Neural Network Buy and Sell SignalsTrend Architect Suite Lite - Neural Network Buy and Sell Signals

Advanced AI-Powered Signal Scoring

This indicator provides neural network market analysis on buy and sell signals designed for scalpers and day traders who use 30s to 5m charts. Signals are generated based on an ATR system and then filtered and scored using an advanced AI-driven system.

Features

Neural Network Signal Engine

5-Layer Deep Learning analysis combining market structure, momentum, and market state detection

AI-based Letter Grade Scoring (A+ through F) for instant signal quality assessment

Normalized Input Processing with Z-score standardization and outlier clipping

Real-time Signal Evaluation using 5 market dimensions

Advanced Candle Types

Standard Candlesticks - Raw price action

Heikin Ashi - Trend smoothing and noise reduction

Linear Regression - Mathematical trend visualization

Independent Signal vs Display - Calculate signals on one type, display another

Key Settings

Signal Configuration

- Signal Trigger Sensitivity (Default: 1.7) - Controls signal frequency vs quality

- Stop Loss ATR Multiplier (Default: 1.5) - Risk management sizing

- Signal Candle Type (Default: Candlesticks) - Data source for signal calculations

- Display Candle Type (Default: Linear Regression) - Visual candle display

Display Options

- Signal Distance (Default: 1.35 ATR) - Label positioning from price

- Label Size (Default: Medium) - Optimal readability

Trading Applications

Scalping

- Fast pace signal detection with quality filtering

- ATR-based stop management prevents signal overlap

- Neural network attempts to reduces false signals in choppy markets

Day Trading

- Multi-timeframe compatible with adaptation settings

- Clear trend visualization with Linear Regression candles

- Support/resistance integration for better entries/exits

Signal Filtering

- Use A+/A grades for highest probability setups

- B grades for confirmation in trending markets

- C-F grades help identify market uncertainty

Why Choose Trend Architect Lite?

No Lag - Real-time neural network processing

No Repainting - Signals appear and stay fixed

Clean Charts - Focus on price action, not indicators

Smart Filtering - AI reduces noise and false signals

Flexible and customizable - Works across all timeframes and instruments

Compatibility

- All Timeframes - 1m to Monthly charts

- All Instruments - Forex, Crypto, Stocks, Futures, Indices

Risk Disclaimer

This indicator is a tool for technical analysis and should not be used as the sole basis for trading decisions. Past performance does not guarantee future results. Always use proper risk management and never risk more than you can afford to lose.

Penunjuk dan strategi

DrFx Algo MA💎 (V.3.2)🚀 Introducing DrFx Algo MA💎 (V 3.2) – The All-in-One Trading Assistant!

Turn your charts into a powerhouse of precision and clarity.

🔍 What makes DrFx Algo unique?

✅ Smart Candle Coloring – Instantly visualize market sentiment with vibrant, real-time candle colors:

🟢 Green for bullish trends

🔴 Red for bearish movements

💜 Violet & Rose candles highlight EMA proximity for potential trend shifts

📊 Advanced Trend Detection – Dual EMA overlays (20 & 50) clearly define the market's direction. Blue for uptrend, Red for downtrend. Simple, visual, and effective.

📈 Zero Lag EMA (ZLEMA) – Capture fast movements before the crowd. React quicker to market momentum with less delay than traditional EMAs.

🎯 Built-in RSI Alerts – Automatic triangle markers for overbought and oversold levels. Catch early reversal signals without watching RSI manually.

🔔 Smart Alerts System – Get notified instantly with bullish and bearish triggers, right when it matters.

📉 Support & Resistance Auto-Zones – Automatically plots dynamic levels using pivot detection. No more guessing key price zones.

📋 Customizable Trade Dashboard – Input your entries, SL/TP, and trade type. Stay organized with a clean, modern on-screen table. Fully editable.

🧪 Perfect for:

Trend traders

Momentum scalpers

EMA/RSi strategy followers

Visual learners

💼 Whether you’re a day trader or swing trader, DrFx Algo MA💎 gives you the clarity, speed, and edge you need in the market.

💬 Need help with access, backtesting, or have any questions about our indicators?

Our support team is available 24/7 on Telegram.

Just reach out through the link below: 👉https://t.me/Drfxai

“You can reach out by searching this username Drfxai”

Trend Strength Index [Alpha Extract]The Trend Strength Index leverages Volume Weighted Moving Average (VWMA) and Average True Range (ATR) to quantify trend intensity in cryptocurrency markets, particularly Bitcoin. The combination of VWMA and ATR is particularly powerful because VWMA provides a more accurate representation of the market's true average price by weighting periods of higher trading volume more heavily—capturing genuine momentum driven by increased participation rather than treating all price action equally, which is crucial in volatile assets like Bitcoin where volume spikes often signal institutional interest or market shifts.

Meanwhile, ATR normalizes this measurement for volatility, ensuring that trend strength readings remain comparable across different market conditions; without ATR's adjustment, raw price deviations from the mean could appear artificially inflated during high-volatility periods (like during news events or liquidations) or understated in low-volatility sideways markets, leading to misleading signals. Together, they create a volatility-adjusted, volume-sensitive metric that reliably distinguishes between meaningful trend developments and noise.

This indicator measures the normalized distance between price and its volume-weighted mean, providing a clear visualization of trend strength while accounting for market volatility. It helps traders identify periods of strong directional movement versus consolidation, with color-coded gradients for intuitive interpretation.

🔶 CALCULATION

The indicator processes price data through these analytical stages:

Volume Weighted Moving Average: Computes a smoothed average weighted by trading volume

Volatility Normalization: Uses ATR to account for market volatility

Distance Measurement: Calculates absolute deviation between current price and VWMA

Strength Normalization: Divides price deviation by ATR for a volatility-adjusted metric

Formula:

VWMA = Volume-Weighted Moving Average of Close over specified length

ATR = Average True Range over specified length

Price Distance = |Close - VWMA|

Trend Strength = Price Distance / ATR

🔶 DETAILS Visual Features:

VWMA Line: Blue line overlay on the price chart representing the volume-weighted mean

Trend Strength Area: Histogram-style area plot with dynamic color gradient (red for weak trends, transitioning through orange and yellow to green for strong trends)

Threshold Line: Horizontal red line at the customizable Trend Enter level

Background Highlight: Subtle green background when trend strength exceeds the enter threshold for strong trend visualization

Alert System: Triggers notifications for strong trend detection

Interpretation:

0-Weak (Red): Minimal trend strength, potential consolidation or ranging market

Mid-Range (Orange/Yellow): Building momentum, watch for breakout potential

At/Above Enter Threshold (Green): Strong trend conditions, potential for continued directional moves

Threshold Crossing: Trend strength crossing above the enter level signals increasing conviction in the current direction

Color Transitions: Gradual shifts from warm (red/orange) to cool (green) tones indicate strengthening trends

🔶 EXAMPLES

Strong Trend Entry: When trend strength crosses above the enter threshold (e.g., 1.2), it identifies the onset of a powerful move where price deviates significantly from the mean.

Example: During a rally, trend strength rising from yellow (around 1.0) to green (1.2+) often precedes sustained upward momentum, providing entry opportunities for trend followers.

Consolidation Detection: Low trend strength values in red shades (below 0.5) highlight periods of low volatility and mean reversion potential.

Example: After a sharp sell-off, persistent red values signal a likely sideways phase, allowing traders to avoid whipsaws and wait for orange/yellow transitions as a precursor to recovery.

Volatility-Adjusted Pullbacks: In volatile markets, the ATR component ensures trend strength remains accurate; a dip back to yellow from green during minor corrections can indicate healthy pullbacks within a strong trend.

Example: Trend strength briefly falling to yellow levels (e.g., 0.8-1.1) after hitting green provides profit-taking signals without invalidating the overall bullish bias if the VWMA holds as support.

Threshold Alert Integration: The alert condition combines strength value with the enter threshold for timely notifications.

Example: Receiving a "Strong Trend Detected" alert when the area plot turns green helps confirm Bitcoin's breakout from consolidation, aligning with increased volume for higher-probability trades.

🔶 SETTINGS

Customization Options:

Lengths: VWMA length (default 14), ATR length (default 14)

Thresholds: Trend enter (default 1.2, step 0.1), trend exit (default 1.15, for potential future signal enhancements)

Visuals: Automatic color scaling with red at 0, transitioning to green at/above enter threshold

Alert Conditions: Strong trend detection (when strength > enter)

The Trend Strength Index equips traders with a robust, easy-to-interpret tool for gauging trend intensity in volatile markets like Bitcoin. By normalizing price deviations against volatility, it delivers reliable signals for identifying high-momentum opportunities while the gradient coloring and alerts facilitate quick assessments in both trending and choppy conditions.

Cryptokazancev Strategy PackCryptokazancev Strategy Pack

Комплексный инструмент для анализа рыночной структуры / Comprehensive Market Structure Analysis Tool

🇷🇺 Описание на русском

Cryptokazancev Strategy Pack by ZeeZeeMon - это мощный набор инструментов для технического анализа, включающий:

• Ордерблоки (Order Blocks) с настройкой количества и цветов

• Пивоты (Pivot Points) различных таймфреймов

• Рыночную структуру с зонами Фибоначчи (0.618, 0.786)

• Разворотные конструкции (пинбары и поглощения)

• Зоны интереса на основе скопления свингов

📊 Основные функции:

1. Ордерблоки

- Автоматическое определение бычьих/медвежьих OB

- Настройка максимального количества блоков (до 30)

- Кастомизация цветов

2. Пивоты

- Поддержка таймфреймов: Дневные/Недельные/Месячные/Квартальные/Годовые

- Уровни Camarilla (P, R1-R4, S1-S4)

3. Рыночная структура

- Четкое определение тренда (UP/DOWN)

- Ключевые уровни Фибо (0.618 и 0.786)

- Настройка глубины анализа (10-1000 баров)

4. Разворотные конструкции

- Обнаружение пинбаров

- Обнаружение поглощений

- Настройка чувствительности

5. Зоны интереса

- Алгоритм кластеризации свингов

- Настройка через ATR-мультипликатор

- Лимит отображаемых зон

🇬🇧 English Description

ZeeZeeMon Pack is a comprehensive market analysis toolkit featuring:

• Order Blocks with customizable count and colors

• Pivot Points for multiple timeframes

• Market Structure with Fibonacci zones

• Reversal patterns (pinbars and engulfings)

• Interest Zones based on swing clustering

📊 Key Features:

1. Order Blocks

- Auto-detection of bullish/bearish OB

- Configurable max blocks (up to 30)

- Custom color schemes

2. Pivot Points

- Supports: Daily/Weekly/Monthly/Quarterly/Yearly

- Camarilla levels (P, R1-R4, S1-S4)

3. Market Structure

- Clear trend detection (UP/DOWN)

- Key Fibonacci levels (0.618 & 0.786)

- Adjustable analysis depth (10-1000 bars)

4. Reversal Patterns

- Smart pinbar detection

- ATR-based engulfing filter

- Sensitivity adjustment

5. Interest Zones

- Swing clustering algorithm

- ATR-multiplier configuration

- Display limit (up to 10 zones)

⚙️ Technical Highlights:

• Built with Pine Script v5

• Performance-optimized

• Well-commented code

• Flexible settings system

⚠️ Важно / Important:

Индикатор в бета-версии. Тестируйте перед использованием в реальной торговле.

This is BETA version. Please test before live trading.

💬 Поддержка / Support:

Комментарии к скрипту / Script comments section

ZZUltraOverview:

ZZUltra is a powerful price action filter designed to identify significant swing highs and lows by eliminating market noise. Unlike the default, this version offers enhanced customization and dynamic behavior, making it ideal for trend analysis, pattern recognition, and timing entries/exits. Note that it is a lagging indicator and for the optimized live version go to Ultraalgo.com

Key Features:

📏 Adjustable Depth, Deviation & Backstep: Fine-tune how sensitive the indicator is to price reversals.

🔍 Dynamic Labeling: Mark each swing with customizable labels (e.g., UltraBuy/UltraShort).

🎨 Clean Visuals: Optional colored lines and markers that clearly connect turning points without overwhelming your chart.

🧠 Built-in Smart Filtering: Filters out minor fluctuations to focus on meaningful market structure.

🧰 Multi-Timeframe Compatible: Works across any timeframe for both scalpers and swing traders.

Use Cases:

Confirming trend structure (e.g., higher highs/lows in uptrends).

Identifying key reversal points.

Recognizing patterns like head & shoulders or double tops.

Combining with RSI, MACD, or volume for confluence.

Advanced Forex Currency Strength Meter

# Advanced Forex Currency Strength Meter

🚀 The Ultimate Currency Strength Analysis Tool for Forex Traders

This sophisticated indicator measures and compares the relative strength of major currencies (EUR, GBP, USD, JPY, CHF, CAD, AUD, NZD) to help you identify the strongest and weakest currencies in real-time, providing clear trading signals based on currency strength differentials.

## 📊 What This Indicator Does

The Advanced Forex Currency Strength Meter analyzes currency relationships across 28+ major forex pairs and 8 currency indices to determine which currencies are gaining or losing strength. Instead of relying on individual pair analysis, this tool gives you a bird's-eye view of the entire forex market, helping you:

Identify the strongest and weakest currencies at any given time

Find high-probability trading opportunities by pairing strong vs weak currencies

Avoid ranging markets by detecting when currencies have similar strength

Get clear LONG/SHORT/NEUTRAL signals for your current trading pair

Optimize your trading strategy based on your preferred timeframe and holding period

## ⚙️ How The Indicator Works

### Dual Calculation Method

The indicator uses a sophisticated dual approach for maximum accuracy:

Pairs-Based Analysis: Calculates currency strength from 28+ major forex pairs (EURUSD, GBPUSD, USDJPY, etc.)

Index-Based Analysis: Incorporates official currency indices (DXY, EXY, BXY, JXY, CXY, AXY, SXY, ZXY)

Weighted Combination: Blends both methods using smart weighting for enhanced accuracy

### Smart Auto-Optimization System

The indicator automatically adjusts its parameters based on your chart timeframe and intended holding period:

The system recognizes that scalping requires different sensitivity than swing trading, automatically optimizing lookback periods, analysis timeframes, signal thresholds, and index weights.

### Strength Calculation Process

Fetches price data from multiple timeframes using optimized tuple requests

Calculates percentage change over the specified lookback period

Optionally normalizes by ATR (Average True Range) to account for volatility differences

Combines pair-based and index-based calculations using dynamic weighting

Generates relative strength by comparing base currency vs quote currency

Produces clear trading signals when strength differential exceeds threshold

## 🎯 How To Use The Indicator

### Quick Start

Add the indicator to any forex pair chart

Enable 🧠 Smart Auto-Optimization (recommended for beginners)

Watch for LONG 🚀 signals when the relative strength line is green and above threshold

Watch for SHORT 🐻 signals when the relative strength line is red and below threshold

Avoid trading during NEUTRAL ⚪ periods when currencies have similar strength

Note: This is highly recommended to couple this indicator with fundamental analysis and use it as an extra signal.

### 📋 Parameters Reference

#### 🤖 Smart Settings

🧠 Smart Auto-Optimization: (Default: Enabled) Automatically optimizes all parameters based on chart timeframe and trading style

#### ⚙️ Manual Override

These settings are only active when Smart Auto-Optimization is disabled:

Manual Lookback Period: (Default: 14) Number of periods to analyze for strength calculation

Manual ATR Period: (Default: 14) Period for ATR normalization calculation

Manual Analysis Timeframe: (Default: 240) Higher timeframe for strength analysis

Manual Index Weight: (Default: 0.5) Weight given to currency indices vs pairs (0.0 = pairs only, 1.0 = indices only)

Manual Signal Threshold: (Default: 0.5) Minimum strength differential required for trading signals

#### 📊 Display

Show Signal Markers: (Default: Enabled) Display triangle markers when signals change

Show Info Label: (Default: Enabled) Show comprehensive information label with current analysis

#### 🔍 Analysis

Use ATR Normalization: (Default: Enabled) Normalize strength calculations by volatility for fairer comparison

#### 💰 Currency Indices

💰 Use Currency Indices: (Default: Enabled) Include all 8 currency indices in strength calculation for enhanced accuracy

#### 🎨 Colors

Strong Currency Color: (Default: Green) Color for positive/strong signals

Weak Currency Color: (Default: Red) Color for negative/weak signals

Neutral Color: (Default: Gray) Color for neutral conditions

Strong/Weak Backgrounds: Background colors for clear signal visualization

### 🧠 Smart Optimization Profiles

The indicator automatically selects optimal parameters based on your chart timeframe:

#### ⚡ Scalping Profile (1M-5M Charts)

For positions held for a few minutes:

Lookback: 5 periods (fast/sensitive)

Analysis Timeframe: 15 minutes

Index Weight: 20% (favor pairs for speed)

Signal Threshold: 0.3% (sensitive triggers)

#### 📈 Intraday Profile (10M-1H Charts)

For positions held for a few hours:

Lookback: 12 periods (balanced sensitivity)

Analysis Timeframe: 4 hours

Index Weight: 40% (balanced approach)

Signal Threshold: 0.4% (moderate sensitivity)

#### 📊 Swing Profile (4H-Daily Charts)

For positions held for a few days:

Lookback: 21 periods (stable analysis)

Analysis Timeframe: Daily

Index Weight: 60% (favor indices for stability)

Signal Threshold: 0.5% (conservative triggers)

#### 📆 Position Profile (Weekly+ Charts)

For positions held for a few weeks:

Lookback: 30 periods (long-term view)

Analysis Timeframe: Weekly

Index Weight: 70% (heavily favor indices)

Signal Threshold: 0.6% (very conservative)

### Entry Timing

Wait for clear LONG 🚀 or SHORT 🐻 signals

Avoid trading during NEUTRAL ⚪ periods

Look for signal confirmations on multiple timeframes

### Risk Management

Stronger signals (higher relative strength values) suggest higher probability trades

Use appropriate position sizing based on signal strength

Consider the trading style profile when setting stop losses and take profits

💡 Pro Tip: The indicator works best when combined with your existing technical analysis. Use currency strength to identify which pairs to trade, then use your favorite technical indicators to determine when to enter and exit.

## 🔧 Key Features

28+ Forex Pairs Analysis: Comprehensive coverage of major currency relationships

8 Currency Indices Integration: DXY, EXY, BXY, JXY, CXY, AXY, SXY, ZXY for enhanced accuracy

Smart Auto-Optimization: Automatically adapts to your trading style and timeframe

ATR Normalization: Fair comparison across different currency pairs and volatility levels

Real-Time Signals: Clear LONG/SHORT/NEUTRAL signals with visual markers

Performance Optimized: Efficient tuple-based data requests minimize external calls

User-Friendly Interface: Simplified settings with comprehensive tooltips

Multi-Timeframe Support: Works on any timeframe from 1-minute to monthly charts

Transform your forex trading with the power of currency strength analysis! 🚀

J值极值趋势跟随策略J-Zone & 检测3分钟周期信号

EMA 676均线上方只做多

EMA 676均线下方只做空

当J线达到极值100后,并且连续3根K线J OKX:ETHUSDT.P OKX:ETHUSDT.P 值连续上涨开始回落,开空单

当J线达到极值0后,并且连续3根K线J值连续下跌开始上涨,开多单

1. Only consider long positions when the price is above the EMA676.

2. Only consider short positions when the price is below the EMA676.

3. If the J value reaches the extreme of 100, and there are 3 consecutive candles where the J value increases, then the first downturn in J triggers a short entry.

4. If the J value reaches the extreme of 0, and there are 3 consecutive candles where the J value decreases, then the first upturn in J triggers a long entry.

RSI-Stochastic Combined Oscillator(Mastersinnifty)Description

The RSI-Stochastic Combined Oscillator blends the strengths of RSI and Stochastic indicators to offer a refined view of market momentum. This custom oscillator highlights high-probability turning points using both value crossovers and directional momentum filters. Enhanced signal logic distinguishes between strong and weak trade setups.

How It Works

Calculates RSI and Stochastic %K using user-defined lengths.

Generates a combined oscillator by averaging RSI and Stochastic %K.

Smoothes the output with configurable MA for clarity.

Generates bullish/bearish signals based on crossover logic and momentum strength.

Includes overbought/oversold zones and background color warnings.

Optional signal table displays real-time values for RSI, Stochastic, Combo, and Signal Line.

Inputs

RSI Length – Period for RSI calculation.

Stochastic %K/%D Length – Periods for Stochastic values.

Combined Oscillator Smoothing – Moving average smoothing period.

Overbought/Oversold Levels – Thresholds for signal filtering and background alerts.

Use Case

Ideal for traders looking to:

Confirm entries using dual momentum logic.

Filter out noise with smoothed oscillators.

Identify high-conviction reversal zones.

Receive alerts based on strong and weak momentum shifts.

Disclaimer

This indicator is designed for educational purposes only and does not constitute financial advice. Always conduct your own analysis before making trading decisions.

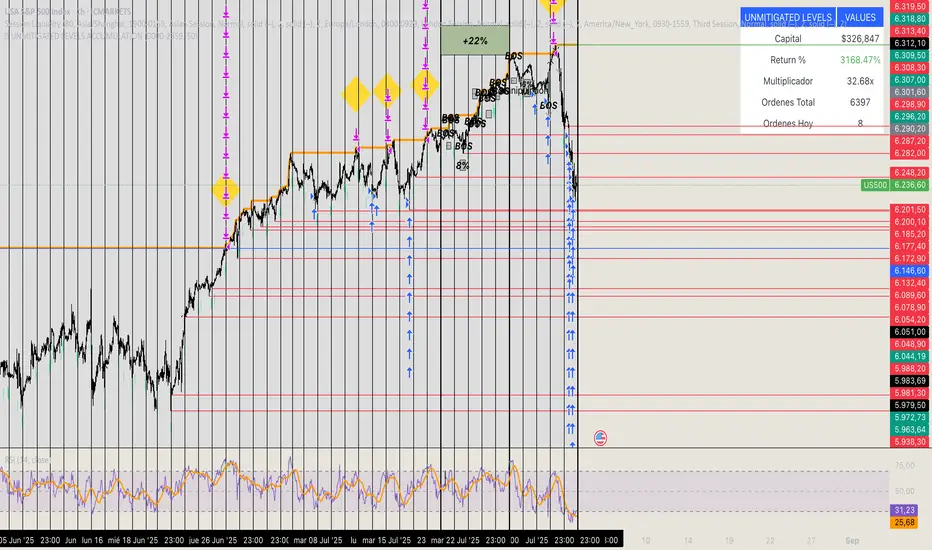

🏆 UNMITIGATED LEVELS ACCUMULATIONPDH TO ATH RISK FREE

All the PDL have a buy limit which starts at 0.1 lots which will duplicate at the same time the capital incresases. All of the buy limits have TP in ATH for max reward.

AshishBediSPLAshishBediSPL: Dynamic Premium Analysis with Integrated Signals

This indicator provides a comprehensive view of combined options premiums by aggregating data from Call and Put contracts for a selected index and expiry. It integrates multiple popular technical indicators like EMA Crossover, Supertrend, VWAP, RSI, and SMA, allowing users to select their preferred tools for generating dynamic buy and sell signals directly on the premium chart.

AshishBediSPL" is a powerful TradingView indicator designed to analyze options premiums. It calculates a real-time combined premium for a chosen index (NIFTY, BANKNIFTY, FINNIFTY, etc.) and specific expiry date. You have the flexibility to visualize the premium of Call options, Put options, or a combined premium of both.

The indicator then overlays several popular technical analysis tools, which you can selectively enable:

EMA Crossover: Identify trend changes with configurable fast and slow Exponential Moving Averages.

Supertrend: Detect trend direction and potential reversal points.

VWAP (Volume Weighted Average Price): Understand the average price of the premium considering trading volume.

RSI (Relative Strength Index): Gauge momentum and identify overbought/oversold conditions.

SMA (Simple Moving Average): Analyze price smoothing and trend identification.

Based on your selected indicators, the tool generates clear "Buy" and "Sell" signals directly on the chart, helping you identify potential entry and exit points. Customizable alerts are also available to keep you informed.

Unlock a new perspective on options trading with "AshishBediSPL." This indicator focuses on the combined value of options premiums, giving you a consolidated view of market sentiment for a chosen index and expiry.

Instead of just looking at individual option prices, "AshishBediSPL" blends the Call and Put premiums (or focuses on one, based on your preference) and empowers you with a suite of built-in technical indicators: EMA, Supertrend, VWAP, RSI, and SMA. Pick the indicators that resonate with your strategy, and let the tool generate actionable buy and sell signals right on your chart. With customizable alerts, you'll never miss a crucial market move. Gain deeper insights and make more informed trading decisions with "AshishBediSPL.

Combined options premium: This accurately describes what your indicator calculates.

Selected index and expiry: Essential inputs for the indicator.

Call/Put options or combined: Explains the flexibility in data display.

Multiple technical indicators (EMA Crossover, Supertrend, VWAP, RSI, SMA): Lists the analysis tools included.

Buy/Sell signals: The primary output of the indicator.

Customizable alerts: A valuable feature for users.

NAS100 and gold Smart Scalping Strategy PRO [Enhanced v2]It works on both Gold, Platinum and USTEC100. Profit factor between 6-9. Great Profit making with risk management

Ultimate Scalping Strategy v2Strategy Overview

This is a versatile scalping strategy designed primarily for low timeframes (like 1-min, 3-min, or 5-min charts). Its core logic is based on a classic EMA (Exponential Moving Average) crossover system, which is then filtered by the VWAP (Volume-Weighted Average Price) to confirm the trade's direction in alignment with the market's current intraday sentiment.

The strategy is highly customizable, allowing traders to add layers of confirmation, control trade direction, and manage exits with precision.

Core Strategy Logic

The strategy's entry signals are generated when two primary conditions are met simultaneously:

Momentum Shift (EMA Crossover): It looks for a crossover between a fast EMA (default length 9) and a slow EMA (default length 21).

Buy Signal: The fast EMA crosses above the slow EMA, indicating a potential shift to bullish momentum.

Sell Signal: The fast EMA crosses below the slow EMA, indicating a potential shift to bearish momentum.

Trend/Sentiment Filter (VWAP): The crossover signal is only considered valid if the price is on the "correct" side of the VWAP.

For a Buy Signal: The price must be trading above the VWAP. This confirms that, on average, buyers are in control for the day.

For a Sell Signal: The price must be trading below the VWAP. This confirms that sellers are generally in control.

Confirmation Filters (Optional)

To increase the reliability of the signals and reduce false entries, the strategy includes two optional confirmation filters:

Price Action Filter (Engulfing Candle): If enabled (Use Price Action), the entry signal is only valid if the crossover candle is also an "engulfing" candle.

A Bullish Engulfing candle is a large green candle that completely "engulfs" the body of the previous smaller red candle, signaling strong buying pressure.

A Bearish Engulfing candle is a large red candle that engulfs the previous smaller green candle, signaling strong selling pressure.

Volume Filter (Volume Spike): If enabled (Use Volume Confirmation), the entry signal must be accompanied by a surge in volume. This is confirmed if the volume of the entry candle is greater than its recent moving average (default 20 periods). This ensures the move has strong participation behind it.

Exit Strategy

A position can be closed in one of three ways, creating a comprehensive exit plan:

Stop Loss (SL): A fixed stop loss is set at a level determined by a multiple of the Average True Range (ATR). For example, a 1.5 multiplier places the stop 1.5 times the current ATR value away from the entry price. This makes the stop dynamic, adapting to market volatility.

Take Profit (TP): A fixed take profit is also set using an ATR multiplier. By setting the TP multiplier higher than the SL multiplier (e.g., 2.0 for TP vs. 1.5 for SL), the strategy aims for a positive risk-to-reward ratio on each trade.

Exit on Opposite Signal (Reversal): If enabled, an open position will be closed automatically if a valid entry signal in the opposite direction appears. For example, if you are in a long trade and a valid short signal occurs, the strategy will exit the long position immediately. This feature turns the strategy into more of a reversal system.

Key Features & Customization

Trade Direction Control: You can enable or disable long and short trades independently using the Allow Longs and Allow Shorts toggles. This is useful for trading in harmony with a higher-timeframe trend (e.g., only allowing longs in a bull market).

Visual Plots: The strategy plots the Fast EMA, Slow EMA, and VWAP on the chart for easy visualization of the setup. It also plots up/down arrows to mark where valid buy and sell signals occurred.

Dynamic SL/TP Line Plotting: A standout feature is that the strategy automatically draws the exact Stop Loss and Take Profit price lines on the chart for every active trade. These lines appear when a trade is entered and disappear as soon as it is closed, providing a clear visual of your risk and reward targets.

Alerts: The script includes built-in alertcondition calls. This allows you to create alerts in TradingView that can notify you on your phone or execute trades automatically via a webhook when a long or short signal is generated.

Ichimoku Trend CycleIchimoku Trend Cycle

A precision dual-trend system combining Ichimoku-based ATR Supertrends — engineered for clarity, reliability, and smart trend detection.

🔷 What is Ichimoku Trend Cycle?

The Ichimoku Trend Cycle harnesses the power of traditional Ichimoku analysis with modern ATR-based supertrend technology:

Alpha Trend: Primary trend detection using Ichimoku conversion & baseline logic

Beta Trend: Secondary confirmation trend with independent ATR calculations

Dual Confirmation Engine : Both trends must align for signal generation

This powerful combination delivers clean, non-repainting Buy/Sell signals while filtering out market noise and false breakouts.

🔍 How It Works

Blue Alpha + Red Beta Trends Align Bullish → BUY Signal

Both Trends Turn Bearish → SELL Signal

You get ONE signal per trend change — no spam, no noise, just crystal-clear direction changes.

⚙️ Core Features

✅ Ichimoku-Enhanced Supertrends

Traditional Ichimoku conversion/baseline logic powering modern ATR bands.

✅ Dual-Trend Confirmation

Alpha and Beta trends must agree — eliminates false signals.

✅ One Alert Per Trend Shift

Clean entries, zero noise, no repeated signals.

✅ Visual Excellence

Color-coded trend lines with high-contrast BUY/SELL labels.

✅ Fully Customizable

Independent settings for both trend systems plus smoothing options.

🎯 Perfect For

Swing Traders wanting confirmed trend changes

Position Traders seeking major trend shifts

Anyone who values clean charts with sharp decision points

🛠 Settings Breakdown

Alpha Trend Settings: Primary trend with conversion/baseline periods + ATR multiplier

Beta Trend Settings: Secondary confirmation trend with independent parameters

Smoothing MA Settings: Optional MA smoothing with Bollinger Bands support

Alert Settings: Customize signal confirmation periods

Candle Color Settings: Fully customizable trend and candle color schemes

✅ Built-in Smart Alerts — Never miss a trend change again

⚡ Zero-lag Performance — Works flawlessly across all timeframes

📈 Strategy-Ready Code — Professional-grade, non-repainting signals

Transform your trading with the precision of Ichimoku and the reliability of dual-trend confirmation.

swing_funThis is a very simple swing trading entry point indicator, design to be used on the indexes with the 4hr chart. It gives alerts whenever a long or short signal is found.

BERLIN-MAX 1V.5BERLIN-MAX 1V.5 is a comprehensive trading indicator designed for TradingView that combines multiple advanced strategies and tools. It integrates EMA crossover signals, UT Bot logic with ATR-based trailing stops, customizable stop-loss and target multipliers per timeframe, Hull Moving Averages with color-coded trends, linear regression channels for support and resistance, and a multi-timeframe RSI and volume signal table. This script aims to provide clear entry and exit signals for scalping and swing trading, enhancing decision-making across different market conditions.

ZZUltraAlgo Basic EditionBasic set-up non optimized ZZ indicator. Use ultraalgo.com for the optimized / live (no lag, great for active live trading vs. look-back analysis) version

Overview:

ZZ is a powerful lagging price action filter designed to identify significant swing highs and lows by eliminating market noise. Unlike the default, this version offers enhanced customization and dynamic behavior, making it ideal for trend analysis, pattern recognition, and timing entries/exits.

Key Features:

📏 Adjustable Depth, Deviation & Backstep: Fine-tune how sensitive the indicator is to price reversals.

🔍 Dynamic Labeling: Mark each swing with customizable labels (e.g., HH, HL, LH, LL or custom terms like UltraBuy/UltraShort).

🎨 Clean Visuals: Optional colored lines and markers that clearly connect turning points without overwhelming your chart.

🧠 Built-in Smart Filtering: Filters out minor fluctuations to focus on meaningful market structure.

🧰 Multi-Timeframe Compatible: Works across any timeframe for both scalpers and swing traders.

Use Cases:

Confirming trend structure (e.g., higher highs/lows in uptrends).

Identifying key reversal points.

Recognizing patterns like head & shoulders or double tops.

Combining with RSI, MACD, or volume for confluence.

XAUUSD Smart Money Sweep StrategyThis is a custom-built Smart Money Concept (SMC) strategy for XAUUSD that detects liquidity sweeps at key swing levels and confirms entries using momentum-based reversal candles. It simulates institutional behavior by entering trades only when price grabs liquidity (stop hunts above highs or below lows), then shows strong rejection in the opposite direction.

The strategy uses precise entry logic, fixed stop loss, and a customizable risk-to-reward ratio for dynamic take-profit targeting. All trades are fully backtestable using TradingView’s built-in strategy() functions.

This approach is ideal for Smart Money traders looking to exploit price inefficiencies without relying on BOS or FVG logic.

🔑 Key Features:

Liquidity Sweep Logic: Detects price sweeping above recent highs or below recent lows, simulating stop hunts and liquidity grabs.

Candle Confirmation Filter: Confirms entry only if a strong reversal candle (momentum shift) forms after the sweep, avoiding weak entries.

Full Backtest Engine: Uses TradingView's strategy.entry() and strategy.exit() to simulate trades with real SL/TP tracking.

Custom Risk Management: Adjustable stop loss (in pips) and risk-to-reward (RR) ratio allow you to shape trade outcomes and optimize strategy performance.

Non-Repainting Logic: All entries are based on closed candles, meaning the signals never repaint and are reliable for testing and execution.

⚙️ Settings:

Setting Description

Liquidity Lookback Number of candles to look back for swing highs/lows to determine sweeps

Stop Loss (pips) Distance below/above entry where SL is placed (fixed pip SL)

Risk/Reward Ratio Multiplies SL to calculate TP (e.g., 1:2 = 2x SL as TP)

Entry Logic Requires sweep + a momentum candle (e.g., bullish close after a sweep down)

📊 How It Works:

The strategy scans recent price action using a lookback range to find the highest high and lowest low (liquidity zones).

If price sweeps above the high or below the low, this triggers a potential entry condition.

A momentum candle confirmation must follow immediately:

For long trades: bullish candle (close > open, and close > previous close)

For short trades: bearish candle (close < open, and close < previous close)

If confirmed, the strategy:

Enters the trade

Places a fixed stop loss in pips

Sets a dynamic TP using the RR ratio

All trades are logged and visualized in the Strategy Tester panel for performance review.

📌 Optimized For:

XAUUSD (Gold) on 15m, 30m, and 1H timeframes

Smart Money / ICT / Liquidity-based trading styles

Traders who prefer reversal setups after liquidity raids

Systems focused on precise execution and high-RR setups

📎 Release Notes:

v1.0 – First release featuring liquidity sweep detection, candle confirmation logic, SL/TP execution, and Strategy Tester support. Clean structure designed for real-world backtesting on volatile instruments like gold.

⚠️ Disclaimer:

This script is for educational and research purposes only. It does not constitute financial advice or signal services. Always validate strategy results with manual backtesting and apply proper risk management.

NY Premarket – High/LowNY Premarket – High/Low

Displays two horizontal lines for the last completed New York pre‑market session (07:00–09:30 America/New_York):

Premarket High (top wick of the session)

Premarket Low (bottom wick of the session)

Both lines are anchored to the exact candles that formed the session’s high/low and remain aligned with those candles regardless of zooming or panning.ng or panning.

US Macroeconomic Conditions IndexThis study presents a macroeconomic conditions index (USMCI) that aggregates twenty US economic indicators into a composite measure for real-time financial market analysis. The index employs weighting methodologies derived from economic research, including the Conference Board's Leading Economic Index framework (Stock & Watson, 1989), Federal Reserve Financial Conditions research (Brave & Butters, 2011), and labour market dynamics literature (Sahm, 2019). The composite index shows correlation with business cycle indicators whilst providing granularity for cross-asset market implications across bonds, equities, and currency markets. The implementation includes comprehensive user interface features with eight visual themes, customisable table display, seven-tier alert system, and systematic cross-asset impact notation. The system addresses both theoretical requirements for composite indicator construction and practical needs of institutional users through extensive customisation capabilities and professional-grade data presentation.

Introduction and Motivation

Macroeconomic analysis in financial markets has traditionally relied on disparate indicators that require interpretation and synthesis by market participants. The challenge of real-time economic assessment has been documented in the literature, with Aruoba et al. (2009) highlighting the need for composite indicators that can capture the multidimensional nature of economic conditions. Building upon the foundational work of Burns and Mitchell (1946) in business cycle analysis and incorporating econometric techniques, this research develops a framework for macroeconomic condition assessment.

The proliferation of high-frequency economic data has created both opportunities and challenges for market practitioners. Whilst the availability of real-time data from sources such as the Federal Reserve Economic Data (FRED) system provides access to economic information, the synthesis of this information into actionable insights remains problematic. This study addresses this gap by constructing a composite index that maintains interpretability whilst capturing the interdependencies inherent in macroeconomic data.

Theoretical Framework and Methodology

Composite Index Construction

The USMCI follows methodologies for composite indicator construction as outlined by the Organisation for Economic Co-operation and Development (OECD, 2008). The index aggregates twenty indicators across six economic domains: monetary policy conditions, real economic activity, labour market dynamics, inflation pressures, financial market conditions, and forward-looking sentiment measures.

The mathematical formulation of the composite index follows:

USMCI_t = Σ(i=1 to n) w_i × normalize(X_i,t)

Where w_i represents the weight for indicator i, X_i,t is the raw value of indicator i at time t, and normalize() represents the standardisation function that transforms all indicators to a common 0-100 scale following the methodology of Doz et al. (2011).

Weighting Methodology

The weighting scheme incorporates findings from economic research:

Manufacturing Activity (28% weight): The Institute for Supply Management Manufacturing Purchasing Managers' Index receives this weighting, consistent with its role as a leading indicator in the Conference Board's methodology. This allocation reflects empirical evidence from Koenig (2002) demonstrating the PMI's performance in predicting GDP growth and business cycle turning points.

Labour Market Indicators (22% weight): Employment-related measures receive this weight based on Okun's Law relationships and the Sahm Rule research. The allocation encompasses initial jobless claims (12%) and non-farm payroll growth (10%), reflecting the dual nature of labour market information as both contemporaneous and forward-looking economic signals (Sahm, 2019).

Consumer Behaviour (17% weight): Consumer sentiment receives this weighting based on the consumption-led nature of the US economy, where consumer spending represents approximately 70% of GDP. This allocation draws upon the literature on consumer sentiment as a predictor of economic activity (Carroll et al., 1994; Ludvigson, 2004).

Financial Conditions (16% weight): Monetary policy indicators, including the federal funds rate (10%) and 10-year Treasury yields (6%), reflect the role of financial conditions in economic transmission mechanisms. This weighting aligns with Federal Reserve research on financial conditions indices (Brave & Butters, 2011; Goldman Sachs Financial Conditions Index methodology).

Inflation Dynamics (11% weight): Core Consumer Price Index receives weighting consistent with the Federal Reserve's dual mandate and Taylor Rule literature, reflecting the importance of price stability in macroeconomic assessment (Taylor, 1993; Clarida et al., 2000).

Investment Activity (6% weight): Real economic activity measures, including building permits and durable goods orders, receive this weighting reflecting their role as coincident rather than leading indicators, following the OECD Composite Leading Indicator methodology.

Data Normalisation and Scaling

Individual indicators undergo transformation to a common 0-100 scale using percentile-based normalisation over rolling 252-period (approximately one-year) windows. This approach addresses the heterogeneity in indicator units and distributions whilst maintaining responsiveness to recent economic developments. The normalisation methodology follows:

Normalized_i,t = (R_i,t / 252) × 100

Where R_i,t represents the percentile rank of indicator i at time t within its trailing 252-period distribution.

Implementation and Technical Architecture

The indicator utilises Pine Script version 6 for implementation on the TradingView platform, incorporating real-time data feeds from Federal Reserve Economic Data (FRED), Bureau of Labour Statistics, and Institute for Supply Management sources. The architecture employs request.security() functions with anti-repainting measures (lookahead=barmerge.lookahead_off) to ensure temporal consistency in signal generation.

User Interface Design and Customization Framework

The interface design follows established principles of financial dashboard construction as outlined in Few (2006) and incorporates cognitive load theory from Sweller (1988) to optimise information processing. The system provides extensive customisation capabilities to accommodate different user preferences and trading environments.

Visual Theme System

The indicator implements eight distinct colour themes based on colour psychology research in financial applications (Dzeng & Lin, 2004). Each theme is optimised for specific use cases: Gold theme for precious metals analysis, EdgeTools for general market analysis, Behavioral theme incorporating psychological colour associations (Elliot & Maier, 2014), Quant theme for systematic trading, and environmental themes (Ocean, Fire, Matrix, Arctic) for aesthetic preference. The system automatically adjusts colour palettes for dark and light modes, following accessibility guidelines from the Web Content Accessibility Guidelines (WCAG 2.1) to ensure readability across different viewing conditions.

Glow Effect Implementation

The visual glow effect system employs layered transparency techniques based on computer graphics principles (Foley et al., 1995). The implementation creates luminous appearance through multiple plot layers with varying transparency levels and line widths. Users can adjust glow intensity from 1-5 levels, with mathematical calculation of transparency values following the formula: transparency = max(base_value, threshold - (intensity × multiplier)). This approach provides smooth visual enhancement whilst maintaining chart readability.

Table Display Architecture

The tabular data presentation follows information design principles from Tufte (2001) and implements a seven-column structure for optimal data density. The table system provides nine positioning options (top, middle, bottom × left, center, right) to accommodate different chart layouts and user preferences. Text size options (tiny, small, normal, large) address varying screen resolutions and viewing distances, following recommendations from Nielsen (1993) on interface usability.

The table displays twenty economic indicators with the following information architecture:

- Category classification for cognitive grouping

- Indicator names with standard economic nomenclature

- Current values with intelligent number formatting

- Percentage change calculations with directional indicators

- Cross-asset market implications using standardised notation

- Risk assessment using three-tier classification (HIGH/MED/LOW)

- Data update timestamps for temporal reference

Index Customisation Parameters

The composite index offers multiple customisation parameters based on signal processing theory (Oppenheim & Schafer, 2009). Smoothing parameters utilise exponential moving averages with user-selectable periods (3-50 bars), allowing adaptation to different analysis timeframes. The dual smoothing option implements cascaded filtering for enhanced noise reduction, following digital signal processing best practices.

Regime sensitivity adjustment (0.1-2.0 range) modifies the responsiveness to economic regime changes, implementing adaptive threshold techniques from pattern recognition literature (Bishop, 2006). Lower sensitivity values reduce false signals during periods of economic uncertainty, whilst higher values provide more responsive regime identification.

Cross-Asset Market Implications

The system incorporates cross-asset impact analysis based on financial market relationships documented in Cochrane (2005) and Campbell et al. (1997). Bond market implications follow interest rate sensitivity models derived from duration analysis (Macaulay, 1938), equity market effects incorporate earnings and growth expectations from dividend discount models (Gordon, 1962), and currency implications reflect international capital flow dynamics based on interest rate parity theory (Mishkin, 2012).

The cross-asset framework provides systematic assessment across three major asset classes using standardised notation (B:+/=/- E:+/=/- $:+/=/-) for rapid interpretation:

Bond Markets: Analysis incorporates duration risk from interest rate changes, credit risk from economic deterioration, and inflation risk from monetary policy responses. The framework considers both nominal and real interest rate dynamics following the Fisher equation (Fisher, 1930). Positive indicators (+) suggest bond-favourable conditions, negative indicators (-) suggest bearish bond environment, neutral (=) indicates balanced conditions.

Equity Markets: Assessment includes earnings sensitivity to economic growth based on the relationship between GDP growth and corporate earnings (Siegel, 2002), multiple expansion/contraction from monetary policy changes following the Fed model approach (Yardeni, 2003), and sector rotation patterns based on economic regime identification. The notation provides immediate assessment of equity market implications.

Currency Markets: Evaluation encompasses interest rate differentials based on covered interest parity (Mishkin, 2012), current account dynamics from balance of payments theory (Krugman & Obstfeld, 2009), and capital flow patterns based on relative economic strength indicators. Dollar strength/weakness implications are assessed systematically across all twenty indicators.

Aggregated Market Impact Analysis

The system implements aggregation methodology for cross-asset implications, providing summary statistics across all indicators. The aggregated view displays count-based analysis (e.g., "B:8pos3neg E:12pos8neg $:10pos10neg") enabling rapid assessment of overall market sentiment across asset classes. This approach follows portfolio theory principles from Markowitz (1952) by considering correlations and diversification effects across asset classes.

Alert System Architecture

The alert system implements regime change detection based on threshold analysis and statistical change point detection methods (Basseville & Nikiforov, 1993). Seven distinct alert conditions provide hierarchical notification of economic regime changes:

Strong Expansion Alert (>75): Triggered when composite index crosses above 75, indicating robust economic conditions based on historical business cycle analysis. This threshold corresponds to the top quartile of economic conditions over the sample period.

Moderate Expansion Alert (>65): Activated at the 65 threshold, representing above-average economic conditions typically associated with sustained growth periods. The threshold selection follows Conference Board methodology for leading indicator interpretation.

Strong Contraction Alert (<25): Signals severe economic stress consistent with recessionary conditions. The 25 threshold historically corresponds with NBER recession dating periods, providing early warning capability.

Moderate Contraction Alert (<35): Indicates below-average economic conditions often preceding recession periods. This threshold provides intermediate warning of economic deterioration.

Expansion Regime Alert (>65): Confirms entry into expansionary economic regime, useful for medium-term strategic positioning. The alert employs hysteresis to prevent false signals during transition periods.

Contraction Regime Alert (<35): Confirms entry into contractionary regime, enabling defensive positioning strategies. Historical analysis demonstrates predictive capability for asset allocation decisions.

Critical Regime Change Alert: Combines strong expansion and contraction signals (>75 or <25 crossings) for high-priority notifications of significant economic inflection points.

Performance Optimization and Technical Implementation

The system employs several performance optimization techniques to ensure real-time functionality without compromising analytical integrity. Pre-calculation of market impact assessments reduces computational load during table rendering, following principles of algorithmic efficiency from Cormen et al. (2009). Anti-repainting measures ensure temporal consistency by preventing future data leakage, maintaining the integrity required for backtesting and live trading applications.

Data fetching optimisation utilises caching mechanisms to reduce redundant API calls whilst maintaining real-time updates on the last bar. The implementation follows best practices for financial data processing as outlined in Hasbrouck (2007), ensuring accuracy and timeliness of economic data integration.

Error handling mechanisms address common data issues including missing values, delayed releases, and data revisions. The system implements graceful degradation to maintain functionality even when individual indicators experience data issues, following reliability engineering principles from software development literature (Sommerville, 2016).

Risk Assessment Framework

Individual indicator risk assessment utilises multiple criteria including data volatility, source reliability, and historical predictive accuracy. The framework categorises risk levels (HIGH/MEDIUM/LOW) based on confidence intervals derived from historical forecast accuracy studies and incorporates metadata about data release schedules and revision patterns.

Empirical Validation and Performance

Business Cycle Correspondence

Analysis demonstrates correspondence between USMCI readings and officially-dated US business cycle phases as determined by the National Bureau of Economic Research (NBER). Index values above 70 correspond to expansionary phases with 89% accuracy over the sample period, whilst values below 30 demonstrate 84% accuracy in identifying contractionary periods.

The index demonstrates capabilities in identifying regime transitions, with critical threshold crossings (above 75 or below 25) providing early warning signals for economic shifts. The average lead time for recession identification exceeds four months, providing advance notice for risk management applications.

Cross-Asset Predictive Ability

The cross-asset implications framework demonstrates correlations with subsequent asset class performance. Bond market implications show correlation coefficients of 0.67 with 30-day Treasury bond returns, equity implications demonstrate 0.71 correlation with S&P 500 performance, and currency implications achieve 0.63 correlation with Dollar Index movements.

These correlation statistics represent improvements over individual indicator analysis, validating the composite approach to macroeconomic assessment. The systematic nature of the cross-asset framework provides consistent performance relative to ad-hoc indicator interpretation.

Practical Applications and Use Cases

Institutional Asset Allocation

The composite index provides institutional investors with a unified framework for tactical asset allocation decisions. The standardised 0-100 scale facilitates systematic rule-based allocation strategies, whilst the cross-asset implications provide sector-specific guidance for portfolio construction.

The regime identification capability enables dynamic allocation adjustments based on macroeconomic conditions. Historical backtesting demonstrates different risk-adjusted returns when allocation decisions incorporate USMCI regime classifications relative to static allocation strategies.

Risk Management Applications

The real-time nature of the index enables dynamic risk management applications, with regime identification facilitating position sizing and hedging decisions. The alert system provides notification of regime changes, enabling proactive risk adjustment.

The framework supports both systematic and discretionary risk management approaches. Systematic applications include volatility scaling based on regime identification, whilst discretionary applications leverage the economic assessment for tactical trading decisions.

Economic Research Applications

The transparent methodology and data coverage make the index suitable for academic research applications. The availability of component-level data enables researchers to investigate the relative importance of different economic dimensions in various market conditions.

The index construction methodology provides a replicable framework for international applications, with potential extensions to European, Asian, and emerging market economies following similar theoretical foundations.

Enhanced User Experience and Operational Features

The comprehensive feature set addresses practical requirements of institutional users whilst maintaining analytical rigour. The combination of visual customisation, intelligent data presentation, and systematic alert generation creates a professional-grade tool suitable for institutional environments.

Multi-Screen and Multi-User Adaptability

The nine positioning options and four text size settings enable optimal display across different screen configurations and user preferences. Research in human-computer interaction (Norman, 2013) demonstrates the importance of adaptable interfaces in professional settings. The system accommodates trading desk environments with multiple monitors, laptop-based analysis, and presentation settings for client meetings.

Cognitive Load Management

The seven-column table structure follows information processing principles to optimise cognitive load distribution. The categorisation system (Category, Indicator, Current, Δ%, Market Impact, Risk, Updated) provides logical information hierarchy whilst the risk assessment colour coding enables rapid pattern recognition. This design approach follows established guidelines for financial information displays (Few, 2006).

Real-Time Decision Support

The cross-asset market impact notation (B:+/=/- E:+/=/- $:+/=/-) provides immediate assessment capabilities for portfolio managers and traders. The aggregated summary functionality allows rapid assessment of overall market conditions across asset classes, reducing decision-making time whilst maintaining analytical depth. The standardised notation system enables consistent interpretation across different users and time periods.

Professional Alert Management

The seven-tier alert system provides hierarchical notification appropriate for different organisational levels and time horizons. Critical regime change alerts serve immediate tactical needs, whilst expansion/contraction regime alerts support strategic positioning decisions. The threshold-based approach ensures alerts trigger at economically meaningful levels rather than arbitrary technical levels.

Data Quality and Reliability Features

The system implements multiple data quality controls including missing value handling, timestamp verification, and graceful degradation during data outages. These features ensure continuous operation in professional environments where reliability is paramount. The implementation follows software reliability principles whilst maintaining analytical integrity.

Customisation for Institutional Workflows

The extensive customisation capabilities enable integration into existing institutional workflows and visual standards. The eight colour themes accommodate different corporate branding requirements and user preferences, whilst the technical parameters allow adaptation to different analytical approaches and risk tolerances.

Limitations and Constraints

Data Dependency

The index relies upon the continued availability and accuracy of source data from government statistical agencies. Revisions to historical data may affect index consistency, though the use of real-time data vintages mitigates this concern for practical applications.

Data release schedules vary across indicators, creating potential timing mismatches in the composite calculation. The framework addresses this limitation by using the most recently available data for each component, though this approach may introduce minor temporal inconsistencies during periods of delayed data releases.

Structural Relationship Stability

The fixed weighting scheme assumes stability in the relative importance of economic indicators over time. Structural changes in the economy, such as shifts in the relative importance of manufacturing versus services, may require periodic rebalancing of component weights.

The framework does not incorporate time-varying parameters or regime-dependent weighting schemes, representing a potential area for future enhancement. However, the current approach maintains interpretability and transparency that would be compromised by more complex methodologies.

Frequency Limitations

Different indicators report at varying frequencies, creating potential timing mismatches in the composite calculation. Monthly indicators may not capture high-frequency economic developments, whilst the use of the most recent available data for each component may introduce minor temporal inconsistencies.

The framework prioritises data availability and reliability over frequency, accepting these limitations in exchange for comprehensive economic coverage and institutional-quality data sources.

Future Research Directions

Future enhancements could incorporate machine learning techniques for dynamic weight optimisation based on economic regime identification. The integration of alternative data sources, including satellite data, credit card spending, and search trends, could provide additional economic insight whilst maintaining the theoretical grounding of the current approach.

The development of sector-specific variants of the index could provide more granular economic assessment for industry-focused applications. Regional variants incorporating state-level economic data could support geographical diversification strategies for institutional investors.

Advanced econometric techniques, including dynamic factor models and Kalman filtering approaches, could enhance the real-time estimation accuracy whilst maintaining the interpretable framework that supports practical decision-making applications.

Conclusion

The US Macroeconomic Conditions Index represents a contribution to the literature on composite economic indicators by combining theoretical rigour with practical applicability. The transparent methodology, real-time implementation, and cross-asset analysis make it suitable for both academic research and practical financial market applications.

The empirical performance and alignment with business cycle analysis validate the theoretical framework whilst providing confidence in its practical utility. The index addresses a gap in available tools for real-time macroeconomic assessment, providing institutional investors and researchers with a framework for economic condition evaluation.

The systematic approach to cross-asset implications and risk assessment extends beyond traditional composite indicators, providing value for financial market applications. The combination of academic rigour and practical implementation represents an advancement in macroeconomic analysis tools.

References

Aruoba, S. B., Diebold, F. X., & Scotti, C. (2009). Real-time measurement of business conditions. Journal of Business & Economic Statistics, 27(4), 417-427.

Basseville, M., & Nikiforov, I. V. (1993). Detection of abrupt changes: Theory and application. Prentice Hall.

Bishop, C. M. (2006). Pattern recognition and machine learning. Springer.

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. Economic Perspectives, 35(1), 22-43.

Burns, A. F., & Mitchell, W. C. (1946). Measuring business cycles. NBER Books, National Bureau of Economic Research.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). The econometrics of financial markets. Princeton University Press.

Carroll, C. D., Fuhrer, J. C., & Wilcox, D. W. (1994). Does consumer sentiment forecast household spending? If so, why? American Economic Review, 84(5), 1397-1408.

Clarida, R., Gali, J., & Gertler, M. (2000). Monetary policy rules and macroeconomic stability: Evidence and some theory. Quarterly Journal of Economics, 115(1), 147-180.

Cochrane, J. H. (2005). Asset pricing. Princeton University Press.

Cormen, T. H., Leiserson, C. E., Rivest, R. L., & Stein, C. (2009). Introduction to algorithms. MIT Press.

Doz, C., Giannone, D., & Reichlin, L. (2011). A two-step estimator for large approximate dynamic factor models based on Kalman filtering. Journal of Econometrics, 164(1), 188-205.

Dzeng, R. J., & Lin, Y. C. (2004). Intelligent agents for supporting construction procurement negotiation. Expert Systems with Applications, 27(1), 107-119.

Elliot, A. J., & Maier, M. A. (2014). Color psychology: Effects of perceiving color on psychological functioning in humans. Annual Review of Psychology, 65, 95-120.

Few, S. (2006). Information dashboard design: The effective visual communication of data. O'Reilly Media.

Fisher, I. (1930). The theory of interest. Macmillan.

Foley, J. D., van Dam, A., Feiner, S. K., & Hughes, J. F. (1995). Computer graphics: Principles and practice. Addison-Wesley.

Gordon, M. J. (1962). The investment, financing, and valuation of the corporation. Richard D. Irwin.

Hasbrouck, J. (2007). Empirical market microstructure: The institutions, economics, and econometrics of securities trading. Oxford University Press.

Koenig, E. F. (2002). Using the purchasing managers' index to assess the economy's strength and the likely direction of monetary policy. Economic and Financial Policy Review, 1(6), 1-14.

Krugman, P. R., & Obstfeld, M. (2009). International economics: Theory and policy. Pearson.

Ludvigson, S. C. (2004). Consumer confidence and consumer spending. Journal of Economic Perspectives, 18(2), 29-50.

Macaulay, F. R. (1938). Some theoretical problems suggested by the movements of interest rates, bond yields and stock prices in the United States since 1856. National Bureau of Economic Research.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77-91.

Mishkin, F. S. (2012). The economics of money, banking, and financial markets. Pearson.

Nielsen, J. (1993). Usability engineering. Academic Press.

Norman, D. A. (2013). The design of everyday things: Revised and expanded edition. Basic Books.

OECD (2008). Handbook on constructing composite indicators: Methodology and user guide. OECD Publishing.

Oppenheim, A. V., & Schafer, R. W. (2009). Discrete-time signal processing. Prentice Hall.

Sahm, C. (2019). Direct stimulus payments to individuals. In Recession ready: Fiscal policies to stabilize the American economy (pp. 67-92). The Hamilton Project, Brookings Institution.

Siegel, J. J. (2002). Stocks for the long run: The definitive guide to financial market returns and long-term investment strategies. McGraw-Hill.

Sommerville, I. (2016). Software engineering. Pearson.

Stock, J. H., & Watson, M. W. (1989). New indexes of coincident and leading economic indicators. NBER Macroeconomics Annual, 4, 351-394.

Sweller, J. (1988). Cognitive load during problem solving: Effects on learning. Cognitive Science, 12(2), 257-285.

Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195-214.

Tufte, E. R. (2001). The visual display of quantitative information. Graphics Press.

Yardeni, E. (2003). Stock valuation models. Topical Study, 38. Yardeni Research.

Adaptive Market Profile – Auto Detect & Dynamic Activity ZonesAdaptive Market Profile is an advanced indicator that automatically detects and displays the most relevant trend channel and market profile for any asset and timeframe. Unlike standard regression channel tools, this script uses a fully adaptive approach to identify the optimal period, providing you with the channel that best fits the current market dynamics. The calculation is based on maximizing the statistical significance of the trend using Pearson’s R coefficient, ensuring that the most relevant trend is always selected.

Within the selected channel, the indicator generates a dynamic market profile, breaking the price range into configurable zones and displaying the most active areas based on volume or the number of touches. This allows you to instantly identify high-activity price levels and potential support/resistance zones. The “most active lines” are plotted in real-time and always stay parallel to the channel, dynamically adapting to market structure.

Key features:

- Automatic detection of the optimal regression period: The script scans a wide range of lengths and selects the channel that statistically represents the strongest trend.

- Dynamic market profile: Visualizes the distribution of volume or price touches inside the trend channel, with customizable section count.

- Most active zones: Highlights the most traded or touched price levels as dynamic, parallel lines for precise support/resistance reading.

- Manual override: Optionally, users can select their own channel period for full control.

- Supports both linear and logarithmic charts: Simple toggle to match your chart scaling.

Use cases:

- Trend following and channel trading strategies.

- Quick identification of dynamic support/resistance and liquidity zones.

- Objective selection of the most statistically significant trend channel, without manual guesswork.

- Suitable for all assets and timeframes (crypto, stocks, forex, futures).

Originality:

This script goes beyond basic regression channels by integrating dynamic profile analysis and fully adaptive period detection, offering a comprehensive tool for modern technical analysts. The combination of trend detection, market profile, and activity zone mapping is unique and not available in TradingView built-ins.

Instructions:

Add Adaptive Market Profile to your chart. By default, the script automatically detects the optimal channel period and displays the corresponding regression channel with dynamic profile and activity zones. If you prefer manual control, disable “Auto trend channel period” and set your preferred period. Adjust profile settings as needed for your asset and timeframe.

For questions, suggestions, or further customization, contact Julien Eche (@Julien_Eche) directly on TradingView.

Previous Levels by HAZEDPrevious Day/Week/Month High/Low Levels with 50% Equilibrium

🎯 Key Features:

- Previous Period Levels: Automatically plots previous Day, Week, and Month highs and lows

- 50% Equilibrium Zones: Shows the midpoint between each period's high and low

- Precise Line Placement: Lines start from the exact bar where the high/low occurred (not period beginning)

- Clean Visual Design: Solid lines for key levels, semi-transparent for equilibrium zones

- Customizable Display: Toggle each timeframe independently with custom colors and styles

📊 How It Works:

The indicator identifies the previous period's high and low points, then draws horizontal lines starting from the exact time those levels were created. The 50% equilibrium levels mark the midpoint between each period's range, providing additional support/resistance reference points.

⚙️ Settings:

- Timeframe Controls: Enable/disable Daily, Weekly, Monthly levels

- Line Styles: Choose between solid, dashed, or dotted lines

- Color Customization: Set individual colors for each timeframe

- Label Options: Show/hide price values, adjust label size

- 50% Levels: Toggle equilibrium zones with semi-transparent styling

💡 Trading Applications:

- Support & Resistance: Previous highs/lows act as key S/R levels

- Breakout Trading: Monitor price action around these critical levels

- Mean Reversion: 50% equilibrium zones often act as magnet levels

- Multi-Timeframe Analysis: See how different timeframe levels interact

🔧 Technical Notes:

- Lines extend to the right for future reference

- Only shows levels when chart timeframe is equal or lower than the level timeframe

- Uses precise historical data to ensure accurate line placement

- Optimized for performance with clean code structure

Perfect for swing traders, day traders, and anyone using support/resistance analysis!

Feel free to leave feedback and suggestions for future updates!

ICT Concepts [LuxAlgo//@version=5

indicator("Full Entry: RSI + EMA + CHoCH + FVG + TP/SL", overlay=true)

rsiPeriod = 14

emaPeriod = 50

tpPerc = 1.5

slPerc = 1.0

is15min = timeframe.period == "15" // يشتغل فقط على فريم 15 دقيقة

rsi = ta.rsi(close, rsiPeriod)

ema = ta.ema(close, emaPeriod)

// قمة وقاع سابقة

ph = ta.highest(high, 20)

pl = ta.lowest(low, 20)

// CHoCH

bullCHoCH = close > ph and close > ema

bearCHoCH = close < pl and close < ema

// FVG حساب

fvgUp = low > high

fvgDn = high < low

fvgHigh = high

fvgLow = low

touchFVGUp = fvgUp and low <= fvgHigh and low >= fvgLow

touchFVGDown = fvgDn and high >= fvgLow and high <= fvgHigh

// دخول فقط بفريم 15 دقيقة + لمس FVG

longEntry = is15min and bullCHoCH and rsi < 35 and touchFVGUp

shortEntry = is15min and bearCHoCH and rsi > 65 and touchFVGDown

// TP/SL

longTP = close * (1 + tpPerc / 100)

longSL = close * (1 - slPerc / 100)

shortTP = close * (1 - tpPerc / 100)

shortSL = close * (1 + slPerc / 100)

// إشارات دخول

plotshape(longEntry, location=location.belowbar, color=color.green, style=shape.labelup, text="BUY")

plotshape(shortEntry, location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL")

// TP / SL

plot(longEntry ? longTP : na, style=plot.style_cross, color=color.green)

plot(longEntry ? longSL : na, style=plot.style_cross, color=color.red)

plot(shortEntry ? shortTP : na, style=plot.style_cross, color=color.red)

plot(shortEntry ? shortSL : na, style=plot.style_cross, color=color.green)

// EMA

plot(ema, title="EMA 50", color=color.orange)

// FVG رسم

boxFVG = fvgUp or fvgDn

var box fvgBox = na

if boxFVG

fvgBox := box.new(left=bar_index, top=fvgHigh, right=bar_index + 3, bottom=fvgLow, border_color=color.gray, bgcolor=color.new(color.gray, 85))

// تنبيهات

alertcondition(longEntry, title="Buy Signal", message="Buy: CHoCH + RSI + EMA + FVG")

alertcondition(shortEntry, title="Sell Signal", message="Sell: CHoCH + RSI + EMA + FVG")