization:

Displays high and low ranges for each session.

Optional transparent range areas with outlines for clarity.

Configurable session range labels for enhanced readability.

Flexible Timezone Settings:

Choose a UTC offset or sync with the exchange's timezone.

User-Friendly Customization:

Compact settings for easier adjustments.

Enable or disable specific sessions to focus on relevant market activity.

How This Script Differs from LuxAlgo

This script draws inspiration from LuxAlgo's session tracking concept but has been developed with significant modifications and unique features:

Built from Scratch in Pine Script v5:

Fully optimized for Pine Script’s latest version, improving performance and functionality.

Expanded Session Range Features:

Five unique sessions (Asia, Frankfurt, London, New York AM, New York PM) with customizable ranges, colors, and labels.

Real-time updating of session ranges for improved intraday analysis.

4H Timeframe Optimization:

Automatically notifies users if applied to an unsupported timeframe, ensuring session accuracy.

Highly Configurable Input Options:

Advanced timezone handling and compact session management settings.

Unique Coding Structure:

Designed to maximize efficiency and minimize resource usage on TradingView.

While LuxAlgo focuses on session concepts, this script brings a fresh, customizable approach specifically tailored for intraday traders seeking precision in tracking session activity.

How It Works

The indicator tracks price movements within each session.

Highlights the high and low range of each session directly on the chart.

Updates session ranges in real-time to reflect evolving market conditions.

Practical Applications

Intraday Trading: Plan trades based on major market session ranges.

Breakout Strategies: Use session high and low levels to identify potential breakouts.

Session-Specific Patterns: Spot consolidations and reversals within session activity.

Important Notes

Optimized for the 4H timeframe. If applied to another timeframe, a notification will appear.

Best used in combination with other tools (e.g., volume or trend indicators) for a complete trading strategy.

Credits

This script draws inspiration from LuxAlgo's open-source session-tracking methodology. However, it introduces substantial improvements and unique features that set it apart. Full credit is given to LuxAlgo for their original open-source concept.

Disclaimer

This script is for informational and educational purposes only. Always test on a demo account before applying to live markets.

TearRepresentative's Rule-Based Dip Buying Strategy Rule-Based Dip Buying Strategy Indicator

This TradingView indicator, inspired by TearRepresentative [ , is a refined tool designed to assist traders in implementing a rule-based dip buying strategy. The indicator automates the identification of optimal buy and sell points, helping traders stay disciplined and minimize emotional biases. It is tailored to index trading, specifically leveraged ETFs like SPXL, to capture opportunities in market pullbacks and recoveries.

Key Features

Dynamic Buy Levels:

Tracks the local high over a customizable lookback period and calculates three buy levels based on percentage drops from the high:

Buy Level 1: First entry point (e.g., 15% drop).

Buy Level 2: Second entry point (e.g., additional 10% drop).

Buy Level 3: Third entry point (e.g., additional 7% drop).

Average Price Tracking:

Dynamically calculates the average price for entered positions when multiple buy levels are triggered.

Sell Level:

Computes a take-profit level (e.g., 20% above the average price) to automate profit-taking when the market rebounds.

Signal Visualization:

Buy Signals: Displayed as green triangles at each buy level.

Sell Signals: Displayed as red triangles at the sell level.

Alerts:

Configurable alerts notify traders when buy or sell signals are triggered, ensuring no opportunity is missed.

Visual Aids:

Semi-transparent and dynamic lines represent buy and sell levels for clear visualization.

Labels provide additional clarity for active levels, helping traders quickly identify actionable signals.

How It Works

The indicator analyzes market movements to identify dips based on predefined thresholds.

Buy signals are triggered when the market price reaches specified levels below the local high.

Once a position is taken, the indicator dynamically adjusts the average entry price and calculates the corresponding sell level.

A sell signal is generated when the market price rises above the calculated take-profit level.

Why Use This Indicator?

Discipline: Automates decision-making, removing emotional factors from trading.

Clarity: Provides clear entry and exit points to simplify complex market dynamics.

Versatility: Suitable for all market conditions, especially during pullbacks and rebounds.

Customization: Allows traders to tailor parameters to their preferred trading style and risk tolerance.

Acknowledgment

This indicator is based on the strategy and insights provided by TearRepresentative, whose expertise in rule-based trading has inspired countless traders. TearRepresentative's approach emphasizes simplicity, reliability, and consistency, offering a robust framework for long-term success.

Quantum ChronoRenko Dynamics Edge - Traditional### **Quantum ChronoRenko Dynamics Edge - Traditional**

**Description:**

The **Quantum ChronoRenko Dynamics Edge - Traditional** is an advanced Renko-based indicator designed for precision trading. It leverages the power of Renko charts to detect price movements, highlight critical trading signals, and dynamically track profit and risk levels. This indicator is built with modern trading strategies in mind, offering robust tools for all traders, from beginners to professionals.

**Key Features:**

1. **Renko-Based Signal Generation**:

- Detects **Buy Signals** when the price closes above the Renko high level.

- Detects **Sell Signals** when the price closes below the Renko low level.

- Ensures signals are non-repainting and confirmed on bar closures.

2. **Take Profit (TP) and Stop Loss (SL) Tracking**:

- Automatically calculates and plots TP and SL levels for every signal.

- Dynamic levels are displayed directly on the chart for better decision-making.

3. **Advanced Signal Management**:

- Prevents duplicate signals within the same Renko range.

- Resets signal conditions when a new Renko range is formed.

4. **Visual Enhancements**:

- Renko high and low levels are plotted with customizable colors and styles.

- TP and SL levels are marked with distinct cross shapes for clarity.

- Optional fill between Renko levels to highlight price ranges.

5. **Real-Time Alerts**:

- Generates alerts for Buy and Sell signals when a candle closes above or below the Renko levels.

- Alerts are designed to help traders react quickly to opportunities.

6. **Comprehensive Statistics**:

- Tracks the number of Buy/Sell signals.

- Calculates the number of TP and SL hits for each signal type.

- Displays detailed percentages and totals in an easy-to-read table.

**Key Benefits**:

- **Non-Repainting Logic**: Ensures stable and reliable signals based on confirmed price movements.

- **Customizability**: Flexible settings for Renko brick size, TP/SL values, and visual enhancements.

- **Professional-Level Insights**: Provides detailed statistics for tracking strategy performance.

**Use Cases**:

- Perfect for intraday and swing traders who rely on Renko charts for clear trend signals.

- Suitable for identifying key breakout opportunities and managing trades with precise TP/SL levels.

Example Usage:

For daily scalping, set the following parameters:

Brick Size: 3

Time Frame: 10 Minutes

This setup provides clean trend signals and dynamic TP/SL tracking for short-term trades.

**Why "Traditional"?**

This version uses the **Traditional Renko method**, ensuring consistent price-based calculations that align with professional trading strategies.

---

**Disclaimer**:

This indicator is a tool to aid trading decisions but does not guarantee profits. Always use proper risk management.

---

Highest High, Lowest Low, Midpoint for Selected Days [kiyarash]Highest High, Lowest Low, and Midpoint for Selected Days Indicator

This custom TradingView indicator allows you to visualize the highest high, lowest low, and the midpoint (average of the highest high and lowest low) over a custom-defined period. You can choose a starting date and specify how many days ahead you want to track the highest and lowest values. This is useful for identifying key levels in a trend and potential support or resistance zones.

How to Use:

Set the Starting Date:

In the settings, input the starting date from which you want to begin tracking the price range. This will be the reference point for your analysis.

Choose the Number of Days to Track:

Specify how many days you want to analyze from the selected starting date. For example, if you want to see the highest high and lowest low over the next 3 days, enter "3" in the settings.

Visualizing the Levels:

The indicator will automatically calculate the highest price and the lowest price over the selected period and draw three lines:

Red Line: Represents the Highest High within the selected period.

Green Line: Represents the Lowest Low within the selected period.

Blue Line: Represents the Midpoint, which is the average of the Highest High and Lowest Low.

Interpretation:

Highest High is a key resistance level, indicating the highest price reached within the specified period.

Lowest Low is a key support level, showing the lowest price during the same period.

Midpoint provides a reference for the average price, often acting as a neutral level between support and resistance.

This tool can help traders to quickly assess potential market ranges, identify breakout or breakdown points, and make informed decisions based on recent price action.

How to Apply:

Add the indicator to your chart.

Adjust the settings to choose your desired starting date and the number of days you want to analyze.

Observe the drawn lines for the Highest High, Lowest Low, and Midpoint levels, and use them to assist in your trading decisions.

Eze Profit - VWAP + MACD Combined SignalThe Eze Profit - VWAP + MACD Combined Signal is an advanced trading tool designed to help traders align price trends with momentum confirmation for better decision-making. By combining Volume-Weighted Average Price (VWAP) and Moving Average Convergence Divergence (MACD), this indicator provides clear entry and exit signals, allowing traders to follow trends and take advantage of momentum shifts.

How It Works:

VWAP:

VWAP represents the average price of an asset, weighted by volume, over a specific period.

It acts as a dynamic support/resistance level and trend filter. Price above VWAP indicates bullish conditions, while price below VWAP suggests bearish conditions.

MACD:

MACD measures momentum through the difference between fast and slow exponential moving averages (EMAs).

Signals are generated when the MACD line crosses its signal line:

Bullish Crossover: Indicates increasing upward momentum.

Bearish Crossunder: Indicates increasing downward momentum.

Combined Logic:

Long Signal: Triggered when price is above VWAP, and MACD exhibits a bullish crossover.

Short Signal: Triggered when price is below VWAP, and MACD exhibits a bearish crossunder.

The script tracks the trader's "in-position" state to prevent redundant signals and ensure clarity.

How to Use:

Use this script to identify potential long and short trading opportunities:

Buy Signal: Enter a long position when the price moves above VWAP and MACD confirms bullish momentum.

Sell Signal: Exit or short when the price drops below VWAP and MACD confirms bearish momentum.

Combine with additional tools like support/resistance, volume analysis, or candlestick patterns for confirmation.

Features:

VWAP Trend Filter: Dynamically adjusts to the trading session to identify overall trend direction.

MACD Momentum Confirmation: Detects key momentum shifts with configurable settings for fast, slow, and signal lengths.

Position State Tracking: Avoids signal redundancy by monitoring open positions.

Buy/Sell Visualizations: Plots Buy/Sell signals directly on the chart for ease of use.

Alerts: Notifies traders in real-time when a long or short signal is triggered.

Customizable Settings:

MACD Fast Length, Slow Length, and Signal Smoothing parameters.

VWAP timeframe resolution to adapt to different trading styles (e.g., intraday or daily).

Credits:

This script is based on standard VWAP and MACD calculations provided by TradingView’s library and has been enhanced with unique logic for combined signal generation.

Notes:

This indicator is intended for educational purposes and should not be considered financial advice. Use it as part of a broader trading strategy alongside other tools for optimal results.

Adaptive ema Cloud v1 Trend & Trade Signals"adaptive ema cloud v1 trend & trade signals" is a comprehensive technical indicator aimed at assisting traders in identifying market trends, trade entry points, and potential take profit (tp) and stop-loss (sl) levels. this indicator combines adaptive exponential moving average (ema) clouds with standard deviation bands to create a visual trend and signal system, enabling users to better analyze price action.

key features:

adaptive ema cloud: calculates a dynamic ema-based cloud using a simple moving average (sma) line, with upper and lower deviation bands based on standard deviations. users can adjust the standard deviation multiplier to modify the cloud's width.

trend direction detection: the indicator determines trend direction by comparing the close price to the ema cloud and signals bullish or bearish trends when the price crosses key levels.

take profit (tp) and stop-loss (sl) points: adaptive tp and sl levels are calculated based on the deviation bands, providing users with suggested exit points when a trade is triggered.

peak and valley detection: detects peaks and valleys in price, aiding traders in spotting potential support and resistance areas.

gradient-based cloud fill: dynamically fills the cloud with a gradient color based on trend strength, helping users visually gauge trend intensity.

trade tracking: tracks recent trades and records them in an internal memory, allowing users to view the last 20 trade outcomes, including whether tp or sl was hit.

how to use:

trend signals: look for green arrows (bullish trend) or red arrows (bearish trend) to identify potential entries based on trend crossovers.

tp/sl management: tp and sl levels are automatically calculated and displayed, with alerts available to notify users when these levels are reached.

adjustable settings: customize period length, standard deviation multiplier, and color preferences to match trading preferences and chart style.

inputs-

period: defines the look-back period for ema calculations.

standard deviation multiplier: adjusts cloud thickness by setting the multiplier for tp and sl bands.

gauge size: scales the gradient intensity for trend cloud visualization.

up/down colors: allows users to set custom colors for bullish and bearish bars.

alert conditions: this script has built-in alerts for trend changes, tp, and sl levels, providing users with automated notifications of important trading signals.

The Pattern-Synced Moving Average System (PSMA)Description:

The Pattern-Synced Moving Average System (PSMA) is a comprehensive trading indicator that combines the reliability of moving averages with automated candlestick pattern detection, real-time alerts, and dynamic risk management to enhance both trend-following and reversal strategies. The PSMA system integrates key elements of trend analysis and pattern recognition to provide users with configurable entry, stop-loss, and take-profit levels. It is designed for all levels of traders who seek to trade in alignment with market context, using signals from trend direction and established candlestick patterns.

Key Functional Components:

Multi-Type Moving Average:

Provides flexibility with multiple moving average options: SMA, EMA, WMA, and SMMA.

The selected moving average helps users determine market trend direction, with price positions relative to the MA acting as a trend confirmation.

Automatic Candlestick Pattern Detection:

Identifies pivotal patterns, including bullish/bearish engulfing and reversal signals.

Helps traders spot potential market turning points and adjust their strategies accordingly.

Configurable Entry, Stop-Loss, and Take-Profit:

Risk management is customizable through risk/reward ratios and risk tolerance settings.

Entry, stop-loss, and take-profit levels are automatically plotted when patterns appear, facilitating rapid trade decision-making with predefined exit points.

Higher Timeframe Trend Confirmation:

Optional feature to verify trend alignment on a higher timeframe (e.g., checking a daily trend on an intraday chart).

This added filter improves signal reliability by focusing on patterns aligned with the broader market trend.

Real-Time Alerts:

Alerts can be set for key pattern detections, allowing traders to respond promptly without constant chart monitoring.

How to Use PSMA:

Set Moving Average Preferences:

Choose the preferred moving average type and length based on your trading strategy. The MA acts as a foundational trend indicator, with price positions indicating potential uptrends (price above MA) or downtrends (price below MA).

Adjust Risk Management Settings:

Set a Risk/Reward Ratio for defining take-profit levels relative to the entry and stop-loss levels.

Modify the Risk Tolerance Percentage to adjust stop-loss placement, adding flexibility in managing trades based on market volatility.

Activate Higher Timeframe Confirmation (Optional):

Enable higher timeframe trend confirmation to filter out counter-trend trades, ensuring that detected patterns are in sync with the larger market trend.

Review Alerts and Trade Levels:

With PSMA’s real-time alerts, traders receive notifications for detected patterns without having to continuously monitor charts.

Visualized entry, stop-loss, and take-profit lines simplify trade execution by highlighting levels directly on the chart.

Execute Based on Entry and Exit Levels:

The entry line suggests the potential entry price once a bullish or bearish pattern is detected.

The stop-loss line is based on your set risk tolerance, establishing a predefined risk level.

The take-profit line is calculated according to your preferred risk/reward ratio, providing a clear profit target.

Example Strategy:

Ensure price is above or below the selected moving average to confirm trend direction.

Await a PSMA signal for a bullish or bearish pattern.

Review the plotted entry, stop-loss, and take-profit lines, and enter the trade if the setup aligns with your risk/reward criteria.

Activate alerts for continuous monitoring, allowing PSMA to notify you of emerging trade opportunities.

Release Notes:

Line Color and Style Customization: Customizable colors and line styles for entry, stop-loss, and take-profit levels.

Dynamic Trade Tracking: Tracks trade statistics, including total trades, win rate, and average P/L, displayed in the data window for comprehensive trade performance analysis.

Summary: The PSMA indicator is a powerful, user-friendly tool that combines trend detection, pattern recognition, and risk management into a cohesive system for improved trade decision-making. Suitable for stocks, forex, and futures, PSMA offers a unique blend of adaptability and precision, making it valuable for day traders and long-term investors alike. Enjoy this tool as it enhances your ability to execute timely, well-informed trades on TradingView.

MultiTimeFrame Trends and Candle Bias (by MC) v1This MultiTimeFrame Trends and Candle Bias provides the trader a quick glance on how each timeframe is trending and what the current candle bias is in each timeframe.

Interpreting Candle Bias : Green points to a bullish bias while red, a bearish bias for a given specific timeframe. For instance, if the current 1 hour candle bias is red, it means that the last hour, the bias has been bearish. If the Daily candle bias is red, it means that the day in question has been a bearish for this selected symbol.

Interpreting MTF Trends: Trends for each time frame follows the simple moving average of the closing prices for the X number of candles you enter in the input section. So for example, if you decide to enter 6 for the 1-hour time frame, the trend for the last 6 hours will be shown and tracked; if on the Daily time frame, you enter 7, the trend for the last 7 days or 1 week will be shown and tracked. I have provided below (as well as on tooltips in the input section of this indicator) recommendations of what numbers to use depending on what kind of trader you are.

What is a best setup for MultiTimeFrame Trends?

Considerations Across All Timeframes:

- Trading Style : Scalpers and very short-term intraday traders may prefer fewer candles (like 12 to 20), which allow them to react quickly to price changes. Swing traders or those holding positions for a few hours to a couple of days might prefer more candles (like 50 to 120) to identify more stable trends.

- Market Conditions : In volatile markets, using more candles helps smooth out price fluctuations and provides a clearer trend signal. In trending markets, fewer candles might be sufficient to capture the trend.

- Session-Based Adjustments : Traders may adjust their settings depending on the time of day or session they are trading. For example, during high-volatility periods like market open or close, using fewer candles can help capture quick moves.

The number of preceding candles to use for estimating the recent trend can depend on various factors, including the type of market, the asset being traded, the timeframe, and the specific goals of your analysis. However, here are some general guidelines to help you decide:

### 1. **Short-Term Trends (Fast Moving Averages):**

- **5 to 20 Candles**: If you want to capture a short-term trend, typically in day trading or scalping strategies, you might use 5 to 20 candles. This is common for fast-moving averages like the 9-period or 15-period moving averages. It reacts quickly to price changes, but it can also give more false signals due to market noise.

### 2. **Medium-Term Trends (Moderate Moving Averages):**

- **20 to 50 Candles**: For a more balanced approach that reduces the impact of short-term volatility while still being responsive to trend changes, 20 to 50 candles are commonly used. This range is popular for swing trading strategies, where the goal is to capture trends that last several days to weeks.

### 3. **Long-Term Trends (Slow Moving Averages):**

- **50 to 200 Candles**: To identify long-term trends, such as those seen in position trading or for confirming major trend directions, you might use 50 to 200 candles. The 50-period and 200-period moving averages are particularly well-known and are often used by traders to identify significant trend reversals or confirmations.

### 4. **Adaptive Approach:**

- **Market Conditions**: In trending markets, fewer candles might be needed to identify a trend, while in choppy or range-bound markets, using more candles can help filter out noise.

- **Volatility**: In highly volatile markets, more candles might be necessary to smooth out price action and avoid false signals.

### **Experiment and Backtesting:**

The optimal number of candles can vary significantly based on the asset and strategy. It's often a good idea to backtest different periods to see which provides the best balance between responsiveness and reliability in identifying trends. You can use tools like the strategy tester in TradingView or other backtesting software to compare the performance of different settings.

### **General Recommendation:**

- **For Shorter Timeframes** (e.g., 5m, 15m): 10-20 candles might be effective.

- **For Medium Timeframes** (e.g., 1h, 4h): 20-50 candles are often a good starting point.

- **For Longer Timeframes** (e.g., Daily, Weekly): 50-200 candles help capture major trends.

If you're unsure, a common starting point for many traders is the 20-period moving average, which provides a balance between sensitivity and reliability.

Guidelines for 1-Minute Timeframe:

For the 1-minute (1M) timeframe, trend analysis typically focuses on very short-term price movements, which is crucial for scalping and ultra-short-term trading strategies. Here’s a breakdown of the number of preceding candles you might use:

1. **Very Short-Term Trend:**

- **10 to 20 Candles (10 to 20 Minutes):** Using 10 to 20 candles captures about 10 to 20 minutes of price action. This range is suitable for scalpers who need to identify very short-term trends and make quick trading decisions.

2. **Short-Term Trend:**

- **30 to 60 Candles (30 to 60 Minutes):** This period covers 30 to 60 minutes of trading, making it useful for traders looking to understand the trend over a full trading hour. It helps capture price movements and trends that develop within a single hour.

3. **Intraday Trend:**

- **120 Candles (2 Hours):** Using 120 candles provides a view of the trend over approximately 2 hours. This is useful for traders who want to see how the market is trending throughout a larger portion of the trading day.

4. **Extended Intraday Trend:**

- **240 to 480 Candles (4 to 8 Hours):** This longer period gives a broader view of the intraday trend, covering 4 to 8 hours. It’s helpful for identifying trends that span a significant portion of the trading day, which can be useful for traders looking to align with the broader intraday movement.

**Considerations:**

- **High Sensitivity:** The 1-minute timeframe is highly sensitive to market movements, so shorter periods (10 to 20 candles) can capture rapid price changes but may also generate noise.

- **Market Volatility:** In highly volatile markets, using more candles (like 30 to 60 or more) helps smooth out the noise and provides a clearer trend signal.

- **Trading Style:** Scalpers will typically use shorter periods to make very quick decisions. Traders holding positions for a bit longer, even within the same day, may use more candles to get a clearer picture of the trend.

**Common Approaches:**

- **5-Period Moving Average:** The 5-period moving average on a 1-minute chart can be used for extremely short-term trend signals, reacting quickly to price changes.

- **20-Period Moving Average:** The 20-period moving average is a good choice for capturing short-term trends and can help filter out some of the noise while still being responsive.

- **50-Period Moving Average:** The 50-period moving average provides a broader view of the trend and can help smooth out price movements over a longer intraday period.

**Recommendation:**

- **Start with 10 to 20 Candles:** For the most immediate and actionable signals, especially useful for scalping or very short-term trading.

- **Use 30 to 60 Candles:** For a clearer view of trends that develop over an hour, suitable for those looking to trade within a single trading hour.

- **Consider 120 Candles:** For observing broader intraday trends over 2 hours, helping align trades with more significant intraday movements.

- **Explore 240 to 480 Candles:** For a longer intraday perspective, covering up to 8 hours, which can be useful for strategies that span a larger portion of the trading day.

**Practical Example:**

- **Scalpers:** If you’re executing trades every few minutes, start with 10 to 20 candles to get rapid trend signals.

- **Short-Term Traders:** For trends that last an hour or so, 30 to 60 candles will provide a better sense of direction while still being responsive.

- **Intraday Traders:** For broader trends that span several hours, 120 candles will help you see the overall intraday movement.

Experimentation and backtesting with these settings on historical data will help you fine-tune your approach to the 1-minute timeframe for your specific trading strategy and asset.

Guidelines for 5, 15 and 30 min Timeframes:

For shorter timeframes like 5, 15, and 30 minutes, the number of preceding candles you use will depend on how quickly you want to react to changes in the trend and the specific trading style you’re employing. Here's a breakdown for each:

**5-Minute Timeframe:**

1. **Very Short-Term (Micro Trend):**

- **12 to 20 Candles (60 to 100 Minutes):** Using 12 to 20 candles on a 5-minute chart captures 1 to 1.5 hours of price action. This is ideal for very short-term trades, such as scalping, where quick entries and exits are key.

2. **Short-Term Trend:**

- **30 to 60 Candles (150 to 300 Minutes):** This period covers 2.5 to 5 hours, making it useful for intraday traders who want to identify the trend within a trading session. It helps capture the direction of the market during the most active parts of the day.

3. **Intra-Day Trend:**

- **120 Candles (10 Hours):** Using 120 candles gives you a broad view of the trend over two trading sessions. This is useful for traders who want to understand the trend throughout the entire trading day.

**15-Minute Timeframe:**

1. **Very Short-Term:**

- **12 to 20 Candles (3 to 5 Hours):** On a 15-minute chart, this period covers 3 to 5 hours, making it useful for capturing the morning or afternoon trend within a trading day. It’s often used by intraday traders who need to make quick decisions.

2. **Short-Term Trend:**

- **30 to 60 Candles (7.5 to 15 Hours):** This covers almost a full trading day to a day and a half. It’s popular among day traders who want to align their trades with the trend of the day or the previous trading session.

3. **Intra-Week Trend:**

- **120 Candles (30 Hours):** This period spans about two trading days and is useful for traders looking to capture trends that may extend beyond a single trading day but not necessarily for an entire week.

**30-Minute Timeframe:**

1. **Short-Term Trend:**

- **12 to 20 Candles (6 to 10 Hours):** This period captures the trend over a single trading session. It's useful for day traders who want to understand the market’s direction throughout the day.

2. **Medium-Term Trend:**

- **30 to 50 Candles (15 to 25 Hours):** This period covers about two trading days and is useful for short-term swing traders or intraday traders who are looking for trends that might last a couple of days.

3. **Intra-Week Trend:**

- **100 to 120 Candles (50 to 60 Hours):** This longer period captures about 4 to 5 trading days, making it useful for traders who want to understand the broader trend over the course of the week.

**Summary Recommendations:**

- **5-Minute Chart:**

- **12 to 20 candles** for very short-term trades.

- **30 to 60 candles** for intraday trends within a single session.

- **120 candles** for a broader view of the day’s trend.

- **15-Minute Chart:**

- **12 to 20 candles** for short-term trades within a few hours.

- **30 to 60 candles** for trends lasting a full day or more.

- **120 candles** for trends extending over a couple of days.

- **30-Minute Chart:**

- **12 to 20 candles** for understanding the daily trend.

- **30 to 50 candles** for trends over a couple of days.

- **100 to 120 candles** for an intra-week trend view.

Experimenting with these settings and backtesting on historical data will help you find the optimal number of candles for your specific trading style and the assets you trade.

Guidelines for 1H Timeframes: